The continuous growth in digital channel use has impacted basic banking transactions the most, including checking balances, paying a bill, transferring money and even depositing a check. Over time, the paying of bills through online and mobile channels has approached universal acceptance, with 74% of online banking users taking advantage of online bill pay, and 65% of mobile bankers using mobile bill pay.

These were some of the findings of Fiserv’s quarterly Expectations & Experiences survey. The survey, conducted by Harris Poll among 3,031 banking consumers in the U.S., found adoption of all digital payment options increasing as consumers become increasingly comfortable with digital technologies. For instance, the top 5 online banking uses were:

- Paying bills (75%)

- Transferring money (60%)

- Receiving bills electronically (35%)

- Receiving alerts regarding activity on an account (35%)

- Making loan payments online (28%)

Similarly, the acceptance and use of mobile banking has grown, with the types of transactions being done expanding beyond rudimentary banking:

- Viewing balances (80%)

- Transferring money (56%)

- Paying bills through financial organization’s bill pay service (41%)

- Depositing a check (39%)

- Receiving account alerts via mobile or email (36%)

Digital Payments Surpass Traditional Options

While consumers continue to use traditional payment methods such as direct mail, pay-by-phone and in-person payments, online and mobile payments (either through the

financial organization or through the biller) now make up 59% of payments, according to the Fiserv research. Not only have the majority of consumers switched to digital channels, they are happy with their decision. For online bill pay users, 79% rated the service 8 of 10 or higher, with 70% of mobile bill pay users having the same sentiment.

The reason for the satisfaction is clear. Both banking bill pay services and biller direct services provide speed and convenience. Major points of differentiation between the services are evident though, with biller direct services getting higher marks for speed and financial institution options being preferred due to the ability to pay multiple organizations in one sitting.

Mobile Bill Payment Growing in Importance

While the acceptance is lower for mobile bill pay, the correlation between mobile bill pay customers and revenue generating services should be noted. According to Fiserv, “While 53% of [consumers] with five or fewer services use mobile bill pay, 83% of consumers with 10 or more revenue-generating products use the service.”

The primary difference between online and mobile payment customers is the desire for real-time engagement. For instance, 85% of Gen Xers say real-time payment delivery is at least somewhat important, while 93% of the Millennial segment agree. “Whether it’s availability of deposits, cash from a check, or withdrawals of funds and credit of payments, consumers are clear about one thing: They want it now,” says Fiserv.

Millennials Lead in Digital Payments Use

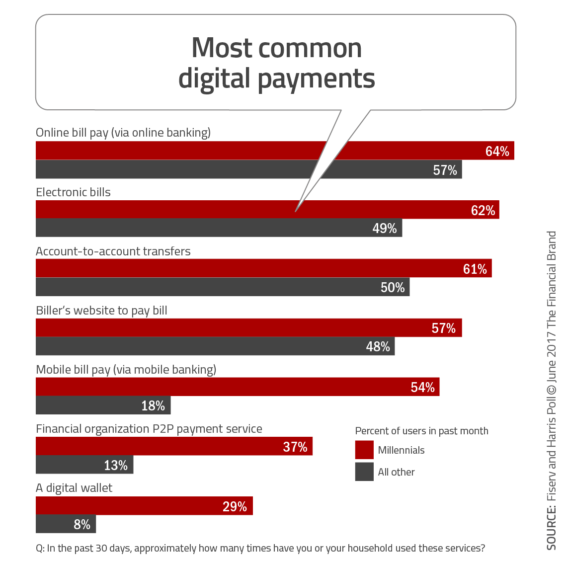

Millennials (ages 18–36) are unafraid of new technology and have embraced every possible way to pay. Compared to older demographic segments, Millennials are more likely to have used online banking, mobile bill pay, digital wallets and payment options from outside providers.

Compared to age group segments, Millennials are approximately three times as likely to use mobile bill pay, P2P payments and digital wallets.

P2P Poised for Significant Growth

All market indicators point to person-to-person (P2P) use to be the ‘next big thing.’ Not only do the benefits of P2P align with the desires of the digital consumer (speed, security and real-time availability), but the marketplace is about to explode with options. Beyond P2P services offered by financial institutions and organizations such as Square Cash and PayPal (Venmo) today, new options from the banking industry (Zelle) and Apple (Apple Pay Cash) are also coming online.

While still small in scale, the share of active consumers – defined as those who say they have used the service in the past 30 days – has increased by more than one-third compared to 2015, from 14% to 19%. The appeal of P2P, according to the research, includes that it saves time and hassle compared to using cash or checks (54%), is more convenient than cash or checks (51%) and that it provides more control (35%).

When nonusers were asked what has held them back from trying the mobile payment option, the largest percentage noted that they preferred options – such as cash, checks and credit card. The percentage noting this reason were obviously skewed to older demographic segments. The good news is that the concern around security actually fell 8% to 21% from last year.

Digital Wallets Mirror Online Banking Adoption Curve

Possibly not meeting early expectations, the early adoption curve for mobile wallets is very similar to what was seen in the early days of online banking. According to the Pew Research Center, the earliest online banking users tended to be younger and have higher incomes than the overall population. The Fiserv research found the same patterns of acceptance for the early adopters of digital wallets.

Early adoptors of mobile wallets include:

- 15% Consumers overall

- 28% Urban

- 32% Millennials

- 33% High net worth

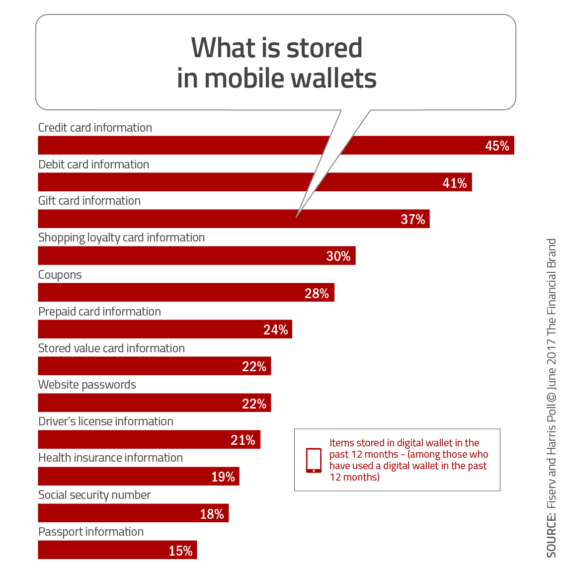

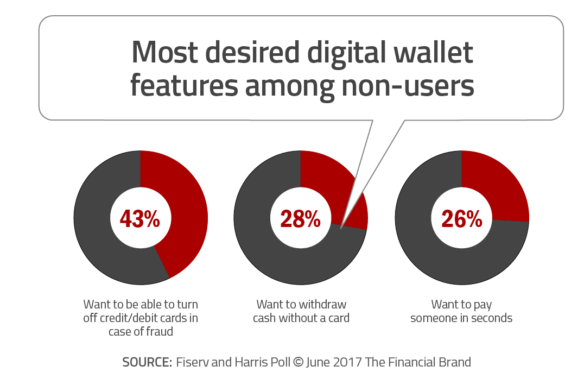

Similar to what is stored in a typical physical wallet, a mobile wallets is primarily used to store payment information, loyalty program membership and coupons. The primary features wanted by nonusers of mobile wallets were the control over card security (43%), replacing plastic cards with a digital alternative (28%) and speed of transaction (26%).