Since the beginning of the year, I have been part of the beta tests for new industry players Simple, GoBank and Moven. While each of these new players have different features and benefits, they differ from traditional banks significantly more than they differ from each other. They are what could be called NeoBanks — those offering retail banking services but without physical locations (what Ron Shevlin originally termed “NeoChecking”). These new competitors are garnering a great deal of industry attention, as much due to their mobile-first positioning as their rapid market penetration.

Shevlin says that one day NeoBanks like these may very well be rivals at war. But for now, the firms are better off collaborating than fighting. These new players have to educate consumers on what a new type of bank is, will be, or could be. They have to build demand for the new type of bank they’re building. Which is, of course, no easy feat.”

Marketers in the traditional banking space — retail banks and credit unions — need to take heed. Ignoring players like Moven, Simple and Bluebird from Amex is a big mistake. At the very least, traditional banks and credit unions need to learn from what these firms are doing right and apply what they can to their offerings. Failure to give these startups the attention they deserve could yield a huge competitive advantage to them, and leave you behind the eight ball playing catch-up.

Focus on Intuitive Design and Simplicity

When you visit their websites, what is immediately apparent about these NeoBanks is their focus on ease of use, whether you want to open an account, transact business or communicate with the firms on a one-to-one basis.

Instead of websites that are littered with more information than any consumer could digest and awkward processes, these NeoBanks understand the customer experience and create a pleasurable customer journey. When was the last time a customer said that about your bank or credit union?

While there are those who will point out that these banks don’t offer the vast array of products and services that are available at a traditional bank, I would challenge most banks to review their checking account page(s) and compare the user interface of their website to the NeoBanks.

I have also noticed that as Moven, Simple or GoBank add new features, the complexity of my relationship with these banks has not increased. Instead, simplicity is part of the innovation process.

While each of the NeoBanks have staggered their market rollout to manage demand and their ability to support new clients (Simple and Moven still have people in virtual queuing lines waiting to open an account), the ease of opening an account at any of these banks is unparalleled (a Virtual Wallet account opening at PNC is close).

Tracking Spending

What’s nice about the NeoBanks is that they were built from the ground up with a focus on providing the most dynamic and instantaneous method of tracking spending. By providing real-time feedback, smarter spending decisions can be made.

My GoBank account is set up with the debit card as the focal point of the relationship, whereby Moven and Simple are definitely mobile applications with card access. Moven even provides a PayPass sticker for the back of my mobile device for card-less payments.

While GoBank doesn’t provide the amount of depth of insight into every transaction I do, I still believe the balance bar is the best mobile app in the banking world. While not flashy, it allows me to see my balance with one swipe of the finger without logging into my mobile account if I wish (I had to pre-authorize this capability).

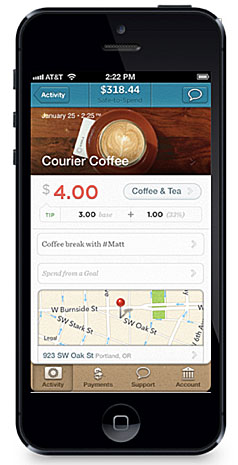

When viewing transaction history, Simple provides a number of options to provide notations about purchases, including the option to add a memo to the purchase, a picture of what was bought (or where I ate) and even a map of the location. The view on my desktop is very similar to what I can view on my phone.

My Moven account goes a step further than Simple, providing an immediate receipt for each purchase on my phone (or by text/email) as well as giving me insight into how much I have spent in any individual category or at a specific location. Over time, I also get information as to whether my spending in any category (or at a specific location) is on track with previous behavior. Moven has even talked about providing insight into how my spending compares to other people in my behavioral/demographic segment.

Integrated PFM

While the definition and extent of personal financial management (PFM) differs quite a bit between the three banks, the functionality is definitely integrated within the application as opposed to being added on as an accessory. The tools are all very intuitive and in the case of Moven, very feature-rich, with account history, goal setting, budgeting, etc. all front and center with both the online and mobile versions.

