For years, bank and credit union leaders in the U.S. have looked at the Canadian banking model — five huge banks and a few small and midsize institutions — and said, “That will never happen here.” Maybe not completely, but more and more the situation is moving in that direction as four megabanks dominate U.S. retail banking.

And their influence keeps on growing…

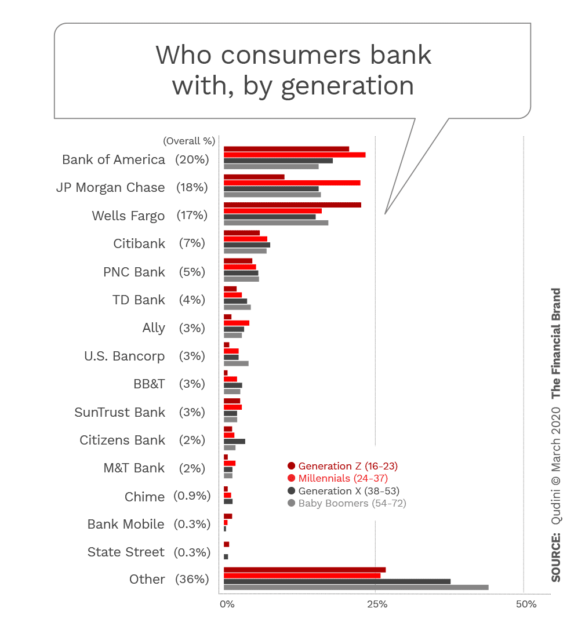

A survey of U.S. consumers found that close to two thirds (62%) of the more than 2,000 respondents say they bank with one of the top four U.S. banks: Bank of America, Chase, Wells Fargo or Citibank.

As the chart below shows, a little over a third (36%) of consumers bank with “other” financial institutions. That’s still a sizeable number in total, but those people are spread over approximately 9,800 banks and credit unions.

The survey, conducted for software provider Qudini, included people ranging in age from 16 to 72.

The number of consumers using the digital-only banks Chime and BankMobile was under 1% for both. Ally Bank fared better at 3%, putting it on par with U.S. Bank. In total only 4% of Gen Z respondents have bank accounts with digital banks such as these — far below the numbers for the top four banks in the chart.

Bank of America and Chase had the most Millennial customers at 24% and 23% respectively, while Wells Fargo had a particularly large Gen Z customer base at 23%. Citibank and PNC have fairly even distribution among generations (as does BofA), while TD Bank and U.S. Bancorp skew somewhat older.

What’s Holding Back the Digital Banks?

Traditional bankers may be surprised (and pleased) at how few consumers actually have bank accounts with digital-only banks, also referred to as challenger banks or neobanks, especially considering how much attention these upstarts have received. Across all generations, only 5% of consumers bank with Ally, Chime or Bank Mobile. The figure increases to 7% for Millennials.

Brand recognition among some neobanks was much higher than actual usage. Slightly more than half (51%) of all respondents had heard of Ally, putting it about even with Citizens Bank’s 52% level of recognition and above TD Bank’s 48% and U.S. Bancorp’s 32%.

As the Qudini report states, “The main obstacle holding [consumers] back from opening an account with challenger banks … was the lack of physical branches, with 37% agreeing that banks without any branches was off-putting.” Not surprisingly, this was most true among Baby Boomers, at 45%.

The research found that Gen Zers want face-to-face service alongside tech-led channels from their banking providers. More than four out of five (81%) of these young adults say face-to-face support is important, compared to 78% across all generations.

Read More: How Banks Can Beat Fintechs in the War for Millennials and Gen Z

Two-Pronged Threat to Mid-Tier Institutions

While the percentage of consumer account penetration by digital banks may appear very low, the math suggests that five out of every 1,000 U.S. adults on average has an account with one of these digital banks if the survey sample is representative. How many traditional institutions can say that?

Two further points from the Qudini research add further insight into the position of some of these non-traditional financial institutions:

1. Of the consumers who use a challenger bank, nearly two in five (39%) say they use the bank as their sole provider. This was true for 100% of Gen Z respondents who use a challenger bank, 41% of Millennials and 47% of Gen Xers.

2. Just over one quarter (26%) of challenger bank customers say they are strongly considering using the bank as their sole provider. This was especially true among Millennials at 32%.

Those figures suggest that American consumers, having tested the nontraditional banking waters with a secondary account or product, are becoming more comfortable in using neobanks for their primary account.

