Just when financial marketers feel like they’ve got Millennials pretty well pegged, a closer look reveals that there’s more lurking behind the usual stereotypes. In fact, some assumptions about this huge demographic that have been accepted as gospel may be leading some banks and credit unions down the wrong road. Or at least a bumpier one.

Let’s take the widely held belief that Millennials want digital, all-digital, all the time — that they wouldn’t be caught dead in a branch. Everybody knows that, right?

Research from the Bank Administration Institute (BAI) takes a sledgehammer to this Millennial myth, and many others.

When BAI researchers asked three different generations — Millennials, GenXers, and Baby Boomers — what their priorities were when shopping for banking services, most of Millennials’ top choices are no surprise. They want good points and rewards, and a financial institution with a solid brand reputation.

But the top priority for Millennials? Convenient branches. And Gen Xers said the same thing.

| What consumers are looking for when evaluating banking products and other retail financial services. | ||

|---|---|---|

| MILLENNIALS | GEN X | BOOMERS |

| 1. Convenient branches | 1. Convenient branches | 1. Best products/rates |

| 2. Cash incentives and/or rewards |

2. Best products/rates | 2. Cash incentives and/or rewards |

| 3. Positive brand reputation |

3. Cash incentives and/or rewards |

3. Convenient branches |

| 4. Large ATM network | 4. Large ATM network | 4. Superior experience |

| 5. Superior experience | 5. Superior experience | 5. Positive brand reputation |

| 6. Best products/rates | 6. Lowest fees | 6. Lowest fees |

| 7. Lowest fees | 7. Positive brand reputation |

7. Large ATM network |

| 8. Superior digital capabilities |

8. Superior digital capabilities |

8. Superior digital capabilities |

| 9. Family/friend recommendation |

9. Family/friend recommendation |

9. Family/friend recommendation |

Source: BAI © 2018

“Most people think Millennials don’t care about branches, that they only care about digital,” observes Karl Dahlgren, Managing Director at BAI. “But branches rank highly with them.”

Equally surprising is that all three generations ranked superior digital capabilities near the bottom when listing their priorities.

What lies behind these seemingly surprising findings?

Byron Marshall, BAI’s Director of Research, believes he has the explanation.

“Digital is just table stakes,” he said.

Today consumers assume a bank will offer good digital access to accounts. They also assume that as new channels evolve, old ones will remain available.

While digital is table stakes, that doesn’t mean it isn’t important. Marshall says that if an institution’s digital access is poor or virtually nonexistent, that will count heavily against it. In fact, according to his associate, Mark Riddle, Director of Research and Content Delivery at BAI, half of all Millennials would switch to another bank or credit union if they heard it offered a digital app that was superior to the one they were using at their current banking provider’s.

BAI’s research again battered popular misconceptions about Millennial’s preferences and usage patterns when it comes to retail banking channels. When looking at the average interactions each generation had with typical services, Millennials used mobile banking almost twice as much as they reported using a branch or a drive-up station. But that’s only part of the picture.

Reality Check: Millennials use branches and drive-ups more in a month than either GenXers and Boomers.

Read More: Branches Refuse to Die – Millennials Seeking Loans Visit Branches Most

| Average interactions per month |

MILLENNIALS | GEN X | BOOMERS |

|---|---|---|---|

| Total | 72.2 | 60.7 | 44.3 |

| Mobile banking | 9.2 | 7.9 | 2.5 |

| Credit card | 7.8 | 6.3 | 5.5 |

| In-person at branch/drive-up | 4.7 | 2.9 | 3.2 |

| Mobile check deposit | 2.9 | 1.9 | 0.3 |

| Personal check written | 2.8 | 2.5 | 3.3 |

| Phone call with live agent | 1.9 | 0.9 | 0.8 |

Source: BAI © 2018

In fact, in all but one category of service, Millennials use their primary financial institution’s services — from physical to digital — more in a month than any other generation.

“Millennials are using nearly every channel more,” Dahlgren notes. “It’s a generational thing.”

Boomers, Dahlgren explains, hark back to a time of “banker’s hours” and in-branch paycheck cashing. To them a weekly trip to their financial institution — often on Fridays — was the limit of their interaction.

By contrast, he continued, Millennials have grown up with both information and services always being readily available — from banking apps to movies on Netflix.

“That’s just what their patterns are,” Dahlgren says. Digital access hasn’t negated the desire for other channels, at necessary times.

On top of that, Millennials and others today have an appetite for “instant gratification.”

“There’s an insatiable need for information to help people with general financial awareness,” Dahlgren points out.

An interesting ripple effect of the growing number of channels, and the fact that “consumers keep using all of them,” says Riddle, is that institutions’ call centers are growing, not shrinking.

“You need more people to answer the questions that each new channel is creating,” said Riddle.

Cross-Selling Potential vs. Reality

BAI’s findings were part of a broader research project concerning how financial institutions acquire and retain consumer relationships across generations, and then cross-selling that base.

Broadly, consumers’ primary financial institutions have some degree of “home court advantage,” but not nearly the leg up that they’d like to think they have.

