Two of every five people say cashback is their favorite credit card feature, eMarketer reports. And nearly six of ten people (58%) have a cashback credit card, according to a survey conducted by Forbes.

Indeed, cashback has become the go-to feature in the card world. And why not? It’s a way for people to make money as they spend money.

More than that, there is short-term gratification that makes reward dollars more satisfying than earning points gathered through frequent flyer programs.

Cashback cards “motivate consumers to achieve a benefit from spending their money with a brand,” Forbes notes. “There’s a psychological pull that most consumers do not — and sometimes cannot — resist.”

A handful of large credit card issuers have taken the idea of cashback to the next level: the quarterly, rotating credit card cashback calendar. The feature is growing more popular with consumers

What is a Rotating Cashback Calendar?

Most credit card issuers apply a flat cashback percentage on general purchases, although some offer higher percentages for certain qualifying purchases. However, at least two credit card issuers are offering 5% cashback on a special categories of products that the issuers select. These categories earn the high cashback rate for one quarter and then revert to a normal rate.

The cashback calendar can be a great feature for financial institutions and customers alike. But, the benefits aren’t as clear-cut as they might appear — for either party.

Learn More: Innovation and Inflation: Two Trends Changing Credit Card Marketing

Which Card Issuers Use Rotating Cashback Calendars

One-fifth of consumers prefer a credit card with a rotating cashback calendar over flat-rate cashback cards or even tiered 3%/2%/1% reward cards, according to a Kantar report. Especially as the price of gas and other consumer items rise, the rotating cashback calendar has attracted the attention of credit card holders.

To top it off, “the most likely to select the 5% rotating category rewards are two of the top segments for which issuers are fighting: Millennials and affluent consumers,” Kantar finds.

Oddly enough, only two card issuers actively offer such a program to consumers at present: Discover with its Discover It and Discover More credit cards and Chase with its Chase Freedom credit card. (Citi also offers a quarterly cashback card — the Citi Dividend Card — but it is currently available only to existing Citi customers.)

What’s even more interesting is that Chase and Discover take very different approaches to the cashback calendar feature.

For instance, Discover’s rotating categories don’t change much from year to year. The company alternates through quarterly rewards, which fit seasonal themes. For instance, in 2022, Discover promises 5% cashback according to the following schedule:

- January–March: Grocery stores, fitness clubs and gym memberships

- April–June: Gas stations and Target

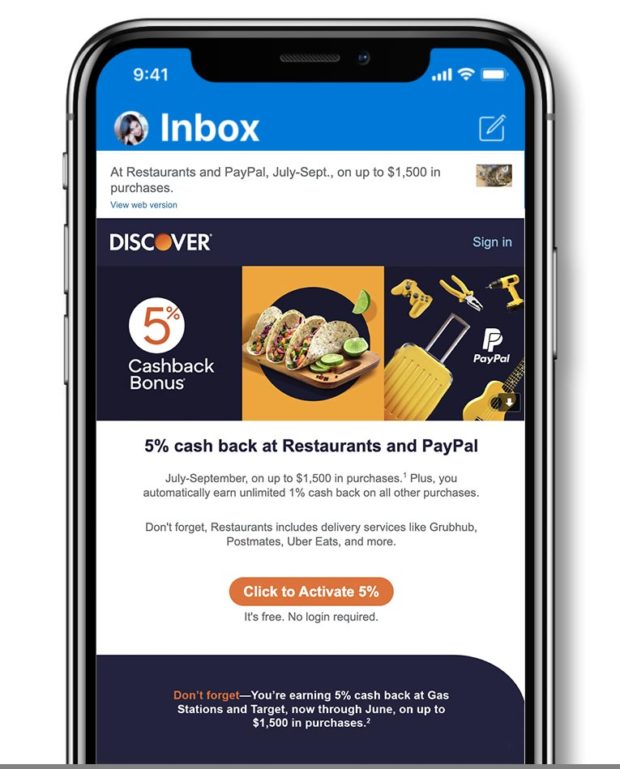

- July–September: Restaurants and PayPal

- October–December: Amazon.com and digital wallet purchases

The spending categories in the first three months are designed for New Year’s resolutions — or as Discover puts it: “to refresh your health and fitness routine.” The next three months are for early spring trips and getting-ready-for-summer purchases. The third quarter is meant to reward cardholders for eating out in the summer while the last three months of the year help kick off holiday shopping.

With Discover’s offer, the cashback maximum taps out at $75 every quarter and there are no retroactive rewards. Customers must activate the 5% cashback before the start of the next quarter to earn all their rewards.

Chase announces its quarterly categories only a few weeks before the quarter begins. For the summer of 2022, Chase is offering 5% cashback on up to $1,500 worth of purchases at gas stations, car rental agencies, movie theaters and “select live entertainment.”

Previously, Chase has offered the following cashback categories:

- Q2 2022: Amazon.com and streaming services

- Q1 2022: Grocery stores and eBay

- Q4 2021: Walmart and PayPal

Unlike Discover, Chase says customers can get cashback on purchases they already made if they activate that quarter’s cashback savings at least two weeks before the quarter ends.

Dig Deeper: It Takes More Than Convenience to Acquire Credit Card Users

Why Consumers Might Hesitate to Use Cashback Calendars

Cashback rewards are also not taxable, so the funds cardholders earn can go toward paying off their existing credit card debt or other purchases. Since customers can earn even more reward dollars with a rotating cashback credit card, these cards would seem like an easy win.

