Consumer credit is in a Twilight Zone right now. While there are indications that payment performance is improving, there are several flashing yellow lights. In addition, the impact of the coronavirus recession on small business is looking more serious.

A Two-Tier Consumer Borrowing Picture Emerges

TransUnion captures the overall picture in two studies.

In the first, its monthly industry snapshot report, the credit bureau indicates that the most serious delinquency rates improved for auto loans, credit cards, mortgages and personal loans. This covers results seen by all reporting lenders, including fintechs.

“A significant percentage of consumers utilized financial accommodations to defer or freeze payments during the early stages of the pandemic. As the first wave of consumers exit accommodation and a period of excess liquidity, they are returning to their debt obligations and continuing to perform,” said Matt Komos, Vice President Of Research And Consulting at TransUnion.

August Industry Snapshot of Consumer-Level Delinquency Performance by Credit Product

| Timeframe | Auto | Credit Card | Mortgage | Personal Loans |

|---|---|---|---|---|

| August 2020 | 1.39% | 1.23%* | 1.03% | 2.53% |

| July 2020 | 1.43% | 1.37%* | 1.08% | 2.79% |

| June 2020 | 1.50% | 1.48%* | 1.07% | 3.11% |

| May 2020 | 1.55% | 1.76%* | 1.14% | 3.14% |

| April 2020 | 1.33% | 1.87%* | 1.27% | 3.27% |

| March 2020 | 1.37% | 1.96%* | 1.40% | 3.40% |

| August 2019 | 1.32% | 1.72%* | 1.45% | 3.08% |

*Credit card delinquency rate reported as 90+ DPD per industry-standard; all other products reported as 60+ DPD. SOURCE: TransUnion

However, Komos continued, TransUnion thinks that borrowers still in hardship status may be facing continuing income losses and thus have more difficulty on exiting the various accommodation programs offered by lenders. Their status differs from those who entered those programs as a precautionary step.

Quantifying the difference between the two groups is difficult, Komos tells The Financial Brand.

“We don’t have any way to truly split these consumers,” says Komos. “One indication we’ve observed is many of the early exiting consumers from hardship have continued to perform well as they exit.” He says that over 70% of accounts that have entered into accommodation at some point during the pandemic have exited with little to no impact on delinquency rates thus far.

“The theory is a shorter stay could have been an indication that an educated consumer placed debt obligations in forbearance at the peak of uncertainty to build up liquidity,” says Komos. He explains that the buildup of deposits during the pandemic supports this.

Supporting this, JPMorgan Chase, in announcing third-quarter 2020 earnings, reported that deposits were up 28% over 2019.

Another factor in the market is consumers’ decision to spend less. This has already been seen in credit card balances, according to Federal Reserve figures. A survey by S&P Global Market Intelligence indicates that a growing portion of Americans plan to spend less going into the holiday season. 47% of consumers polled said they plan to spend less over the rest of 2020, and 33.2% said they plan to hold spending to 2019 levels.

TransUnion found a telltale sign in the delinquency numbers at the low end, the 30-day delinquency rate. This measurement, considered an early warning, increased slightly in the auto and mortgage categories. These represent the largest debt categories for most consumers.

“This uptick for both products could signify that consumers are starting to roll forward on deferred payments as they come off of hardship programs,” Komos says. “However, it’s still much too early to tell. It could simply be a missed or delayed payment that is late by a few days or weeks, though the consumer’s intention is still to make the payment.”

Here’s a flashing yellow light: TransUnion’s report states that as consumers exit relief programs and the likelihood of further government aid remains questionable, “many consumers may find themselves at an inflection point.” Komos indicates that the next industry snapshot survey may clarify how worried lenders should be.

Lenders Flying with Weaker Radar

One touchstone for consumer lenders is a bit less clear these days. That is the credit score.

“The CARES Act, along with lender-sponsored hardship programs, have paused much of the negative reporting during this period for those consumers using the programs,” Komos explains. “As a result, we are seeing the distribution of scores continue the pre-pandemic trend of shifting up — to lower risk tiers.” Thus, while consumers have that benefit, lenders are dealing with hampered radar.

During the Chase earnings call, Jennifer Piepszak, CFO, said that most card and auto customers were out of the relief programs at Chase — mortgage programs were slated to run longer — and that 90% of consumers who have exited programs are current. The bank also told analysts that while it expects a rise in chargeoffs, notably in credit card accounts, the effect of stimulus and relief efforts has forestalled that and that the chargeoffs that come will likely be seen in latter 2021.

