Organizations in all industries are battling for customers based on providing a superior customer experience. The banking industry is no exception. In fact, as digital banking applications have grabbed a greater share of customer transactions, the need to provide an easy-to-use, frictionless experience, with new digital services offered across a greater number of touchpoints has never been greater.

To satisfy these increased expectations, financial technology firms (fintechs) have entered the financial services marketplace. While most of this competition has not achieved significant scale, that shouldn’t signal that these solutions are not important to the industry. In fact, nearly one-third of banking customers have a relationship with at least one non-traditional firm.

According to the World Retail Banking Report 2017, published by Capgemini in conjunction with Efma, fintech firms are more likely than traditional banks to provide consumers with positive banking experiences. That said, more collaboration than ever is taking place between banks and fintech firms, leveraging the benefits that each can bring to the table to create customer-centric solutions. This collaboration has lead to the emergence of Open Banking and APIs, using customer data and innovations to create new revenue streams and more contextual services.

“Fintechs are now earning higher positive customer experience scores than traditional banks, and banks are openly seeking to collaborate with fintechs,” said Anirban Bose, Global Head of Banking and Capital Markets, Capgemini. “Open Banking offers banks an opportunity to retain and grow their customer base as they add the varied services of third parties to personalize and customize products and services. For banks that don’t think strategically and establish a role in Open Banking, there is a chance they will be disintermediated from their customers.”

The Evolving Relationship Between Banking and Fintech

The emergence and acceptance of digital technology caught the banking industry flat footed. After decades of being able to dictate the products, services and channels the customer would use to transact banking business, the consumer took control of the relationship almost overnight, expecting the same simplified interactions offered by firms like Google, Amazon, Facebook and Apple (GAFA).

Without the legacy technology and outdated processes of a traditional financial institution, fintech firms quickly identified a large number of narrowly focused solutions that would leverage consumer data, advanced analytics and digital technology for an improved customer experience. These innovations were welcomed by an increasingly tech-savvy consumer base, especially in the lending and payments product lines. Without the burden of a extensive physical infrastructure, fintech firms were also able to take advantage of significantly lower costs to serve.

According to the World Retail Banking Report (WRBR), while a small minority (2.9%) of consumers do all of their banking with non-traditional firms, more than a quarter (26.5%) use both traditional banks and non-traditional firms. More than one-half (52.4%) maintain relationships with three or more non-traditional firms, while only 7.4% have a relationship with just one. In total, 29.4% of consumers globally use at least one non-traditional firm, with many of these consumers being the most desirable to the traditional banking community.

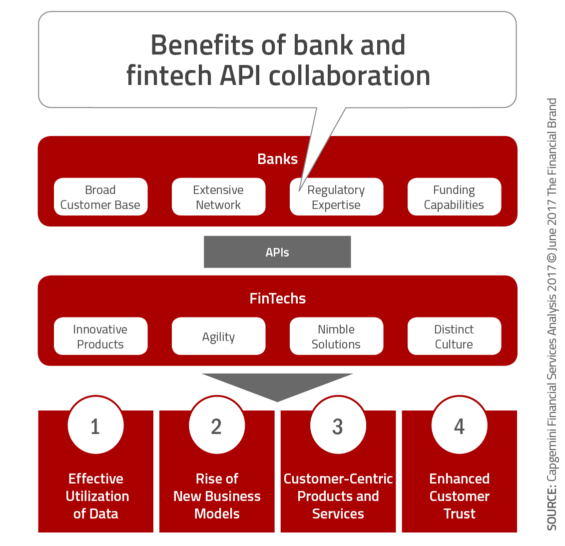

While once considered a formidable threat, the largest traditional banking organizations now view fintech firms as potential collaborators, bringing agile processes, an innovative culture and much needed technological expertise to the table. Many fintech firms have come to realize that traditional banks have a better knowledge or regulations, greater access to capital and the scale of customer base needed to be successful.

