Millennials switch banks twice as often as other consumers. According to an Accenture survey of more than 4,000 retail banking consumers in the United States and Canada, nearly one in five Millennials (18%) said they switched from their primary bank in the past 12 months, compared with 10% of consumers aged 35-54 and only 3% of people 55 and older. Though local/community banks were the biggest winners of this trend, 17% of Millennials who switched chose online-only banks. Surprisingly, slightly older consumers were even more likely to have switched to an online-only bank within the past 12 months, with 31% of consumers aged 35-39 years old saying they did so.

Millennials also have distinct preferences for how banking services should be delivered. Two-thirds (67%) of them said that the traditional and digital banking experience they receive at their current bank is only somewhat or not at all seamless, and nearly half (47%) said they would like their bank to provide tools and services to help them create and monitor their budget. Nearly half (48%) also said they would like their banks to offer video chat on their website or mobile/tablet application, compared to only 30% over 55.

“In 2015, as Millennials overtake Baby Boomers as the largest living generation in the United States, they are becoming one of the most influential — and challenging — consumer groups for the banking industry,” said Robert Mulhall, managing director and North America lead for Accenture Distribution and Marketing Services, Banking. “Not only are Millennials more likely to switch banks, but many continue to migrate to online-only banks, which poses a significant risk for traditional brick-and-mortar based banks in the future.”

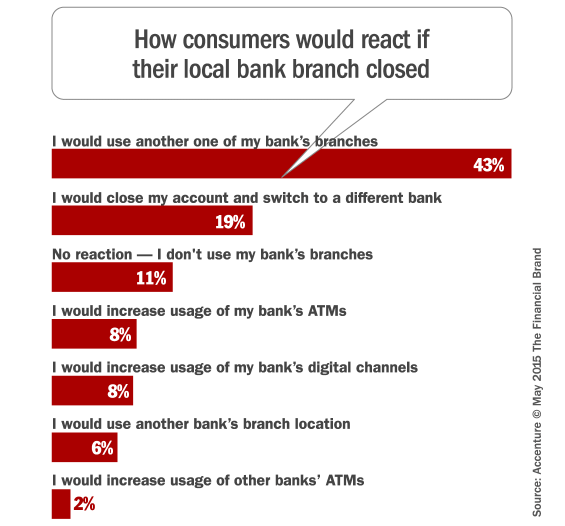

And while many banks and credit unions continue to add branches, Accenture’s research suggests that strategy isn’t the key to growth. An overwhelming majority (81%) of consumers said they would not switch banks even if their local branch closed. This is a significant increase from the 52% of respondents in Accenture’s 2013 retail banking study who said they would be unlikely to switch banks if their branch closed. At the same time, 34% of consumers said that online is the most important channel for banks to invest in over the next five years, followed by mobile (cited by 20% of respondents).

“This is a big change in the evolution of retail banking,” Mulhall said. “For the first time in our research, consumers ranked online banking services as the number one reason for staying with their bank, ahead of branch locations and low fees. It’s no longer a question of proximity to the local branch that is driving consumer choice, it’s a matter of which banks are offering the strongest online capabilities and mobile applications.”

Consumers Trust Their Financial Institution, But Not Enough For Advice

When asked what type of company they trust most with securely managing their data, the vast majority of respondents (86%) chose banks and financial institutions. This is more than 10 times the number of respondents who chose payment companies (7%), mobile phone providers (2%) or consumer technology companies (2%). Only 1% of consumers said they trust social media providers the most to manage their data.

“Despite the many threats that banks face, they still possess competitive advantages that are critical in today’s digital world,” said Dave Edmondson, senior managing director of Accenture’s North America Banking practice. “At the same time, our report highlights several trends that are causing significant challenges for banks and should serve as a call to action for them to focus more on improving consumer perceptions and gaps in their digital offerings.”

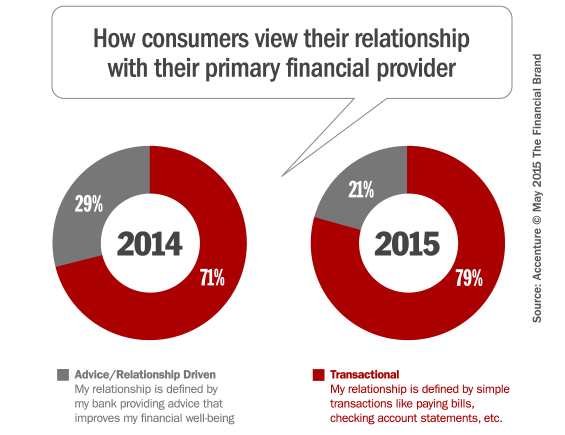

The survey found that most consumers (79%) define their banking relationship as transactional or commoditized, rather than advice-driven and offering high-margin products and services. These consumers said that their relationship with their bank is defined by simple transactions like paying bills and receiving checking-account statements.

Though consumers overwhelmingly trust banks over other types of providers with their data, they are going to competitors for more sophisticated, high-margin products. For example, the majority of consumers said they went to other sources to purchase auto loans (70%), brokerage accounts (61%), retirement accounts (53%), financial advice (52%) and home mortgage loans (52%).

“Consumers’ perception of their banking relationship as transactional and not advice-driven is growing at a rapid pace,” Edmondson said. “Banks run the risk that consumers increasingly view them as a utility — a service for basic financial transactions — and not as the first choice for seeking financial advice. Banks need to become more relevant to consumers’ everyday lives, including recommending suitable products and services, whether these options come from the bank or third parties.”

In the Accenture study, consumers said they would be interested in several value-added services provided by banks, including: discounts for purchases (54%); proactive bill-pay services (53%); product recommendations (52%); end-to-end assistance with car buying, such as help with negotiating a loan and providing vehicle recommendations (49%); and buying a home (46%).

How Financial Institutions Must Shape the Future of Banking

Accenture says that delivering on the expectations of banking shaped by all customers — specifically Millennials — requires an analytics foundation in addition to business and IT integration, agile operating models and strong digital governance. According to Accenture, these fundamentals will be key to deepening customer relationships and intimacy so that banks can deliver the insight-driven experiences that customers want:

Know the customers. Micro-segmentation allows financial marketers to understand customers better as groups, sub-segments and individuals. It guides banks to direct resources, develop products and service customers through individual interaction models and as part of an omni-channel strategy.

Re-imagine the experience. With analytics, banks and credit unions can create consumer-centered journeys that go beyond conventional banking encounters. They can develop test-and-learn approaches, using data insight to inform continuous improvement efforts that reflect customer behaviors and feedback.

Change the distribution mix. Considering the changing role of the branch and the growing importance of digital, financial institutions need to rethink the distribution mix to make the most of consumers’ changing patterns of channel usage.

Deepen and sustain loyalty. Financial institutions can sustain customer loyalty by combining implicit loyalty — advice, matching donations or services

like merchant-funded offers — with explicit loyalty (points based systems), using the right data for an insight- driven, holistic loyalty program.

Evolve into everyday banks. Banks and credit unions must bring multiple elements together—channels, customer experience, analytics, partnerships, digital platforms and innovation among them—to power a new Everyday Bank value proposition.