Piepszak noted that the intent of the stimulus and forbearance programs was to improve the end result, not merely delay the impact on lenders. However, she acknowledged that it’s difficult to know whether what she described as a bridge “will be long enough and strong enough” to get consumers and small businesses back to normal.

Overall, says TransUnion’s Komos, “it seems everyone is in the same boat trying to figure out the true impact to their portfolios. Lenders certainly understand they are operating in a riskier environment than what their delinquency and roll rates tell them. Some lenders have expressed concerns that delinquency will increase when the stimulus funds dry up.”

Yellow Lights Seen in Consumer Hardship Study

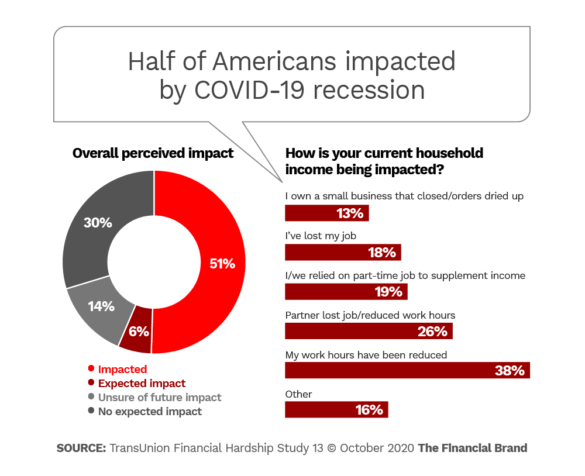

In separate research — TransUnion’s ongoing consumer pulse study measuring COVID-19 impact on consumers — just over half of the sample currently says they have been hit by the recession. Notably, 13% of the consumers are small business owners who have had to close their firms or that have seen orders dry up.

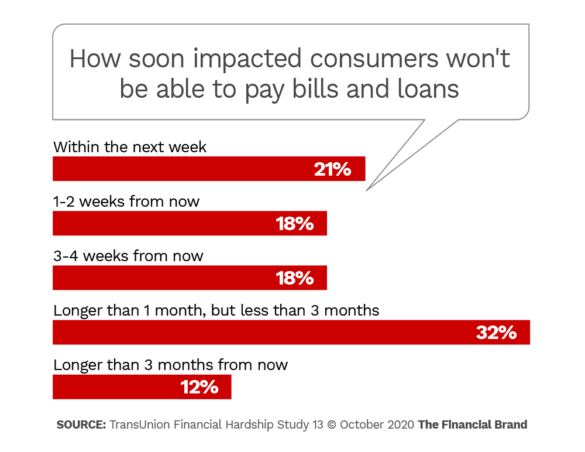

The survey found that of those consumers who say they have already been impacted, they estimated in late September 2020 that they were just over a month — 5.4 weeks — away from not being able to pay their bills and loan payments. (All of the hardship study numbers are snapshots, and have been fluctuating during the term of the pulse study.)

Nearly a quarter of all consumers surveyed have had some financial accommodation from lenders. Among those who are concerned about their being able to repay debt, 63% have approached lenders to discuss repayment plans — the highest rate seen in this survey thus far.

The report notes that the portion of consumers planning to use savings to repay debt has steadily fallen since April 2020, with 26% now saying they will use savings to pay at least a portion of what they owe. 23% plan to borrow from family or friends, 19% plan to use credit cards or balance transfers and 16% plan to take out a personal loan.

But 17% say they don’t know how they will pay.

Impact on Small Business Continues to Erode Owners’ Status

Meanwhile, a fall 2020 survey by LendingTree found that only 13% of small businesses surveyed have been able to return to full operation since the shutdowns of earlier 2020.

Also worrisome is how owners are staying afloat: 74% have taken on debt, even among those who received Paycheck Protection Program funds. This is up from 47% in an earlier round of the survey, taken in March 2020 when COVID first became a factor in the U.S. The types of debt — including multiple sources — that they took on include:

- Credit card debt 37%

- Borrowed from friends and family 28%

- Business loan 18%

- Personal loan 16%

- Home equity credit 2%

- Other 14%

26% of the sample have not borrowed yet.

29% of the owners are worried about being able to provide for their own families, and 22% are worried about paying off debt.

59% of the sample have not had a layoff, but LendingTree pointed out this was skewed, because most firms that had no layoffs were small businesses of ten people or less. 26% of the overall sample have had layoffs and not been able to bring anyone back. 10% had layoffs but brought some people back, and 5% have brought everyone back.