Mainstream consumer lenders face a confusing set of economic conditions as they wade into 2021.

Low rates and the desire in some areas to move out of cities have helped to increase mortgage demand, but the “two-tier recovery” continues to blur the lending industry’s radar. Some consumers are doing quite well, with fewer expenses during working from home, but many people are working below their ability or not at all. Banks and credit unions are bursting at the seams with cheap deposits, but past a certain point a traditional lender can’t make loans to people who lack cashflow to pay.

In many ways the COVID era is scrambling the usual signals that lenders rely on, and institutions will have to pick and choose what types of credit to promote with one eye on the latest conditions and the other on Washington as new regulators and political leaders step into a credit situation already in progress.

Unemployment At Multiple Levels Will Hold Back Credit Growth

In February Federal Reserve Board Chairman Jerome Powell gave a speech that underscored how much unemployment continues to plague the economy. He delved beneath surface numbers and found trends that could only discourage financial institution credit marketers.

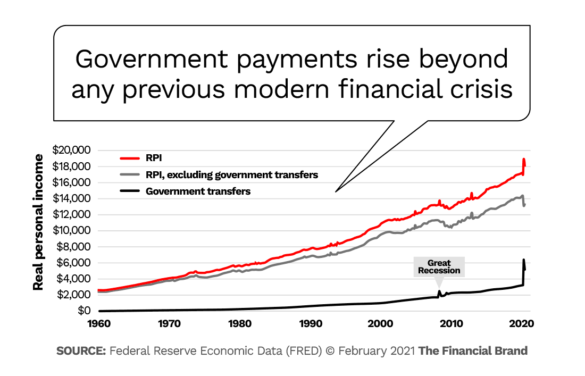

The published unemployment rate hit 14.8% in April 2020 and fell to 6.3% in January 2021, Powell said. However, that’s not the whole picture. “The pandemic has led to the largest 12-month decline in labor force participation since at least 1948,” Powell said. Elaborating, he said that the major impact on industries such as restaurants, hotels and entertainment, and the need for parents to stay at home with children being remotely schooled pulled millions out the workforce, so that they aren’t counted. That factor, and an error at the Bureau of Labor Statistics indicate that in reality 10% of Americans were unemployed in January 2021.

Further, along the lines of the “two-tier recovery” that’s been discussed, Powell said that while top earners have only seen unemployment of 4%, the lowest-income workers have been seeing an unemployment rate of 17%. He suggested that in the absence of the Paycheck Protection Program, the situation would have been even worse. Some economists think that the Biden Administration’s plans to phase in a $15 minimum wage would increase unemployment further — with businesses laying off some people in order to pay the survivors more money.

A Ray of Sunshine?

Considering all the headlines about job losses and small businesses failing, consumer bankruptcy filings could have skyrocketed. But they haven’t. Actually, federal non-business bankruptcies fell by 30% in 2020 vs. 2019.

Research from Harvard Business School reported by one of the university’s publications suggests reasons for fewer than expected bankruptcies may include the federal stimulus payments, federal and state pauses on evictions and foreclosures and in some cases difficulty accessing courts because of COVID restrictions — that plus the thousands of dollars in legal fees some forms of consumer bankruptcy require.

But another factor may be hardship accommodations, some voluntarily offered by banks and credit unions and some mandated by COVID-era federal law. TransUnion has been following hardship levels since the relief began to be offered in 2020. The table below illustrates the trend in each major credit area. The accommodations will begin to expire in spring 2021.

PERCENTAGE OF ACCOUNTS IN FINANCIAL HARDSHIP

| Date | Auto Loans | Credit Cards | Mortgages | Personal Loans |

|---|---|---|---|---|

| March 2020 | 0.64% | 2.15% | 0.48% | 1.56% |

| October 2020 | 3.64% | 2.14% | 5.44% | 3.87% |

| November 2020 | 3.22% | 2.21% | 5.85% | 3.60% |

| December 2020 | 2.93% | 2.42% | 5.36% | 3.36% |

| Peak Level | 7.21% June 2020 |

3.73% May 2020 |

7.48% May 2020 |

7.03% June 2020 |

SOURCE: TransUnion © 2021 The Financial Brand

The percentage of accounts suffering financial hardship are declining, but are still elevated. While the percentages may seem small, they actually represent hundreds of thousands of consumers who have had credit relief. Jason Laky, EVP and head of TransUnion’s financial services business, notes that one key difference between COVID accommodations and those of the Great Recession was the much stronger push by creditors during the pandemic to inform borrowers of relief options. Laky recommends that consumer lenders stay in touch with consumers who have accepted accommodations to be sure of their financial status as they roll out of deferrals.

