Once considered a product for the unbanked, prepaid cards are rapidly gaining mainstream status. More than 18 million people used a prepaid debit card last year according to the 2013 Financial Literacy Report conducted by Harris Research. In fact, seven out of eight have or previously had a checking account, and two in three have previously owned a credit card (Pew Charitable Trust 2013).

Only one in four (24%) say they use prepaid debit cards because they have no other payment or banking options. (2013 Financial Literacy Report). So these are not the unbanked.

The fact that big box retailers, drug and convenience stores have successfully used prepaid cards to syphon off bank customers is more a testament to their marketing prowess than the quality of their product. They have convinced many users that an inferior checking substitute is cheaper and more convenient than the real thing. And banks live with the charade.

Vendors may add paper checks, ATM withdrawals, direct deposit and money transfer services to their debit card but it’s still checking-lite — a contorted product without FDIC insurance, credit-building opportunities or the protections of conventional checking accounts.

Prepaid users cite high monthly or overdraft fees as reasons for giving up their checking accounts but pre-paid fees can be much higher. Critics have panned celebrities such as Kim Kardashian, Lil Wayne and Suze Orman for putting out their own card and charging excessive fees. Ironically, customer attitudes don’t translate to action. The Pew study found two thirds of prepaid customers did not compare terms and fees when they obtained their card. They simply chose cards recommended to them or ones they saw in a store.

Even prepaid users recognize their card’s a poor substitute for a checking account. In fact, 58% want a checking account in the future (Pew 2014). They aspire to own a checking account.

Community banks and credit unions can meet the needs of prepaid users, give them a better product AND better positon themselves for growth by building their own all-digital account around a debit card. But they must show a little creatively.

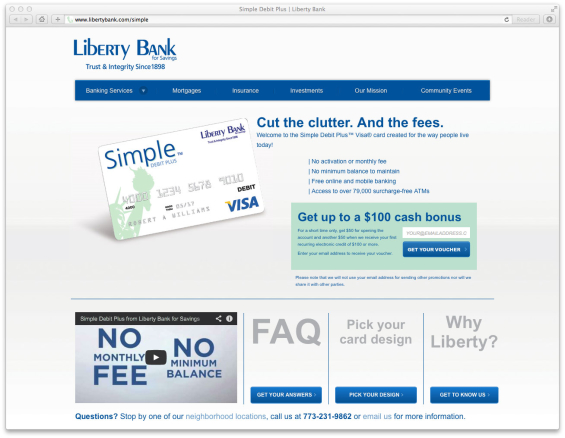

Liberty Bank for Savings, Chicago, recently introduced Simple Debit Plus Visa, a no-minimum balance, no monthly-fee debit card with access to all electronic banking services. Paper checks are not available. The cards bear the photo of iconic neighborhood scenes to reinforce the community orientation of the bank. It has the no-minimum, no overdraft fees associated with a prepaid card, but with the FDIC insurance, ATM networks, bill pay and money transfers that prepaid cards have trouble duplicating. We also tacked on ADD insurance and an identity theft resolution service. Our target is 30-55 year-olds.

Consumers don’t have to settle for a jerry-rigged, almost-good-enough, nearly-a-checking account. Why should they settle, when they can have the real thing, start the savings program they want and build their credit scores?

This low-cost, no-check checking account may not work for every bank or every customer, but Liberty struck a chord with young and older consumers. And it’s a product virtually every community bank and credit union can offer. There’s no reason to let the big box and drug stores steal customers, especially when you have a better quality product.