This year’s WRBR quantified the robust appetite for closer partnerships between fintech firms and banks going forward. The vast majority of banks (91.3%) and most fintech firms (75.3%) say they expect to collaborate in the future, with banks providing access to their broad resources, experience and expertise, and fintech firms offering agility, speed to market and a fresh take on customer-centricity. By working together and taking advantage of APIs, banks and fintech firms can leverage their complementary strengths, enhancing the customer experience much more than each entity could do on its own.

According to the WRBR, “Given the pressures of cost, regulation and fast evolving customer expectations that banks are already struggling with, there is only so much that can be focused on at the same time. This makes the option of partnering with a fintech highly attractive for banks.” This realization has opened the door for the emergence of Application Programming Interfaces (APIs), which can bring together the power of customer insight and fintech innovations.

Read More: Insights from 9 Global Banking and Fintech Innovation Leaders

The Benefits of Open APIs

While APIs are not new to banking and are nothing more than a structure for how software applications should interact, they provide the gateway for innovative, contextual solutions that would be difficult to offer without Open Banking. As outlined by the WRBR, there are three types of APIs:

- Private APIs: These are APIs that are used within the traditional banking organization, reducing friction and enhancing operational efficiency. A vast majority (88%) of banks viewed private APIs as essential in 2015.

- Partner APIs: These are usually between a bank and specific third-party partners, enabling the expansion of product lines, channels, etc.

- Open APIs: In this scenario, business data is made available to third parties that many not have a formal relationship with the bank. Because of the structure of open APIs, many banks have a greater concern around security.

Most banks ease into the use of APIs, moving from private, to partner and sometimes to open APIs. It is believed that, over time, APIs will evolve to the more extensive options in response to the consumer desire for greater digital solutions not currently provided by legacy organizations. This will also occur as both fintechs and traditional banking organizations understand that they need each others strengths. This collaboration will enable both banking organizations and fintech firms to offer more to customers than previously possible.

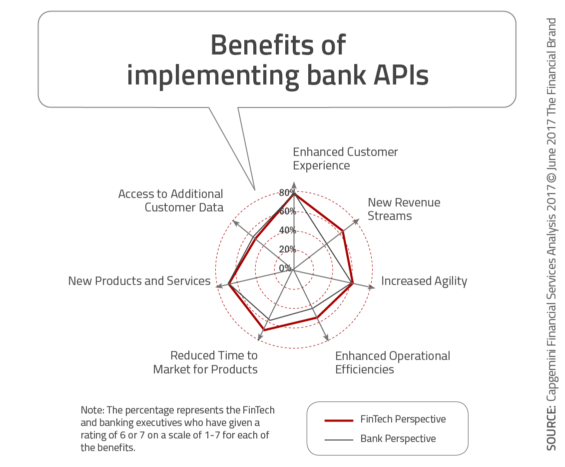

APIs can help banks pursue new distribution channels, while also finding new ways to improve the customer digital banking experience. In addition, the product development process can occur more quickly, responding to rapid changes in digital technology and capabilities (voice banking, P2P, loan processing, risk management, etc.). According to the WRBR, 78.3% of banks are counting on APIs to help them improve the customer experience, with fintech firms agreeing. They also agree that new revenue streams are possible.

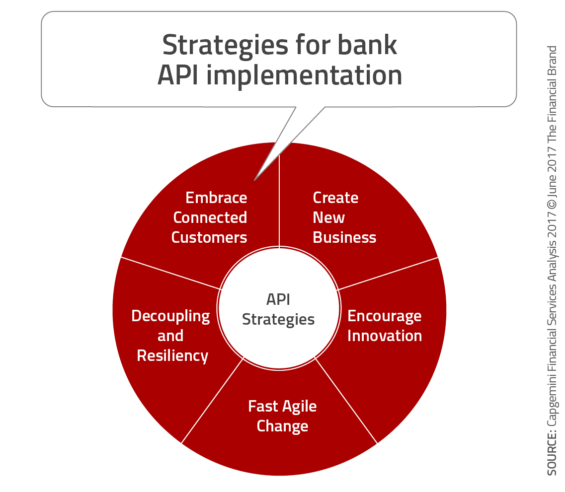

Alternative API strategies could include:

Alternative API strategies could include:

