Many neobanks and fintechs offering consumer accounts start off narrowly, sometimes offering just a single account, and they frequently depend on the underlying structure of their banking-as-a-service partner for the real functionality behind their easy-to-use customer experience layer.

Brian Hamilton, Co-Founder and CEO at One Finance, had something different in mind when he founded One, a neobank whose consumer accounts hit the street in September 2020. He wanted to create something that would bring middle-class consumers a convenient new form of banking account, credit card service at lower rates than traditional card issuers offer, and new ways for people to cooperate financially.

But beyond that, Hamilton wanted an unprecedented degree of control over not only the way the guts of One would work, but also over its future as a financial organization.

After having developed multiple fintechs on the business side of banking, including Azlo, he wanted that control for the sake of continuing independence and to be able to slash typical costs of providing consumer banking services.

Read More: The World’s Biggest List of Digital Banks

How a Serial Neobanker Tackles Consumer Finance

Hamilton fell into banking as a commercial lender at Wells Fargo out of college. But he wound up writing application programming interfaces, mostly dealing with foreign exchange and business, for Wells.

At heart, Hamilton found that he was a tech entrepreneur and over the years he founded several tech firms, among them PushPoint, a mobile tech startup he sold to Capital One. He says staying on at the acquiring bank for a time taught him that innovation could be scaled. Later came Azlo, a business neobank, which taught him a lesson about independence.

Founded in 2017, Azlo was started with a majority investment by a fintech business incubator operated by BBVA.

“I grew Azlo using BBVA for seed money, as a primary investor,” says Hamilton. “But because of their stake, it was basically treated as part of the control group of the bank. This is different from taking money from a traditional venture capital investor. When you take money from a bank you’re at the risk of being treated as part of the bank by regulators, which Azlo was.”

In time, Hamilton began to realize Azlo wouldn’t grow into what he’d had in mind under a banking umbrella. Indeed, later on, as part of the runup to the acquisition of BBVA USA by PNC, completed June 1, 2021, both Azlo and Simple, a consumer service, were shuttered.

“Once we had gotten Azlo up and running, it turned out that you couldn’t leverage a bank for the advantages you wanted to,” Hamilton explains. Being essentially inside the bank imposed layers of risk governance that added costs and complexities and that Hamilton says stifled potential innovations.

Who’s Encroaching on Whom?

Hamilton believes that long term more fintechs and neobanks will acquire banks or obtain bank charters than banks will buy fintechs.

Long before the shutdown, Hamilton took a big chunk of his team — software engineers and legal and compliance experts — away with him to found One. He intends that One will remain independent so those innovations can be brought to full fruition.

Read More:

- How This Ex-Apple Card Strategist Is Taking ‘Dave’ to Next Level

- Is Challenger Bank Chime the Future of Retail Banking?

- An OCC Insider’s Perspective on Fintechs and Bank Charters

Designing a Fresh Take on Banking-as-a-Service

The package of offerings One makes to consumers is interesting, but the mechanism used to accomplish that is at least as interesting because it follows an atypical approach among fintech players.

“If you build a bank in a box, you can’t do anything outside of the box,” says Hamilton. “And bank in a box is how I describe what neobanks become when they build on top of sponsored bank architectures.”

Hamilton says there are dozens of players in the challenger bank field and dozens more coming. Some are standouts, he continues, like Chime. But many float in a “sea of sameness,” Hamilton says, and may be stuck there.

“If you look at most of the neobank offerings, they are basically a better user experience on top of a debit card. The checking account behind the scenes is the same thing it always was. They just improved the UI and the UX. And, to be fair, there was a lot of low-hanging fruit, because banks’ UI sucks.”

— Brian Hamilton, One Finance

Hamilton says the key to ultimate flexibility was to develop and own the technology stack that would make One what he wanted it to be.

“We built our own architecture down to the rails,” says Hamilton. “It’s the difference between ‘rent an architecture’ versus ‘own your architecture’. When you own it all yourself, you have a lot more autonomy to do meaningful things.”

To accomplish this, rather than relying on the core system of One’s banking-as-a-service vendor, the neobank bought its own virtual core from Finxact, which promotes its technology as “core as a service.”

“This is a heavier lift, and takes longer and more money, to accomplish,” says Hamilton. “Time to market is longer and upfront investment is higher. But at the end of the day, you own more of the economics for yourself instead of spending it on having five other vendors in the mix.”

It’s All About the Money:

A good deal of what makes One Finance possible is patient capital. The time One’s team took to build its core is time most venture capitalists would rather see a neobank acquiring additional customers.

