After being out of favor among lenders for a couple of years, the home equity business is heating up again. Financial institutions that want to deploy the massive surplus deposits they have and not get left behind must step up their digital strategies on this front or get ignored by digitalized consumers.

Traditionally a product many homeowners looked to local branches for, consumers are increasingly applying for home equity lines of credit through mobile and online channels, according to the annual Home Equity Lending Monitor from Phoenix Synergistics.

Financial institutions that don’t adapt to this market preference for digital access, and which also fail to actively cross-sell home equity credit, run the risk of missing out on a lending opportunity that appears to be coming, suggests William McCracken, President at the research firm.

The urgency to move on this is underscored because many institutions remain flush with more money than they know what to do with, he adds. Unlike mortgages, which banks and credit unions typically sell into the secondary mortgage market, home equity credit is generally held by lenders.

Fintechs Could Get Early Lead:

Home equity credit is ripe for disruption by fintechs, which would debut with fully digital application processes.

The fintech Rocket Mortgage (formerly known as Quicken Loans) has already become the largest primary mortgage lender in the U.S. While Rocket doesn’t currently promote home equity credit, something that should prod traditional lenders is that Phoenix Synergistics’ research has found that about three-quarters of home equity line of credit (HELOC) borrowers typically open their credit lines with their primary mortgage lender. And that may no longer be a bank or credit union.

In fact, McCracken says he has been surprised that more traditional financial institutions that offer mortgages don’t take advantage of this tendency. To him, it’s low-hanging fruit that many inexplicably aren’t reaching for. The firm’s study found that only about one out of four homeowners with a HELOC were approached to open a line by their primary mortgage lender. This may reflect the fact that some of the largest mortgage lenders, such as Chase Mortgage, had paused HELOC efforts for a time.

While fintechs haven’t made a significant dent in HELOCs yet, according to McCracken’s data, the planets are lining up for them.

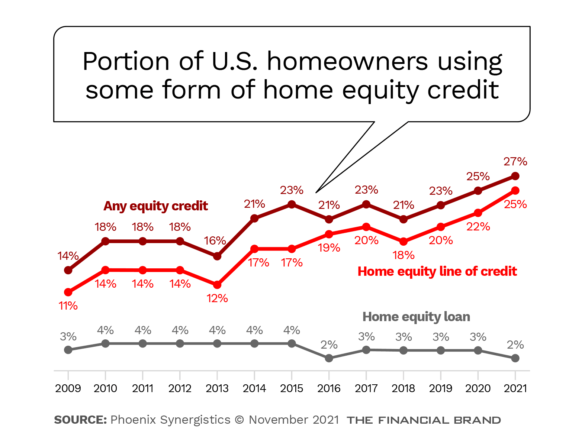

Already, the company’s research indicates that 27% of homeowners surveyed have either a HELOC or a home equity loan. As the chart above illustrates, this is the highest level in years. The credit lines are much favored over the loans for their greater flexibility, according to McCracken.

All these issues come at a point when interest in home equity credit, chiefly home equity lines of credit carrying floating interest rates, are becoming more attractive again.

What’s Favoring a Surge in Home Equity Lines of Credit

In an interview with The Financial Brand McCracken pointed to a number of factors that favor reentry into this business, in a digital way.

A key one is rising home prices.

“If you have had your home for at least a few years, you are equity rich,” says McCracken. “Rather than refinancing to get cash out, you have an opportunity to access an equity line that will let you draw out only as much as you need.”

Nationally, home prices rose year-over-year by 18% in September 2021, according to CoreLogic Home Price Insights. This is partially due to an ongoing housing supply shortage, the firm said. There are areas at risk for price drops. And the high rate of growth won’t go on forever, but McCracken’s point is that there’s equity to be tapped now. He notes that Freddie Mac is predicting a 5.3% rate of price growth for 2022.

Inflation is going to tamp down demand for refinancing.

McCracken says his research indicates that 45% of homeowners have refinanced in the last two years and that another 35% expect to refinance over the next 12 months.

“If that bears out, 80% of all homeowners will have refinanced over a three-year period,” says McCracken. “So that tells you that the pool for refinancing is going to be quite small, because no one will want to refinance as rates are edging up.”

HELOC rates are generally much lower than those of unsecured personal loans and credit card loans, McCracken points out. This will make them attractive for people looking for major personal credit.

Working from home will create additional demand for credit.