- Create new businesses: Increase the reach and depth of product lines or segments

- Encourage innovation: Facilitate innovation not possible with internat resources

- Increase speed of change: By breaking down silos, APIs can improve speed to market

- Decoupling platforms: Rejoining platforms through APIs reduces cost of development

- Embrace IoT future: APIs can allow for a future where the consumer is identified by their device

“The most successful banks will use open APIs to generate new customer insights and revenue streams, while also improving customer experience,” said Vincent Bastid, Secretary General, Efma. “Many banks currently use APIs internally to improve information flow between legacy systems. In fact, we are already seeing early adopter banks asserting their role in Open Banking by proactively making their systems and data available to third parties and creating new revenue streams.”

Read More: Finding Your Financial Institution’s ‘New Normal’ CX

Open APIs, Big Data and Machine Learning

Open APIs will enable banking organizations to gather actionable data from various internal and external sources, including buying habits, financial goals, rick tolerance and even social interactions. Insight derived from this data will enable more proactive (and accurate) multi-channel marketing, moving from reactive sales pitches to proactive solutions and advisory services. In other words, the difference between ‘rear-view mirror’ notifications and ‘financial GPS’ recommendations.

The ability to apply machine learning and artificial intelligence will respond to the customer desires of “Know me”, “Look out for me” and “Reward me.” This is expected to greatly improve the customer experience which currently lacks personalization and real-time engagement.

The Future of Banking in an Open Banking API World

The future of open banking and APIs does not need to be limited to simply a vertical enhancement of what already exists. In fact, the potential of open banking APIs extends far beyond traditional banking, to include all of the services a consumer may want in a digital world. As mentioned in the WRBR, “Banks that open up their APIs to a global community of web developers can tap into a stunning amount of innovation.”

Open banking presents opportunities for creating and distributing a wide variety of both financial and non-financial products and services – with the banking retaining the customer relationship – but greatly expanding the number and variety of services to improve the customer’s quality of life. In an open banking model, an unlimited number of partners could insert themselves into the relationship development process.

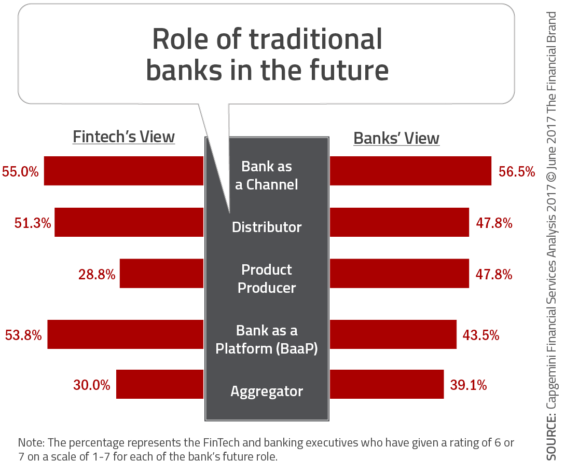

Both fintech firms and banks see the traditional bank continuing to be the primary channel for banking services. The question is whether banks are the best to control innovation or even distribution. While neither banks or fintech firms see banks as aggregators of services, this should be a concern as large tech firms are continuing to encroach on the aggregation role. Losing control of the customer experience could lead to the loss of the customer.

“Perhaps the greatest risk of open banking is that it will allow consumers and merchants to execute direct transactions without going through banks, making it more difficult for banks to have a full view of the customer transactions and maintain customer relationships,” states the WRBR. It is hoped that the open banking concept can avoid this demise, as traditional banks and fintech firms work together to build the customer’s trust and offer products and services that will improve a consumer’s lifestyle.

The foundation of these partnerships will be the data that can be collected and cultivated for the benefit of the customer, the bank and the fintech firms. If applied diligently, the improvement in customer experience could be the differentiator that retains the overall banking (and non-banking) relationship.

The World Retail Banking Report 2017 Methodology

This year’s World Retail Banking Report explores how APIs foster business and technology outcomes that enable productive collaboration among diverse stakeholders. It features data from a global survey and interviews with senior executives from 126 banks and fintech firms.