Respondents were asked if they would give their main provider all of their future deposit business — 45% said yes, with results similar among the generations. That finding came in more positively than what surveyors heard about investments and loans.

Respondents were asked if they would give their main provider all of their future deposit business — 45% said yes, with results similar among the generations. That finding came in more positively than what surveyors heard about investments and loans.

Regarding investments, only 26% would give their primary financial institution all of their future investment business. Millennials were slightly higher, at 29%.

Older generations still tend to divide their financial relationships into two camps — banking products vs. brokerage products — and separate their respective business accordingly, and almost always with traditional providers. Many financial institutions have told BAI researchers that they have had little- to no success changing how older consumers perceive their brands and manage their financial relationships.

Banks and credit unions face an even steeper challenge in credit. Overall, only one quarter of consumers — including Millennials — say they would always borrow with their primary institution.

Marshall says that all generations are open to borrowing from multiple players, and Millennials intentionally spread their credit business around.

BAI’s Dahlgren blames some of the failure of banks and credit unions to cross-sell more to customers on “stovepiping” — different silos in the institution failing to work with- or even communicate with each other.

According to Dahlgren, this will become a growing concern for institutions wanting more of Millennials’ business because in increasing numbers they will be coming into their inheritances from their Boomer parents. Can many institutions currently say they are prepared for that?

Read More:6 Big Millennial Marketing Mistakes Banking Brands Cannot Afford to Make

Cross-Selling: Not Always a Pleasant Experience

The association’s study found a curious trend. Consumers who had been through the cross-selling process at some point were more likely to move their business to another financial institutions, typically about a year or so later.

“The experience of opening an account was a negative factor in retention,” explains Riddle.

According to BAI’s study, the top ten financial products that consumers feel are the most difficult to open/acquire include:

- Mortgage loan

- Home equity loan/line

- IRA

- Auto loan

- Checking account

- Savings account

- Credit card

- Certificate of deposit

- Money market

- Mutual fund

What’s so unpleasant about opening bank accounts?

“Everything is pretty difficult,” says Riddle.

Dahlgren offers an example: the online application process, which is still a conundrum for many institutions.

“Know Your Customer” (KYC) compliance requirements can be difficult to carry out or off-putting, which does not send a friendly message. Dahlgren says that — having invited consumers in — the typical provider then proceeds to scrutinize them.

Consumers would like to be seen as an opportunity rather than a risk, Dahlgren explains.

Beyond these issues, traditional providers’ processes and systems present consumers with annoying obstacles. When BAI asked survey participants what their main banking provider could do to improve the experience, here’s how they ranked their responses that they felt would have the most positive impact:

- Better omnichannel experience so I don’t always have to start over between channels

- Transform the branches — e.g., experts to help me with my financial goals

- Enhance the mobile channel (like Amazon)

- Give me tools and options to customize my own solutions

- Make better use of the data about me to improve product and service suggestions

- Have more useful, real-time messaging and content for day-to-day banking needs

Boomers and GenXers tend to be less negative about account opening and cross selling than Millennials, in the BAI research. Marshall thinks each generation’s attitude hinges on what they have known. The older a consumer is, the more likely they remember account opening procedures that were even more cumbersome and annoying than what institutions use now. So, Marshall reasons, they see today’s practices as an improvement on their past experiences. Millennials, by contrast, see the same measures as clunky when compared to the customer experience they enjoy with other companies.

Multiple elements go into acquisition, cross-selling, and retention, as described, but one not treated with yet are the front-line staffers that banks and credit unions rely on to make lofty sales goals a reality.

And research among institutions’ staffs indicate that this is also a potential weakness. For example:

- Less than a third of employees strongly agree that they have the training necessary to do their jobs.

- Only half of organizations surveyed take proactive steps to hold onto high performers.

- Less than half of employees know of any leadership development program at their organization.

- Not surprisingly, most HR professionals queried believe their employee turnover is too high.

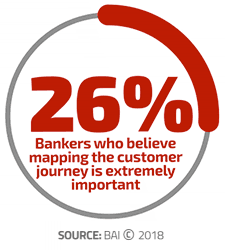

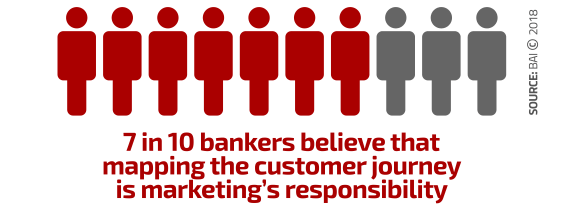

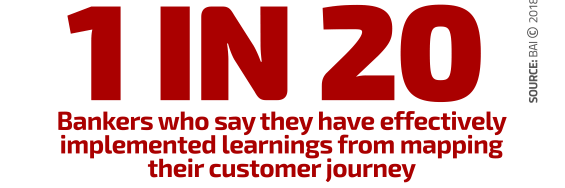

Against these and other weaknesses, there’s plenty of room in the “customer journey” for consumers to fall out. Yet, as the infographic shows, many institutions do little or nothing to figure out where the weak spots lie.

Read More: Generation Z: The Future of Banking