If there was any doubt that the “buy now, pay later” (BNPL) phenomenon is here to stay consider this: The nine-year-old fintech company Affirm now originates close to $1 billion in loans annually solely for upscale exercise equipment company Peloton.

That one client relationship accounted for 28% of Affirm’s total revenue for fiscal 2020, which amounted to $1.2 billion. Affirm also claims as clients Verizon, Expedia, Warby Parker, and Walmart.

Notably, 48% of Affirm’s total customers are Millennials and the portfolio’s average credit score is about 740 — indicating that BNPL users are relatively young, established and creditworthy.

Several studies demonstrate that BNPL is a trend on the rise, and financial institutions must react quickly if they are to compete with the many fintechs providing such services — including Affirm and Klarna — but even more so because of the payment and tech giants in the game including market leader PayPal.

“Banks that underestimate the threat may see continued loss in share and could lose out on participating in a growing value pool … among younger and new-to-credit customers,” according to a McKinsey report. “To avoid that outcome, U.S. banks need to understand the landscape for POS financing and choose from among the emerging models.” (“POS lending” is another term for “buy now, pay later.”)

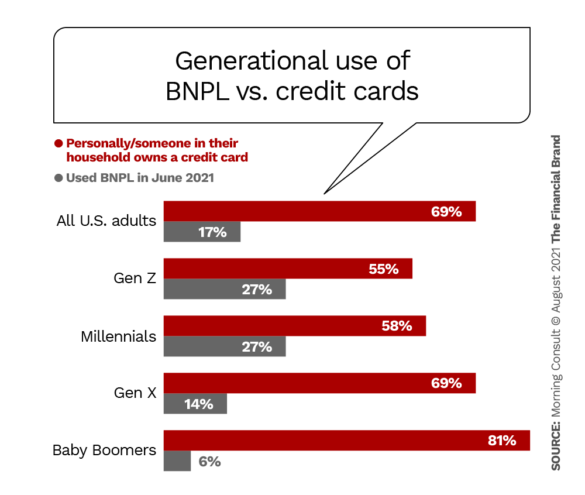

A survey of 4,400 U.S. adults by Morning Consult confirms how interest in BNPL skews toward the key Millennial and Gen Z segments, which are also so less likely to own a credit card than older adults.

“BNPL providers offer what can be a superior consumer experience compared to traditional credit solutions, which includes real-time approval processes, simpler and tech-savvy user experiences, and transparent pricing terms including 0% APR,” says a massive report on this industry by Financial Technology Partners (FTP).

Eye Opener:

If you question the staying power of BNPL, consider that Amazon has its own offering, called “Amazon BNPL,” in which consumers pay one-fifth of the purchase price on eligible products up front, then the rest in equal, interest-free amounts over four months.

BNPL Growth Surging Ahead

The FTP report estimates that the total market potential for BNPL in the U.S. is about $5 trillion, which accounts for about 20% of the global market. “The Covid-19 pandemic has accelerated the shift to BNPL as commerce increasingly moves online and consumers look for ways to better manage their finances,” the report states.

Globally, FTP indicates that BNPL will jump from 2.1% of all payment methods to 4.2% in 2024, while most other payment methods decline. One exception is digital/mobile wallets, as shown in the table below.

Global ecommerce payment methods

| 2020 | 2024 | |

|---|---|---|

| Digital/mobile wallet | 44.5% | 51.7% |

| Credit card | 22.8% | 20.8% |

| Debit card | 12.3% | 12.0% |

| Bank transfer | 7.7% | 5.3% |

| Cash on delivery | 3.3% | 1.7% |

| Charge and deferred debit card | 3.3% | 1.6% |

| Buy Now Pay Later | 2.1% | 4.2% |

| Direct debit | 1.2% | 1.0% |

| Pre-paid card | 1.1% | 0.5% |

| Postpay | 0.9% | 0.5% |

| Prepay | 0.4% | 0.2% |

| Other | 0.4% | 0.4% |

Source: FIS, Financial Technology Partners

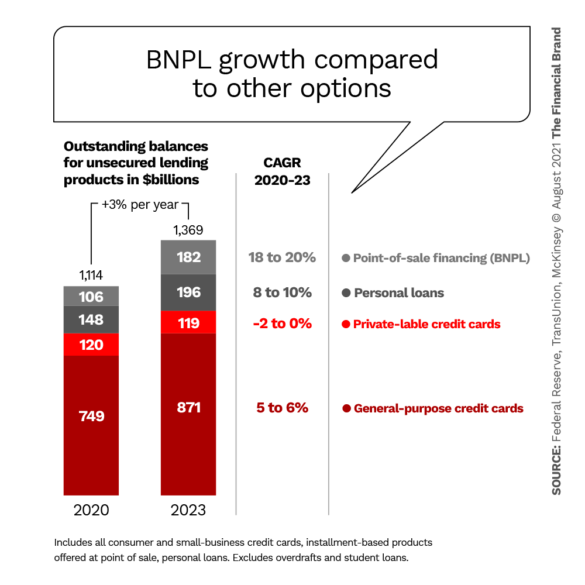

In the U.S., credit originated at the point of sale is projected to continue its growth from 7% of unsecured lending balances in 2019 to 13-15% of balances by 2023, according to McKinsey. Further, a joint Credit Karma/Qualtrics survey found that 42% of Americans already have used some sort of BNPL service.