However, they are not always the best option. One reason: Activating the categories every quarter can be difficult for the average cardholder to keep track of — a challenge that would inevitably fall in the hands of marketers.

“It’s easy with a flat rate card, whether you get 1%, 1.5% or 2% back. You don’t really have to think about what category you’re spending in,” Consumer Finance Analyst Beverly Harzog tells Time. “If you’re a person that doesn’t mind planning your purchases and which cards to use for different purchases, then that’s where the categories come in.”

Keep in Mind:

Rotating cashback calendars could frustrate consumers if there aren't reminders to activate the cashback.

Casey Merolla, a Managing Director in Accenture’s payments practice, agrees, pointing out that financial institutions must be wary of the customer experience.

“While the concept of rotating cashback credit cards sounds nice on paper, it can be hard for customers to follow the category changes,” Merolla explains. “Most cardholders want to just ‘set and forget it’ versus having to pay attention to rewards category changes each month or quarter.”

To avoid that problem arising, Chase says its customers can sign up for email reminders and Discover also notifies people via email to let them know they have an upcoming activation.

Read More: Over 50 Credit Card Trends & Statistics for Banks

Read More: Over 50 Credit Card Trends & Statistics for Banks

Should Banks Be Hesitant about Cashback Calendars?

The customer experience isn’t the only concern associated with rotating cashback calendars. Merolla says integrating this credit card feature is not as easy as the megabanks make it look. Rotating various reward algorithms requires more resources than a stationary rewards program — especially if the bank’s backend technology isn’t up to date.

“Under some of the legacy card processing platforms used by banks, the process to change the reward categories is actually a more complicated process than one might think, making it difficult to make frequent program changes,” she tells The Financial Brand.

There are also big-picture consequences to consider. For one, higher cashback rates could contribute to inflated prices of consumer items.

“Every time a credit card is swiped, the bank charges a fee,” argues Emily Stewart from Vox in a feature on who ultimately pays for cashback rewards. “It seems trivial, but those fees add up — enough to help pay for rewards like points-funded hotel rooms and cashback. To compensate, businesses raise prices, and so cash users (who tend to be poorer) are often subsidizing the perks going to credit card users (who tend to be richer). And the higher the rewards, the bigger the cost to the unsuspecting people paying for it.”

A Downside to Cashback Calendars:

Cashback is a great short-term reward, but it also contributes to price increases on consumer products.

There is no data currently available to indicate whether the interchange rates are higher on Discover and Chase’s rotating cashback credit cards specifically. However, issuers offering credit cards with rewards generally charge higher interchange rates.

“Rewards cards pay for the perks given to cardholders by charging higher interchange rates to businesses,” merchant software provider Big Commerce wrote in a blog post, adding these higher rates can be offset for merchants by the incentive for customers to purchase more.

The Benefits of Rotating Cashback Calendars for Banks

The above considerations notwithstanding, there are advantages to banks and credit unions adopting versions of a rotating cashback calendar. As Investopedia points out, credit card issuers can make the money back through higher merchant fee volumes.

“The goal is to incentivize people to use their credit cards when making payments rather than cash or debit cards, which earns them no rewards,” Investopedia says. “The more a consumer uses a credit card, the more merchant fees the credit card company can earn.”

Offering a cashback card that changes on a revolving quarterly basis also provides opportunities for further product marketing. Most websites explaining rotating cashback calendar credit cards to consumers recommend the cardholder pair it with a more traditional, flat cashback rate credit card to use in the “off months.”

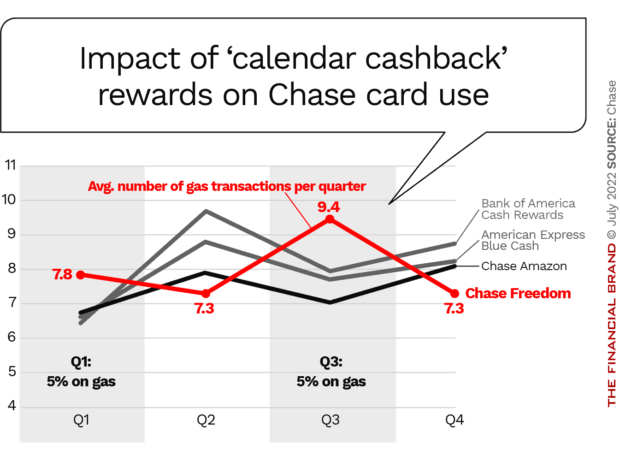

People are taking the advice. Kantar’s report found that among customers who own credit cards with competing card companies, they “appear to use those cards less in a given category when their respective 5% cards are promoting that category.”

For instance, when Chase offers 5% cashback on gas, Kantar found its cardholder’s usage jumped significantly during that quarter — even if that customer uses a competing card more the rest of the year.

Offering a rotating cashback calendar can also be an excellent method for cross-selling. If customers check your bank or credit union’s website four times a year to activate their cashback for the quarter, that means additional touchpoints with your institution’s brand, website and app.

How Banks Could Introduce Cashback Calendars

Merolla says if a bank does decide to roll out a rotating cashback card, she would recommend building a product with a personalized customer experience.

“Creating a rotating cashback card that automatically calculates a customer’s top spending category and offers extra points within that category would be a good focus area for banks,” she says.

This can be costly, however.

“It takes the highest spend categories and offers cashback versus offering cash back on categories where the banks are trying to encourage additional, incremental spend to further engage customers in their card products and obtain ‘top-of-wallet’ status,” Merolla observes.