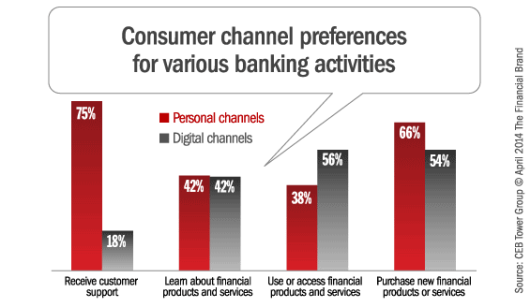

According to CEB TowerGroup research, the majority of retail banking customers in the U.S. prefer to bank through digital (online and mobile) channels. If these trends continue, at least 70% of customers in the future will primarily access their bank through non-personal channels.

But, while consumers indicate that they prefer digital channels for accessing their accounts and for learning about new products and services, they still prefer in-person channels for purchasing those same services and for customer support and problem resolution. In fact, receiving customer support is now the only banking activity that remains dominated by personal channels, due largely to poor digital service and problem resolution. In addition, less than 5% of all respondents indicated that they preferred the mobile channel exclusively across these four key interaction types.

So what is holding customers back from using digital channels for more of their banking? Why do so many customers prefer a balanced mix of digital and personal channels as opposed to using digital channels exclusively?

Digital Service Gap

“Digital preference customers tend to have a more difficult time getting their issues resolved.”

— Nicole Sturgill, CEB TowerGroup Research Director

Nicole Sturgill, research director at CEB TowerGroup discussed these challenges at the CEB Financial Services Technology Summit in Boston in a session called, ‘Closing the Service Gap in Digital Channels.’

“One of the reasons customer transition to exclusively digital banking has lagged is because multichannel customers, especially those who lean towards in-person banking, experience the best service,” says Sturgill. “Interestingly, our research shows that customers who prefer both an exclusive in-person experience or a digital experience are less satisfied than true multichannel customers, and that exclusively digital channel customers are the least satisfied.”

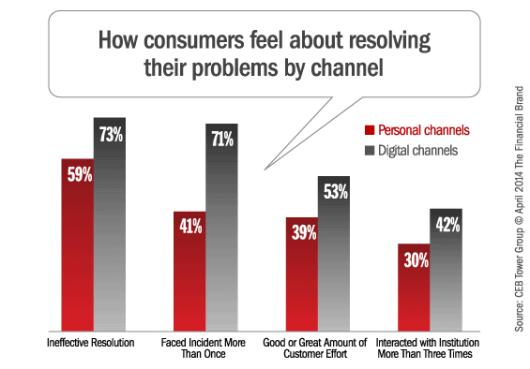

The CEB TowerGroup research found that digital channel service and problem resolution fell short across the board when evaluating how effectively issues were resolved, whether the issue occurred more than once, how much effort needed to be expended by the customer, and how many interactions were needed to resolve an issue.

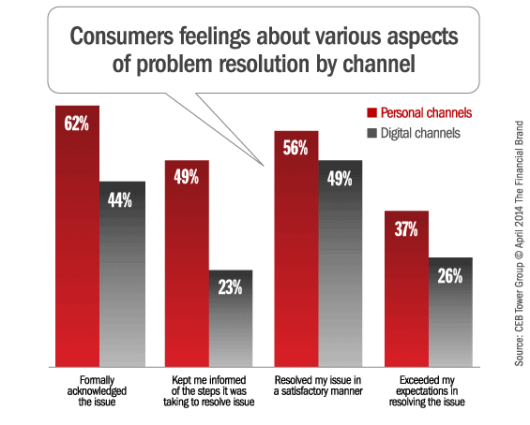

It was further found that even when issues were resolved, digital customers were less likely to feel that the bank communicated appropriately while the issue was being resolved. As shown below, personal channel customers were twice as likely as digital customers to say that the institution kept them informed on the issue resolution process, and 10% less likely to think that the bank exceeded their expectations in resolving the issue.

According to Sturgill, part of the challenge could be the desire by banks to provide cross-channel consistency. “The goal of ‘omnichannel banking’ or trying to provide the same level of service through all channels has caused too much complexity, allowing customers to choose channels that don’t work well for what they are trying to accomplish,” says Sturgill. “This creates confusion when the transaction doesn’t work as expected.” She also noted that cross-channel distribution further increases the demands on banks for channel maintenance, resulting in greater costs while failing to improve customer loyalty.