The FTP report tabulates and analyzes dozens fintechs in the U.S. and abroad that are making inroads in the American market, as well as numerous partnerships between legacy financial institutions, large tech players, and BNPL solution providers. The list includes Mastercard, Amazon, Shopify and Fiserv, among others.

More Big Players Are Jumping In

Incumbent financial institutions like Chase, Citi, Citizens Bank and American Express have introduced BNPL products since late 2020. These moves have been followed by other announcements, including:

- Square announced it is acquiring successful Australian BNPL company Afterpay.

- Visa will collaborate with i2c to launch POS installment capabilities for participating issuers in North America.

- Apple, working with Goldman Sachs as a lender, is expected to announce a new BNPL product tentatively called Apple Pay Later toward the latter part of 2021 — a development analysts deem a potential game changer.

“It seems everyone is getting into the BNPL boom. What was started by fintechs now has credit card issuers, payment firms and banks clamoring to get in.”

— Alyson Clarke, Forrester Research

“Apple Pay Later has the potential to fuel even greater disruption since, unlike other offerings, it’s poised to relocate a line of credit to another financial institution,” write SRM’s Myron Schwarcz and Larry Pruss in a blog.

“It seems everyone is getting into the BNPL boom,” says Alyson Clarke, Principal Analyst at Forrester. “What was started by fintechs, such as Affirm, Afterpay, and Klarna, now has credit card issuers, payments firms, and traditional banks clamoring to get in on the act.”

What’s clear is that U.S. consumers and merchants are demanding BNPL options. McKinsey found that about 60% of consumers say they are likely to use POS financing in the next six to 12 months. Merchants see BNPL as a means to enhance cart conversion, increase average order value, and attract new, younger consumers.

Revenue Drain:

McKinsey: Banks have lost about $8 to $10 billion in annual revenues to BNPL fintechs.

Many Iterations of BNPL Exist

The BNPL landscape has numerous variants. Some providers adhere to the “pay-in-four” model. It’s not unlike the old-fashioned layaway plan, only the customer gets the product right away with minimal credit checks and pays for it interest-free over four months.

Alternatively there is the higher average order value model for products that could cost in the thousands of dollars, in which the consumer is pre-qualified, selects a payment plan from six months to three years, and may or may not be charged interest. Many variations on these schemes exist, including who pays the interest, how the terms are applied, and how thoroughly customer credit checks, if any, are conducted.

McKinsey expects the “pay-in-four” likely will become most common, for four reasons.

1. BNPL providers are turning into shopping apps. For example, shoppers can use the Klarna app or website to buy products on Amazon, even though Klarna is not available at Amazon’s checkout.

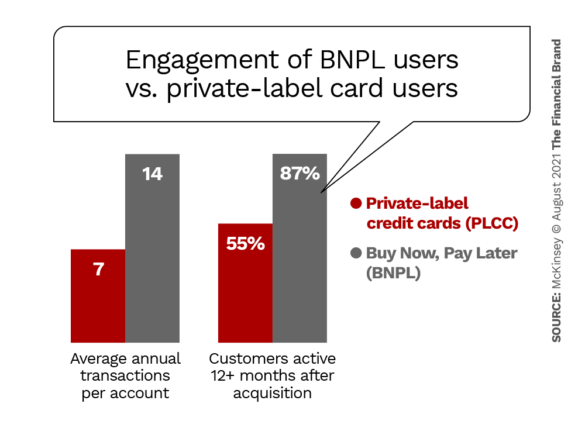

2. These providers drive potential customer engagement and access in prepurchase journeys through enhanced rewards programs and newer features. The chart below illustrates an aspect of this greater engagement.

3. The providers can treat the merchant checkout as a low-cost consumer-acquisition channel, and can cross-sell traditional banking products while gaining advertising revenue.

4. Advanced technological capabilities can protect against potential fraud through powerful underwriting systems.

Read More: 8 Fintech Trends Changing Banking Forever

Still Big Potential for Financial Institutions

Several observers see financial institutions uniquely suited to the BNPL landscape. “The banks bring a stability and cost of capital advantage that BNPL fintechs cannot replicate,” says Adam Hughes, CEO of the BNPL provider Amount, interviewed in the FTP report.

Amount specializes in partnering with U.S. financial institutions. “Banks are looking for solutions to compete with the Affirms and Klarnas of the world who have targeted their merchant partners and credit card portfolios,” Hughes observes.

McKinsey points to three key consumer credit issues traditional financial institutions need to address if they are to compete successfully in the BNPL market:

- Product-agnostic delivery of credit. “The lines across traditional credit products are already blurring, as banks offer loans against open credit card lines and fintechs offer installment-based credit cards or debit cards with pay-in-four features.”

- Integration and engagement across the purchase journey. “Integration at checkout alone will not be enough, as the providers not offering incremental value to the merchant in prepurchase journeys will get commoditized.”

- Expectation of subsidized credit and enhanced value. “U.S. banks might imitate Australian banks that have launched interest-free credit cards to address the expectations, set by pay-in-four providers across the younger consumer base, that credit can be accessed at 0% APR.”

The McKinsey report concludes with this admonition: “Moving fast to have a clear strategy and some path to enter and play in this market will be critical…Starting to make investments to address this trend should be on every banking player’s strategic road map.”