While many companies have been trying to bring their staffs back to the office, working from home has become an option for many Americans. McCracken says that now that this trend has gone beyond a temporary measure, more people are looking to beef up their space. This includes home improvements, extensions, additional or better furniture, and more.

“That kind of spending lends itself to home equity borrowing,” says McCracken. A plus for home equity credit is that for people who itemize their taxes the interest can still be tax-deductible, subject to limits, something that you don’t get if you obtain personal loans or rely on credit cards.

Local lenders have enjoyed some advantages in HELOC lending but this time around there may be a limited window of opportunity, according to McCracken.

Opportunistic fintechs are one risk. Another is the return of major league competitors.

At the start of the pandemic some large HELOC lenders were worried about potential risks and shut off the spigot. McCracken thinks they will be opening it wide again.

“I think a lot of the traditional lenders who have been completely on the sidelines or at least taking a less-aggressive marketing stance on home equity are going to realize, ‘Oh my gosh, look at how much wealth is now sitting in homes, and what borrowers could do with the funds’.”

— William McCracken, Phoenix Synergistics

Harvesting HELOC Potential Will Demand Digital Applications

Having a robust digital process for taking home equity applications has become a “must-have,” according to Phoenix Synergistics’ research.

McCracken points to two aspects of the annual study.

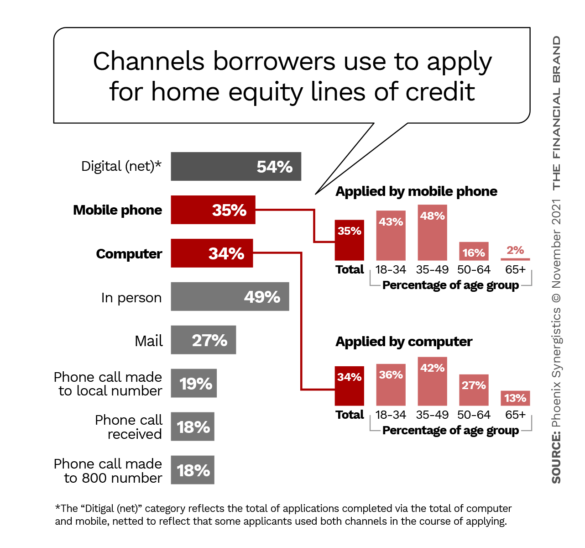

The first are the channels that consumers told researchers that they have actually used when they applied for home equity credit. Applications taken via digital channels have pulled ahead of applications taken in bank branches or other offices. The younger the consumer, the more likely they took either the mobile or online route, or some combination of both.

Read More: How Banks Are Arming to Win the Digital Lending War With Fintechs

What is more dramatic is the way the future is shaping up. The first chart is in the past tense, that is, it is how home equity borrowers obtained their loans, which reflects the way things had been over the last few years.

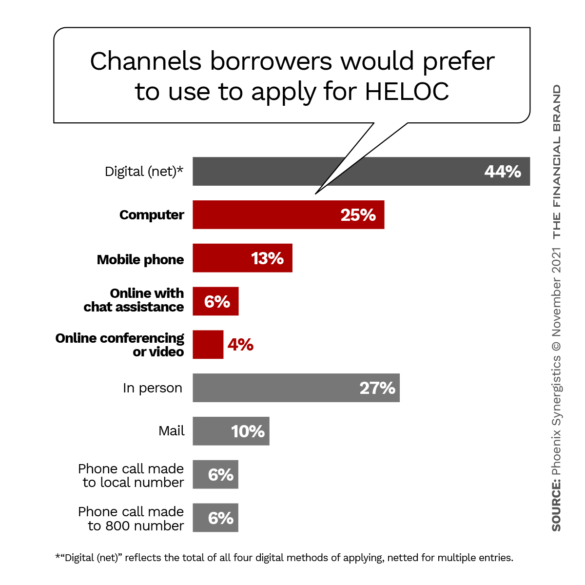

On the other hand, what institutions need to adhere most closely is how people want to apply in the future.

Looked at in this way, willingness to go to an office to obtain home equity credit is dwindling away. Less than a third of the study respondents are willing to do that.

“Home equity credit is really an older product, but it’s kind of in a new package today, in terms of how it’s going to be accessed,” says McCracken. “Instead of going to a branch to talk to someone, it’s gravitating to filling in a form after dinner on your laptop or your phone.”