With the breakneck pace of fintech evolution, how did Hamilton find patient capital? First, his co-founder, Bill Harris, is a seasoned fintech executive and investor, including having co-founded Personal Capital and been CEO at pivotal stages of both PayPal and Intuit. Harris provided some of the startup funding.

Additional investors bought into Hamilton’s pitch that a neobank could either rent a car or it could build and learn to fly a space shuttle. The former is quick but limited, the latter takes training, “but at the end you get to fly into space.”

“Even patient capital isn’t infinitely patient,” Hamilton explains, but One’s investors gave him enough breathing room to go for the heavier lift.

One’s banking partner is Coastal Community Bank, through its CCBX division. (Coastal is one of the banks working with Google on the Google Plex project.)

While the deposits and loans that One generates reside on Coastal’s balance sheet, One’s core system tracks everything as if it were a freestanding bank. One’s records flow into the bank, getting recollated for Coastal’s regulatory reporting purposes. In essence, One is already organized as a standalone bank, according to Hamilton, although it doesn’t have a charter and relies on Coastal for deposit insurance and the ability to offer a credit card nationally.

What One Accounts Bring to Middle-Class Consumers

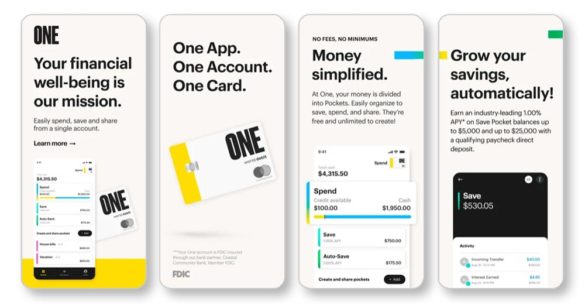

This focus on structure and technology helps One offer multiple consumer financial services in one account.

Each account consists of spending functions and savings functions, including an auto-save feature that works by rounding up purchases. Basic savings get 1% APY presently and auto-saved amounts earn 3% APY. Auto savings of up to 10% of the consumer’s paycheck also receive 3%.

Overdraft protection is built in with a credit line, which is also used to give the consumer a credit line that is based on their cash flow. The line grows as positive experience with the consumer occurs. Customers who put their paychecks in the account receive higher credit limits, but all deposits are taken into account for computing credit limits on a rolling basis. The main offering is unsecured, but for credit newcomers One offers a secured variation to help them build credit.

Part of what sets the offering apart is that borrowing rates are much lower than other credit card options — 12% APR. Hamilton, who comes from middle-class roots, feels typical rates are too high.

“We’re clearly paying for way too much legacy infrastructure and paying rent on a protected system that’s not returning value to the customer,” he says. One’s technological approach enables costs to be cut which allow for lower rates based on consumer cash flow, he explains.

An interesting feature is One’s Pockets. This is a way for customers to create the equivalent of a joint account with friends and family for the sharing of shared expenses or shared savings goals. It’s sort of a P2P financial tool for people banking under One’s roof. (It also functions as a tool for building One’s membership.)

One has an average rating of 4.8 on the App Store and 4.6 on Google Play, both out of 5.

Overall, Hamilton describes One as a “rebundling” of what most fintechs and neobanks have been unbundling.

So, how will One make money?

While Hamilton declines to get too far into the weeds on how revenue is shared with the bank partner, he explains the basics. First there is interchange income, a basic of the neobank mix. But second, because One is both taking deposits and lending via its credit card, there is spread income, part of which belongs to One. The latter will pick up, he says, as more consumers begin carrying balances.

Another feature puts One head to head with brands like Aspiration. One pledges that its customer balances will never be used to finance lending for such industries as guns, fossil fuels, palm oil, private prisons and tobacco.

Read More: What SoFi Rise to One-Stop Financial Shop Means to Banking

Is There a Charter in One’s Future?

“Some companies have bought a charter as if that was the end all be all of this business,” says Hamilton. “I don’t think that’s the case.” Fintechs that don’t get into any lending don’t need to think about a charter, he suggests.

One isn’t up to the charter stage yet, but Hamilton can see the fit for his company’s strategy, for the right reasons.

“The advantage to a charter is the cost of funds and leveraging deposits as lending capital. So for businesses that include lending, like ours, you can’t ignore that at some level of scale or some combination of events a charter might make sense,” says Hamilton.

At this stage in its development, not having a charter makes more sense for One. Hamilton also points out an interesting aspect of venture capital investors: they cringe at the idea of parking big chunks of their investment as statutory bank capital kept sterile on the balance sheet as a cushion.

“There’s a lot of cost margin in the banking system that deserves to get back to the middle class, and other fintechs have only scratched the surface,” says Hamilton. “They haven’t broken the dam yet — and that’s what’s coming.”