Few banks in the United States are willing to dabble in the student lending space. That’s because student lending is a risky business. Young students have limited credit history, loan amounts can be substantial and the risk of default is real. Even if students could get their parents to co-sign, many of banking providers – including big banks like BofA and Capital One – won’t touch student loan applications.

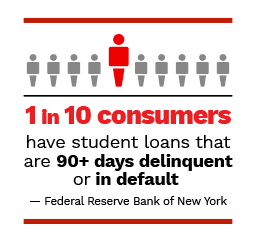

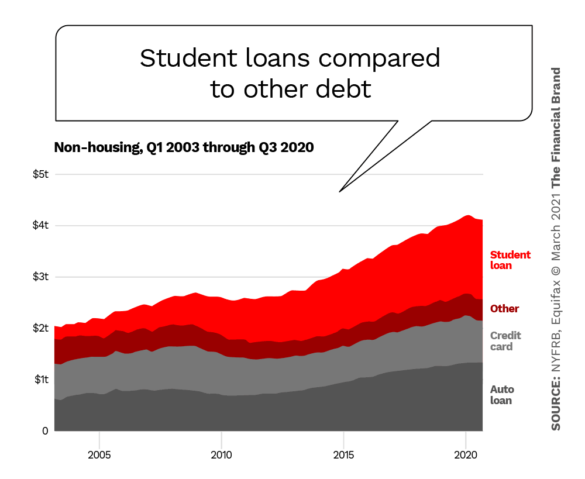

At the start of 2021, over 44 million Americans owed more than $1.71 trillion in student loan debt, amounting to almost 11% of all consumer debt in the U.S. — roughly $739 billion more than the total of all credit card debt.

With the soaring inflation of college tuition, these numbers are only expected to grow.

Big Picture:

While most banks and credit unions dodge student loans directly, their ability to extend consumers credit with delinquent and defaulted debt is seriously diminished.

Major Consequences for Consumers’ Overall Credit Worthiness

Young students will eventually turn into mature consumers with typical borrowing needs for houses, cars, and growing businesses. But the burden of debt looms large in minds of Gen Z and Millennials.

Student loans don’t impact credit scores any more or less than other loans in a credit record. Just like a mortgage, credit bureaus like FICO consider student debt an installment loan and treat it as such. It’s a heavy burden, although when repaid properly, student loans can have a positive effect on credit scores over time.

Unfortunately, most borrowers struggle with their student loans.

“The total individual debt number doesn’t really get to the heart of what people are experiencing,” says Cody Hounanian, Program Director of nonprofit advocacy group Student Debt Crisis. “We hear from borrowers every day who cannot afford their student loan payments, who cannot put food on the table.”

“The total individual debt number doesn’t really get to the heart of what people are experiencing,” says Cody Hounanian, Program Director of nonprofit advocacy group Student Debt Crisis. “We hear from borrowers every day who cannot afford their student loan payments, who cannot put food on the table.”

“The average individual debt is usually somewhere in the $30,000 range, but when you look at the most distressed student loan borrowers who are in default, they are often in the single digits, less than $10,000,” Hounanian said.

(Read More: Understanding How Consumer Borrowing Habits Will Change Post-COVID)

In response to the COVID pandemic, the U.S. government suspended student loan payments through September 2021, making it difficult to predict how distressed these loans may be once the moratorium is lifted. As of September 2020, more than 3 million student borrowers deferred their loans, totaling about $117 billion, according to the National Student Loan Data System.

Clouding the outlook further, progressive lawmakers are advocating that (at least some) student debt should be forgiven. The Biden Administration has proposed a plan that would forgive up to $10,000 of every student’s loans.

However, forgiveness proposals will not make much of a dent in the greater student debt problem, according to recent research from the JPMorgan Chase Institute.

“Our analysis shows that targeting student loan forgiveness by income would be more cost-effective in channeling relief to the hardest-hit families whose circumstances make it difficult to repay and who, in some cases, face a long-term debt trap from their education,” said Co-President Fiona Greig.

Key Question:

With a questionable economic outlook and a shaky job market, will younger borrowers be able to keep their head above water, regardless of whatever federal help they may receive?

Read More: Trend Watch: Young Adults Racking Up Massive Consumer Debt

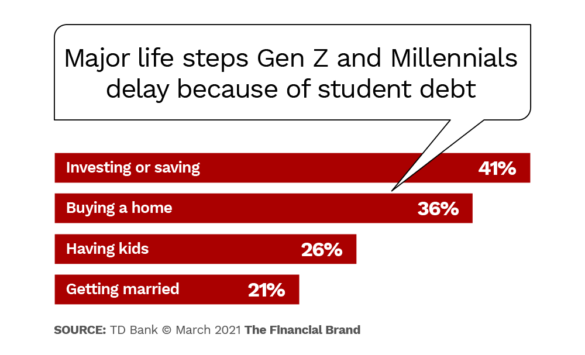

.When TD Bank conducted a study to see how student loans impacted consumers aged 18 to 35, they found one in three delayed buying a home because of their college loan, and a quarter put off having kids.

“Consumers owe money before they even earn their first paycheck, which is troubling.”— Mike Kinane, TD Bank

Mike Kinane, an executive with TD Bank, worries about “the ripple effect” student loans have on borrowers’ financial futures.

“Many Americans are unaware of how student loan debt will impact their lives for the long-term,” Kinane said. “We’re seeing an alarming lack of education surrounding student loans, repayment terms and borrowers’ earning potential after graduation.”

TD Bank’s report on student loans highlighted the problematic trend at its core: Young consumers are putting off big purchases and forgoing new loan applications because they feel like they already can’t keep up with their college loans.

One economics professor with Columbia University predicts that one out of four student borrowers will default on their loan within 12 years of starting college.

Missed payments and default notices on student loans affect credit scores for up to seven years. Considering most students graduate in their 20s, delinquent behavior often haunts people well into their prime career- and parenting years.

Bottom Line:

If people are afraid to take on more debt or if student loan defaults cause consumers’ credit scores to sink, banks and credit unions could see their consumer loan portfolios crumble.

People like 33-year-old Laura Klauser in Chicago said she has no idea if she’ll ever be able to buy a house.

“When I look at the cost of buying a place, especially on my own, it’s not doable,” Klauser said. “I’m currently splitting rent with someone, so my living expenses are a lot lower.”

Read More: Economic Uncertainty Makes Financial Literacy a Banking Urgency

.

And she’s not alone. A study conducted by Apartment List, an online marketplace for apartment listings, found that one in five young adults believe they will most likely always be renters unable to buy a home.

Between the Lines:

Younger and low-income families are the most burdened by student loan payments and that low-income families are less likely to make consistent loan payments (44%) compared to high-income families (63%), according to previous studies by the JPMorgan Chase Institute.

TD Bank also discovered more than half of those with student loans had completely maxed out their credit card lines. This, in turn, can play a big role in consumers’ credit scores, and can easily prevent a student from taking out loans in the future. Even a smaller loan for a used vehicle might be out of the question.

Here is where the debt-to-income (DTI) ratios come into play. While credit bureaus don’t report people’s income, they closely monitor credit utilization. Lenders want to see a lower DTI, but if borrowers are throwing half their paycheck or more at towards their student loans, how can a bank or credit union rationalize more debt?

If the tension between student debt and retail lending continues to worsen at this rate, the financial industry may find itself in an untenable position.

The student loan crisis was already bad for Millennials. It will only get worse for Gen Z. And while student debt may not be a problem directly affecting banks and credit unions today, one day (soon) it might be.