Instead of encouraging customers to self-select the channel of their choice (which is the aspiration of many proponents of omnichannel banking), CEB TowerGroup research recommends that retail banks reduce complexity and decrease costs by making two changes:

- Differentiating channel functionality according to the intrinsic strengths and costs of each banking channel

- Proactively guiding customers to the channel that best fits their banking need

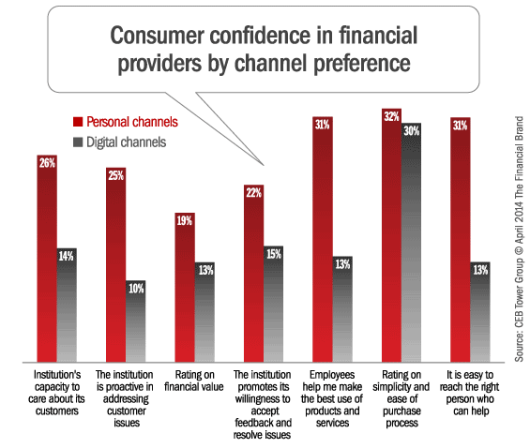

Following these guidelines runs counter to the current industry drumbeat of moving as much as possible to digital channels or towards channel agnostic omnichannel banking. But it would be consistent with customer confidence in the ability for the personal channel to deliver better than digital across a variety of service attributes.

Weak Correlation Between Satisfaction and Loyalty

A CEB study of more than 97,000 consumers and business customers globally showed a weak relationship between satisfaction and loyalty. In fact, 20% of satisfied customers said they intended to leave their provider, while 28% of dissatisfied customers said they intended to stay. This data points to the possibility that customer satisfaction is a poor—and potentially dangerous—guide for gauging digital service strategy progress and resource allocation.

“There is a definite correlation between low customer effort and high customer loyalty.”

— Rick DeLisi, Senior Director of CEB

Several times during the CEB Financial Services Technology Summit, it was emphasized that the desire to ‘exceed customer expectations’ across channels may not only be an unachievable goal, but a highly costly one as well. More specifically, their data showed that loyalty increases when customers’ expectations are met and remains unchanged when they are exceeded.

During one of the keynote addresses, Rick DeLisi, senior director of CEB and co-author of the book, The Effortless Experience: Conquering the New Battleground for Customer Loyalty, illustrated how ‘delighting the customer’ only occurs 16% of the time, while increasing operating costs by 10-20%. In addition, not guiding customers to a ‘best’ channel to resolve service issues can actually decrease loyalty because of increased effort required of the customer, including:

- Needing to make repeat contacts

- Needing to switch channels to get resolution

- Internal transfers between CSRs or departments

- Needing to repeat information

- ‘Robotic’ service

- Internal policies and processes that don’t make sense to the customer

- The ‘hassle factor’

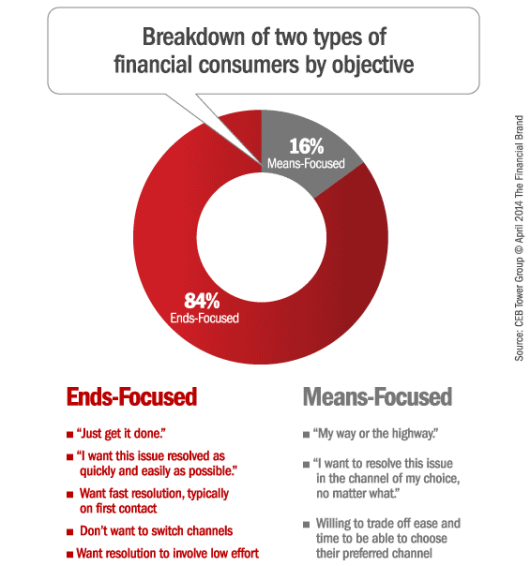

Bottom line, CEB research has found that cross-channel consistency was not the answer to resolve the service issues that we are seeing in digital channels. In fact, the vast majority of customers don’t care what channel they have to use to resolve a service issue … they just want the issue to be resolved. As a result, retail banks should cater to the majority, who value efficiency over cross-channel consistency.

Closing The Digital Service Gap

A positive digital service experience is by definition driven by technology. Business Process Management (BPM) technology allows for consistent problem resolution workflows throughout the organization, while CRM applications allow the bank to track customer issues and ensure that frontline staff is aware of any outstanding customer issues.

According to CEB TowerGroup research, retail banking and credit union executives should do the following to improve service quality in digital channels:

- Guide customers to the best channel(s) for problem resolution needs

- Review problem resolution workflows, evaluating for customer ease of use

- Leverage customer communications management to acknowledge issue

- Provide ongoing status updates using customer’s channel of choice

- Measure resolution effectiveness over time

The pressure to meet consumer expectations for multichannel sales and service mounts on a daily basis. In response, a majority of financial services organizations are adding more options in existing channels. While on the surface this appears to be a good response, CEB TowerGroup shows that it causes many organizations to rush headlong into work-arounds and the “appearance” of multiple channel capabilities — but without the actual functionality of multiple channels.

The result is increased effort on the part of consumers to resolve issues. According to the research, 96 percent of survey respondents indicated that high effort experiences drive disloyalty. To close the digital service gap, financial institutions should focus on ensuring their customer-facing digital channel applications are designed for ease of use, with customers being guided to the best channel for problem resolution.