A $2 trillion surge in cash hit the deposit accounts of U.S. financial institutions since the coronavirus first struck the U.S. in January 2020, according to FDIC. With interest rates near zero, net interest margins have narrowed, making it difficult for banks and credit unions to turn cash around for a healthy profit. Financial institutions would love to make loans, but there seem to be few opportunities for growth.

Auto lending presents an opportunity for financial institutions to take advantage of consumer trends in financing. We’ll start by identifying those trends, then discuss how banks and credit unions can capitalize on them.

Vehicle Sales And Financing Facts And Statistics

Though the pandemic introduced some changes in the auto lending industry, there is still a strong demand for financial institutions that know the market well, can identify current trends, and develop a plan to seize opportunities to drive lending.

Incentives: Though new car sales are down and are expected to be flat compared with 2019, automakers are offering extremely generous financing incentives to move inventory.

New passenger vehicles: 85% of all new passenger vehicles are financed, compared with 55% used vehicles.

Auto loan debt: Americans owe more than $1.2 trillion in auto loan debt, making up 9.5% of all U.S. consumer debt.

New auto originations: On average, Americans take out $51 billion in 2.3 million new auto loans each month, borrowing an average of $32,000 for new cars and $20,000 for used cars.

Average loan term: The average loan term for new cars is between 35 months and 69 months for used cars.

New auto originations for passenger vehicles: For new passenger vehicles, the number of new loans between 85 and 96 months increased 38% compared with Q1 2018, while loans between 49 and 60 months jumped 18%.

New auto originations: For used vehicles, loans between 73 and 84 months led the market with 42% of loans.

Delinquencies: Nearly 4.5% of outstanding auto debt is 90 days late, while 7% is 30 days late.

Average loan APR: The average auto loan APR in 2019 was 8.06%, but ranged from an average of 5.66% for borrowers with the strongest credit to 21.54% for borrowers with poor credit.

The average new vehicle transaction price: $37,851, with an average loan amount new vehicle of $31,187.12. For used cars, the average loan amount is $20,137.13.

(Stats in the section above come from auto and credit industry sources including Experian, LendingTree, Kelly Blue Book and Cox Auto.)

Opportunities For Financial Institutions in Automotive Credit

Armed with an understanding of the auto loan environment, the question is how can financial institutions take advantage of current auto trends while also preparing for future trends? Here are nine ways financial institution lenders can reach today’s consumers and deliver what they need.

1. Offer pre-approvals early (and often).

By the time an auto shopper visits a dealership, they are likely to have researched their vehicle of choice for an average of 13 to 14 hours, spending fewer days in the market for a vehicle.

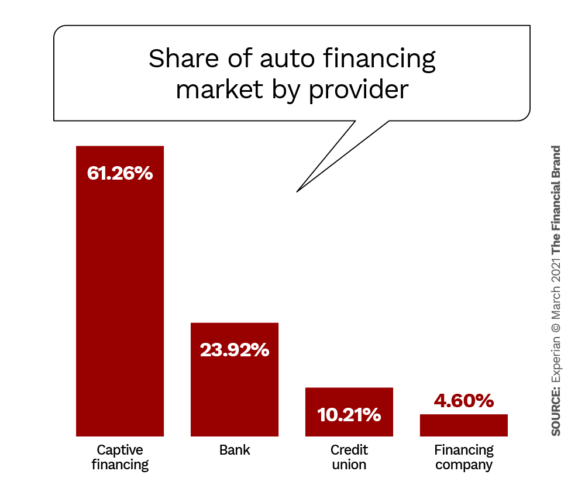

Consider this: More than 61% of new-car financing is done through vehicle manufacturer or dealership “captive” financing deals, while used-car financing is dominated by banks and credit unions with just less than one out of every 10 used car loans financed through a captive.

If financial institutions are going to capture those prospects, they must reach shoppers early in their research phase before they visit a dealer and become susceptible to manufacturer or dealer financing options.

Providing a proactive, pre-approved auto loan to consumers — delivered in a multichannel campaign — not only helps to ensure your offer is top of mind the moment they need an auto loan, it also creates a positive customer experience.