What is interesting about the Moven application is that as opposed to providing a ‘rear-view mirror’ look at my finances, Moven looks ahead to what is going to occur and provides immediate insight into my most recent purchase as well as my purchases over time. Without massive charts or graphs, I am able to get a feel for how my spending behavior varies over time.

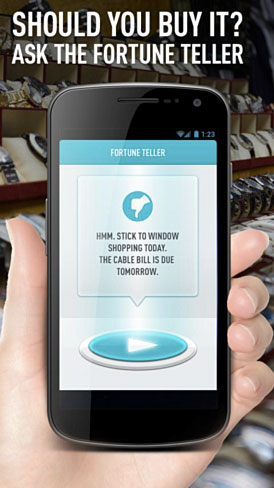

GoBank also allows me to set funds aside in my Money Vault and combined with my budgeting feature, will tell me if I am buying something that may cause me to be short of funds later. If funds set aside for future bills are not enough to allow a current purchase, the GoBank Fortune Teller will let me know that I may want to reconsider my purchase. This is actually a very fun and helpful tool if the account is actively used.

Setting Goals

For most people, setting financial goals is more of an ambition than a way of life. I try to set aside money for upcoming events or purchases, but most of the time, I pay for things after I do them (using credit).

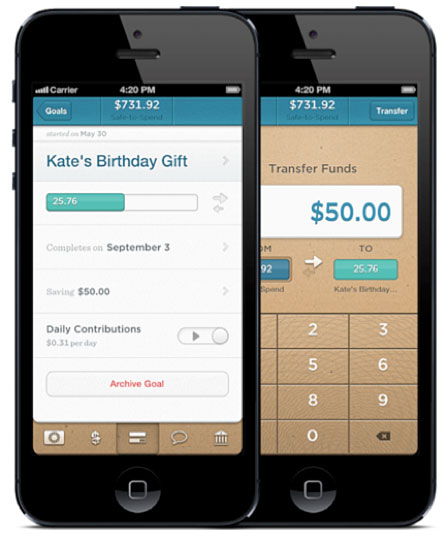

With Simple, the process has been made super easy, using virtual version of the envelope method most of us grew up with. Numerous different ‘Goals’ can be set instantaneously using either the online or mobile interface and funds are automatically set aside each day for my larger purchases.

When paired with the ‘Safe-to-Spend’ feature, my amount set aside for Goals and upcoming payments due are subtracted from my available balance to give me an accurate picture of how much I can really spend.

With the mobile version of Goals, I can avoid impulse purchases and set a goal for something I want to purchase when I see it (like for the new iPhone case I have my eye on). When my goal is met, I can then transfer the funds from my goal to the purchase.

Read More: 7 Reasons to Love GoBank

Deposits and Bill Payments

As can be expected, deposits into any of the NeoBanks is done electronically, either by mobile photo deposit or funds transfer. The process is extremely simple (pun intended) and intuitive. The delay for getting credit for the deposits varies, hoever, with GoBank still having the longest hold time for personal check deposits (government and employment auto deposits occur much quicker).

Since none of the NeoBanks provide checks with their account (you can request checks with Bluebird), payments with these institutions is much different than with traditional banks.

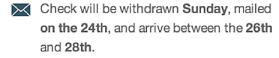

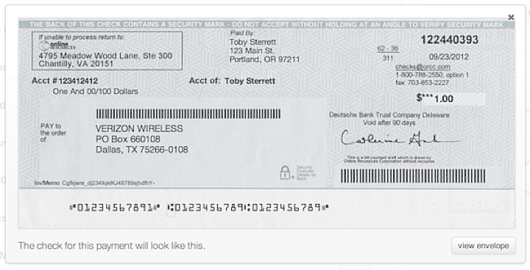

For example, Simple provides a way to select the date I want my payment to be received as opposed to the traditional method of selecting the day I want the payment sent. Simple does the math to determine how far in advance the payment should be sent. They write the check (or send via EFT) and I don’t need to worry. In addition, I receive a clear notification of my payments and even a view of what the check will look like before it is sent.