What Some Large Lenders Are Seeing

How much relief in the form of additional stimulus payments and continuance of the paycheck program there is in the future remains to be seen. It could be argued that at some point the piper is going to have to be paid. On the other hand, economic fires, unattended, generally don’t burn themselves out.

“The bridge has been strong enough. The question that still remains is if the bridge is long enough.”

— Jennifer Piepszak, JPMorgan Chase

The outlook for consumer credit growth trends can’t be separated from current performance. The subject comes up frequently in large bank earnings conference calls.

During one call, Paul Donofrio, CFO at Bank of America, noted that 90-day delinquencies were rising in the bank’s credit card portfolio, but that that trend reflected deferrals. Historically a given percentage of deferrals turn into bad debt, he explained, and BofA expects that this will raise charge offs in the first quarter.

The future? Donofrio says that ultimately the trend with chargeoffs will hinge on whether the unemployed who have been helped by stimulus will receive enough aid. “Will the new stimulus carry them to the point where they get vaccinated and they get their jobs back? Or will the losses just be pushed out into future periods?” said Donofrio.

There is optimism among the largest bank consumer lenders that consumer loan demand will come back to pre-COVID levels soon, but there is also some caution. In response to an analyst question, Jennifer Piepszak, CFO at JPMorgan Chase, said that the government and lender efforts to keep things going — which she calls “the bridge” — “has been strong enough. The question that still remains is if the bridge is long enough. Consumer confidence is still low relative to pre-COVID levels.”

COVID has also morphed the nature of credit demand, according to Ally‘s Jennifer LaClair, CFO. “We’ve seen a shift from services to durables,” she said, “and the whole environment around COVID impact on appetite for rideshare or mass transit has obviously really spurred demand for personal vehicle ownership. So that is a net plus.”

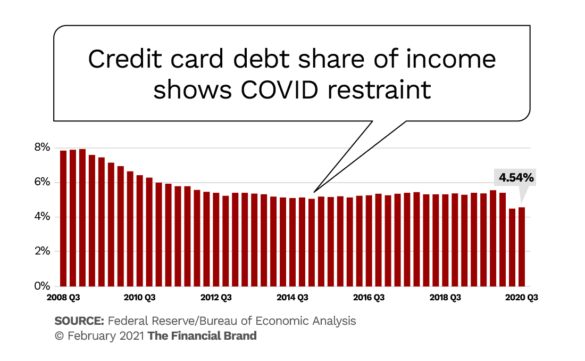

Consumers aren’t dumb. Even with the two-tier economy, a key indicator, credit card borrowing, has been down in 2020. The American Bankers Association Credit Card Monitor, released in February 2021, reported that card issuers remain cautious because of the COVID recession. As of the third quarter 2020, volume of new accounts opened is down 12.2% below pre-pandemic levels. The population of subprime card accounts is shrinking and the portion that is super-prime has hit record levels.

As the chart above shows, while monthly purchase volumes bounced back in the third quarter, the ratio of credit card borrowing outstanding as a share of the nation’s disposable income continues to be at the lowest point on record.

Key Insight:

Consumers are playing it cautious with credit cards. According to the ABA, the portion of cardholders who pay monthly balances in full has hit an all-time high of 33.7%. Those who carry balances has fallen to a record low of 40.7%.

“The record-high share of Transactors [those who pay off monthly] illustrates the resilience of U.S. consumers,” stated ABA Senior Economist Rob Strand. “Though many people are still unemployed, a combination of restrained spending and continued government support has left many consumers well-positioned to manage credit card payments.”

Hence the issuer caution outlined earlier. “Credit card issuers continue to take a cautious but balanced approach,” said Strand.

TransUnion has been predicting that rebounds will be seen in consumer credit types in 2021 as consumer confidence creeps back. But Matt Komos, Vice President of Research and Consulting, warns that lenders shouldn’t mislead themselves by putting too much faith in overall numbers, where strong performers pull up the average.

“We know for sure that there are consumers who are still struggling,” Komos says.

Something that marks this recession, Komos adds, is that many consumers are keeping an almost religious track on their credit ratings. Apps and online sources made available by credit bureaus and some fintechs and neobanks make this much easier to access than was once the case.

A question mark is the “buy now pay later” movement, according to Komos. This has acted as a substitute for credit card charges, to a degree that’s still unclear. Komos says more data from lenders offering these programs is being pulled into credit bureau systems, but not enough has been absorbed yet to get a firm handle on the trend’s impact on credit performance.