2. Maximize digital branding and promote awareness campaigns.

Marketers can now identify likely auto buyers early in their research phase by their internet browsing behavior and physical location alone. People typically use third-party sites (which allow many ads!) the most for car shopping, with four out of five car buyers visiting the websites during the shopping process.

Of course, car buyers don’t enjoy the finance part of buying a car at a dealership. Brand yourself as a trusted provider of an easy auto loan process, promote the benefits taking care of finances in advance, and consumers will be more likely to originate a loan at your financial institution.

3. Engage trigger-based pre-approvals.

There’s no better indication of intent than someone requesting to have their credit run for a new auto loan. Auto shoppers at this stage may also be seeking pre-approval to find out how much they can afford to spend, giving you an opportunity to win their business.

But it’s essential to catch them quickly, before the loan is originated elsewhere. A proactive contact center phone call can help ensure you reach a loan applicant with your offer in time to be considered.

4. Offer education.

Gen Y and Millennials value companies that offer educational resources that help them make smart financial decisions. Helping them understand the ins and outs of vehicle financing will help position your institution as a favorite when it comes time to signing on the dotted line.

5. Ensure a positive digital experience.

Just like specialized educational resources, Millennials and Gen Z also highly value customer experience. Online and mobile auto loan applications that are entirely digital and optimized for customer experience are essential to capture more loans from this consumer segment.

What should this experience look like? For starters, think “intuitive.” The helpful use of autofill, conditional fields based on previously entered information, data validation that ensures correct and accurate application information, as well as an option for a digital capture of driver’s licenses and other documentation, can help consumers quickly fill out applications.

.6. Use quick decisionmaking for auto loans.

Quick decisioning automatically qualifies applications with exceptional credit scores and offers the best terms to those consumers. It also automatically declines applicants whose attributes indicate they are a high risk or do not meet your credit guidelines. You can even automatically structure loan offers by modifying the loan terms to present other acceptable deals if an applicant initially falls short of your credit criteria.You can offer lower loan amounts, shorter loan terms, etc.

7. Use alternative credit data.

Verify financial strength for those who are too young to have established stellar credit scores, but are still considered low credit risks by examining their record of rental, utility and other payments, employment history and stable address history, for example.

8. Use auto refinance as a tool to build goodwill and deepen consumer relationships.

Car buyers who got their initial loan from a dealer are often paying higher rates than banks and credit unions. Even indirect loans through traditional lenders charge slightly higher rates to compensate the dealer. Let people know that they have options even after their initial finance deal. When rates have decreased, they can save money with a lower payment.

When a consumer’s credit score has improved, they may qualify for more favorable terms. Consumers with long loan terms can restructure to a shorter term and avoid owing more than their car is worth. Banking providers could also integrate loyalty programs that offer benefits for more product ownership.

9. Continue marketing after the deal is closed.

While the average new car buyer expects to be in a car for six to eight years and the average age of cars on the road is 11 years, 17 financial institutions should market to the auto loan holder even after the deal is done. Remember, auto loan holders likely to need other loan products and credit cards.

Continuously and proactively market other pre-approved offers to them. They will consider their experience with your institution on the auto loan an indicator of the experience they’ll have with you on other loans.

Credit unions should take advantage of the opportunity to convert indirect members who come in through partnerships with dealers. In fact, by using Harland Clarke’s Multi-Loan Pre-Approval product, one credit union saw that 20% of their total respondents were indirect members.

Financial institutions should continue to provide loan education, especially to Millennials and Generation Y. Start early mortgage loan education — optimizing their credit score for a mortgage, financially planning to buy a home, saving for a down payment, etc. Many potential consumers will be in the market for mortgage loans in the future, looking at your bank or credit union as a trusted provider to help them achieve their goals responsibly.

Auto lending remains a powerful opportunity for financial institutions. By combining a digital-first process and a strong orientation toward customer experience, financial institutions can position themselves to become the go-to resource for consumers in the market for an auto loan.