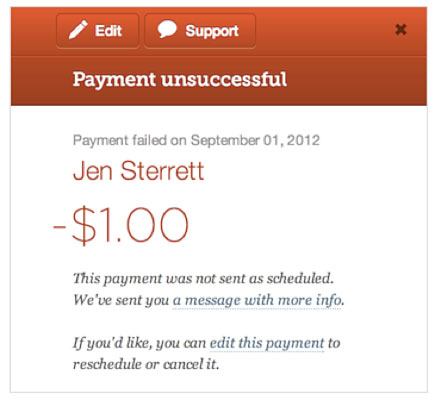

Simple even notifies me if a payment can’t be made as scheduled because of the lack of funds on the day of the scheduled transfer. As opposed to overdrawing the account, they send a message to inform me that a payment is being delayed due to lack of funds.

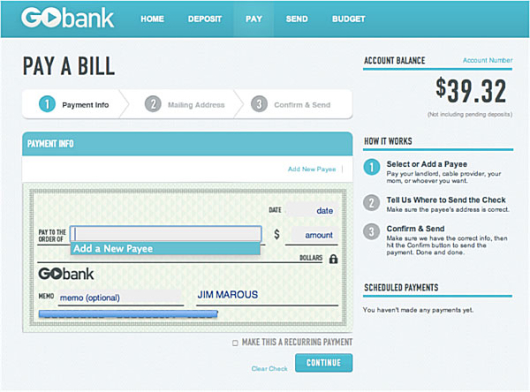

GoBank payments digitizes the check writing process of old with virtual checks being available online to write and have processed. All I need to do is fill in the blanks and the bill is paid.

P2P

Since each of these new banks were built from a digital perspective, P2P payments are one of the best functionalities. While I have spent as much as an hour trying to set up and then make transfers with most of my traditional banks (some require test payments and/or exact matching of names in the required fields), making a P2P transfer with any of my beta banks provides alternatives and is easy to do. But not all of the banks use the same process.

For instance, with my Simple account, I create a new contacts by simply adding a person’s name, email, phone number, & address. After that, I can request Simple to send my contact a check for any given amount provided I have the funds available to do so. A combination of old school and new school.

At GoBank, it is all new school, with the option of sending money to anyone in my contact database using either their email or the mobile phone number. The recipient will get an email or text message with instructions for claiming their money. If the recipient is a GoBanker, they’ll receive the funds automatically. If the recipient isn’t a GoBanker, they have the option to either open a GoBank account to retrieve the money or transfer the money to their PayPal account. If they don’t pick up the money within 10 days, I get a notification and the money back in my account.

The team at Moven is going even a step further, making payments super simple by mobile phone number, email or through Facebook. What’s great is that when I authorize my contacts to be accessed by Moven, the payment process is only a click away since I won’t need to re-enter any recipient information. In other words, I can pay a friend in seconds as opposed to minutes and can do so from my mobile device. Very cool.

Customer Acquisition

With Simple and GoBank expanding beyond initial beta testing and Moven gaining momentum, each NeoBank is beginning to generate more buzz in the marketplace. None is as aggressive as GoBank, with the placement of applications at RiteAid and Kmarts and the product placement on the show Project Runway.

GoBank also has been the most aggressive with social media and referral programs, using current customers, friends from Facebook and others to promote their new services. While no statistics are available on the success of any of these initiatives, some of the efforts must be exceeding expectations since my screen cleaner shipment was delayed due to demand that quickly exceeded the inventory.

Conclusion

Time will tell as to the ultimate success of these new ventures, but I strongly encourage all bank and credit union marketers to open each of these accounts to view how a mobile-first mentality can change product development, product delivery and even customer communication. I for one have been very impressed with each of these offerings and have used the accounts significantly more than any previous ‘shopper’ account I have opened due to the ease of use and the fun I have had banking.