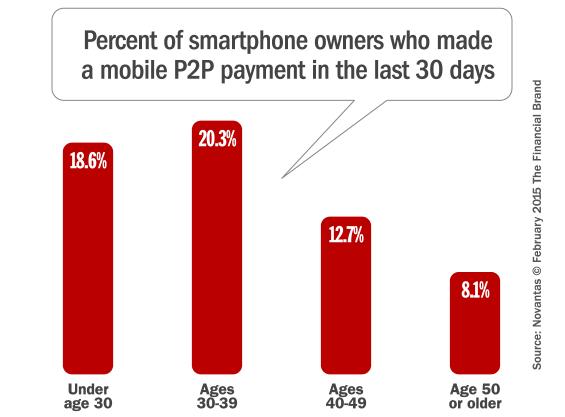

The percentage of smartphone owners that have made recent P2P payments has grown by 23%, up from 13% to 16% in one year. It’s understandable if you assume that P2P appeals to mostly Millennials — roommates sharing housing expenses, restaurant bills and similar situations. But the results of a recent survey on FindABetterBank indicate that smartphone owners aged between 30 and 39 are the most likely age segment to take advantage of mobile P2P services.

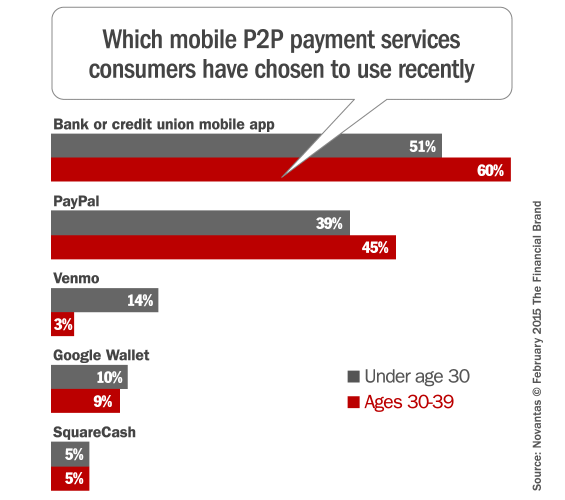

One explanation for the slightly lower use among Millennials compared to consumers that are slightly older is that most P2P services require a checking account or credit card. And there are other trends we see emerging when further investigating which P2P services are most popular with younger Millennials vs. those ages 30 to 39 years old.

30 to 39 year olds are most likely to use a P2P service provided by their bank or credit union. These consumers are 18% more likely to use a P2P service provided by their banking institutions, and 15% more likely to use PayPal’s P2P service vs. Millennials.

Millennials are more willing to use third party services like Venmo. Part of this is marketing. Venmo’s pitch is geared to Millennials and as a result, these young consumers are significantly more likely to use the service. However, P2P services proved by banks and credit unions are far more popular with Millennials than third-party services including Venmo, Google Wallet and Square Cash.

Even though it appears like banks and credit unions are winning today, it’s still early for P2P in terms of facilitating P2P transactions. However, PayPal is already the single dominant provider. What would happen if PayPal started taking deposits and offered more banking services? Banks and credit unions must win the P2P battle by actively promoting P2P services to customers, tightly integrating the capability into mobile apps and competing on price with third parties.