Balancing that is the finding from Qudini that nearly nine in ten consumers (87%) rate their current primary banking provider as good or very good. Further, a little more than a quarter say they’ve never switched primary providers. However, another quarter have switched primary providers three times or more.

Not known from the data is which institutions the “stickers” are sticking with, or who the “switchers” are switching to. Based on the figures cited earlier, it may well be one of the four megabanks in both cases.

Ranking the Top Four on Key Factors

Given the fact that such larger percentages of respondents have bank accounts with Chase, BofA, Wells Fargo and Citibank it is not surprising that these four score the highest overall in brand awareness and in-branch experience. That is part of the challenge for the rest of the industry: the largest banks do it all and they do a lot of things very well.

Not everything, however. Wells Fargo, though popular with Gen Z consumers, was among the weakest in terms of brand strength and general customer service, the study found.

JPMorgan Chase just edged out Bank of America as best at providing good customer service — 69% for Chase versus 68% for BofA. The tables were turned, however, with the opinions for which institution provides the strongest in-branch experience:

- Bank of America 20%

- JPMorgan Chase 17%

- Wells Fargo 17%

- Citibank 8%

Regarding online banking, BofA took top honors overall, but among the younger respondents — Millennials and Gen Z — Wells Fargo and Chase were seen as having stronger online offerings.

Read More: The Challenger Banks That Threaten to Disrupt Financial Institutions

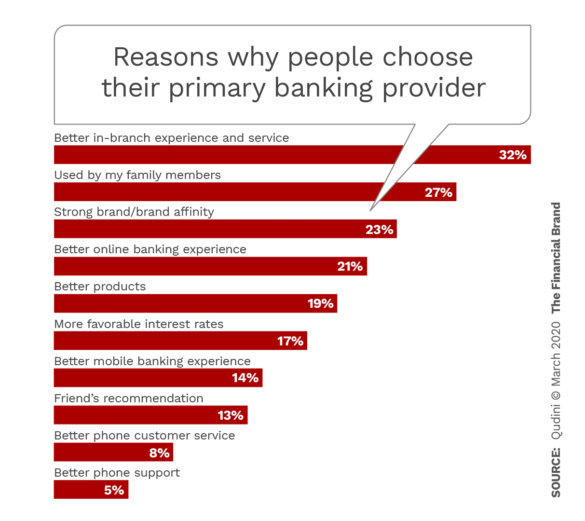

What Consumers Look for When Selecting a Bank

Almost a third of all age segments say they were strongly influenced by family when selecting a banking provider. It was the number-two reason behind “in-branch experience and service.” Actually family might be even more significant if one infers that the respondents probably learned about a prospective bank or credit union’s branch qualities from friends or family who had already experienced them.

The low ranking of phone support as a determining factor in selecting a bank or credit union may be somewhat misleading. The survey probed this area and found that while only 16% of all consumers say good phone service was important to them, nearly three out of ten Gen Zers (29%) felt it was important.

Further, 56% of Gen Zers say they rely on telephone support to interact with their financial institution, according to the study. That gives traditional institutions an edge over many challenger banks that have no, or very limited, phone support.

Other Banking Preferences of Younger Consumers

Lest retail bankers conclude from the above that young adults have abandoned the ideological principles that so many researchers have attributed to them, that’s not the case. Qudini’s study found that 78% of Gen Z adults and just slightly fewer Millennials (68%) say it’s “important or very important for banks to reduce their environmental impact with more sustainable processes and materials.” Further, nearly seven in ten (67%) believe giving back a percentage of profits to help people in need is important.

Beyond that, the study identified these notable facts:

- 82% of Gen Zers and 79% of Millennials want self-service kiosks for tasks like cashing checks quickly.

- Three quarters of Gen Z consumers say the option to pre-book an appointment time to discuss financial issues is important. This doesn’t necessarily mean an in-person conference, however. A video or phone conference appointment works as well for young adults.

- An easy-to-use online banking platform was highly important to 32% of all respondents and 43% of Millennials.

- An easy-to-use mobile banking app was highly valued by the same percentage of Millennials (43%) and by 39% of Gen Zers. But only 18% of Baby Boomers agreed.

- Among the entire sample, just over a third (34%) visit a branch less than once a month. However, among the Gen Z respondents, 22% visit a branch once a week, and 25% go once every two to three weeks.