The level of financial technology (fintech) adoption among digitally active consumers is set to grow significantly in the next year. This will require traditional financial services companies to revisit their product development, distribution, communication and innovation strategies to compete effectively with the new market entrants, according to EY’s first Fintech Adoption Index.

The survey included 10,131 “digitally active” consumers in Australia, Canada, Hong Kong, Singapore, the UK and the US. It was found that 15.5% of those surveyed had used at least two fintech services – financial services products developed by non-bank, non-insurance or online companies — in the past six months. Beyond current use, it was found that adoption rates among digitally active consumers could potentially double within the next 12 months if respondents follow up on their intentions to use fintech products and services.

The index evaluated the use of 10 fintech services in four categories:

- Savings and Investments

- Money Transfer and Payments

- Borrowing

- Insurance

The 10 services included P2P investment services, equity/rewards crowdfunding, online investment advice and investments, online financial planning, online stock brokering or spread betting, online foreign exchange, overseas remittances, non-bank money transfers, P2P borrowing, and health insurance premium aggregators or car insurance using telematics.

Imran Gulamhuseinwala, EY Global Fintech Leader, said, “The adoption of fintech products is relatively high for such a new sector, so the risk of disruption is real. As fintech continues to catch on among consumers, traditional financial services companies will have to reassess their view of which customers are most at risk from the new competition and step up their efforts to serve them effectively.”

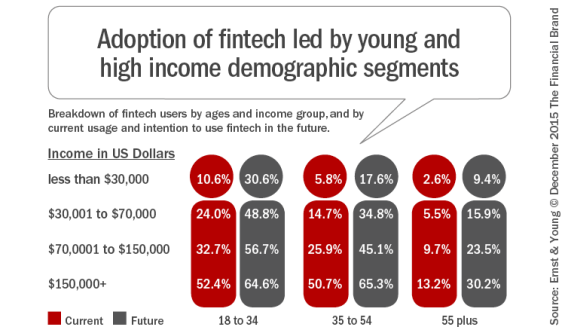

Young, Urban and Wealthier Audiences Lead Fintech Parade

The EY study found that the stereotype of fintech users being young, urban and higher-income would be on target. Both current and future users of fintech services fell into the 18-34 age category and tended to be wealthier and located in urban areas such as New York, Hong Kong and London.

Urban consumers were found to use fintech at rates greater than the 15.5% average for all six regions surveyed. According to the study, online users in New York are more likely than users in the United States as a whole to use at least two fintech services (33.3% in New York City compared to 16.5% for the US as a whole). The same is true of respondents in London who use online services (25.1% in London compared to 14.3% in the UK as a whole).

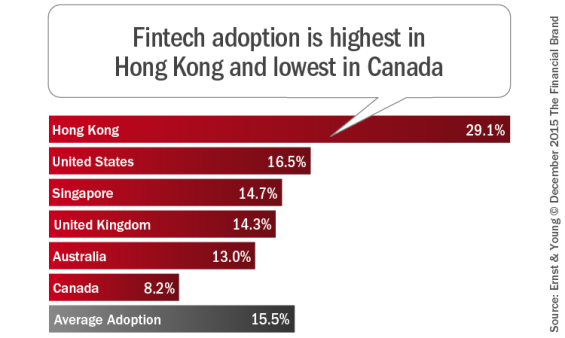

Hong Kong was found to have the highest rate of fintech use of all markets surveyed (29.1%). The US had the second-highest adoption rate (16.5%), followed by Singapore (14.7%), the UK (14.3%), Australia (13%) and Canada (8.2%).

As a result of the demographic variations, traditional banking organizations need to build more digital acquisition strategies to appeal to the younger consumer as well as improve digital engagement strategies to retain existing higher income, high value customers. Otherwise, these consumers will find their digital solutions elsewhere.

“Higher-income individuals are some of the most economically valuable customers for banks and insurers,” observed Steven Lewis, EY Global Lead Banking Analyst. “These organizations will have to review how their offerings, such as their own multi-channel strategies or partnerships with fintech providers, meet their customers’ needs. Otherwise, they may have difficulty stemming the flight to fintech.”

Because of the potential for exodus to fintech firms, traditional providers may want to consider exploring partnerships with fintech providers as opposed to building in-house. This was the most prominent trend identified in the 2016 Retail Banking Trends and Predictions compiled by The Financial Brand.

Fintech Potential Differs by Product Category

The overarching advantage provided by most fintech solutions is the ability to make consumer’s lives easier. By leveraging technology to deliver value and convenience, fintech firms have targeted those services with the most friction in the delivery process as well as those with the greatest financial margins.

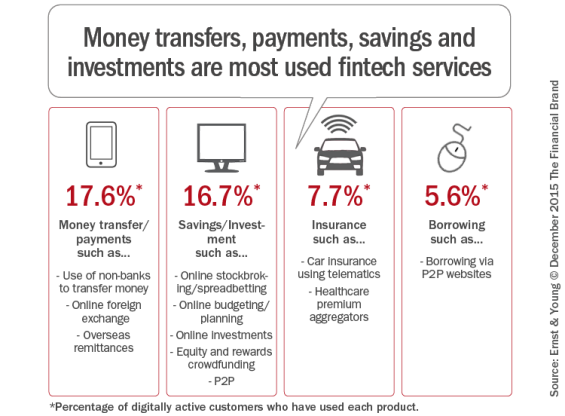

According to the research, payment services had the highest adoption rate (17.6%) of all services reviewed. Services in this category included the use of non-bank providers to pay for goods and services, transfer money between accounts and send

funds overseas.

The savings and investment category was the second most impacted by fintech firms, with usage pegged at 16.7%. Services in this category included online stockbroking and spreadbetting, online budgeting/planning, online investing, equity and rewards crowdfunding and P2P lending.

Finally, insurance services, including health premium aggregators and car insurance using telematics (7.7%), and online borrowing through peer-to-peer websites (5.6%) were the less commonly used services by respondents.

Simplicity is Fintech’s Calling Card

There is nothing simple about opening a checking or current account, adding a savings plan, taking out a loan or establishing an investment or insurance relationship at a traditional bank. At most institutions, the paperwork is intimidating and the consumer is usually are relegated to visiting a branch office.

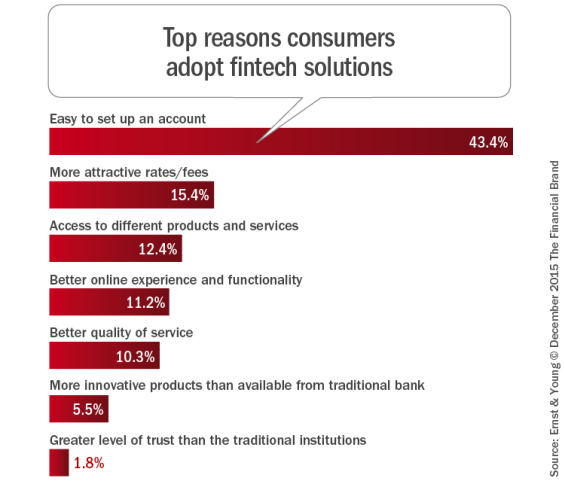

That may be why the simplicity of setting up an account was the overwhelming reason for using a fintech provider according to the EY study. More attractive rates, access to different products and services and a better online experience were also popular responses, but these were dwarfed by the impact of making the process simpler for the consumer to engage.

Unfortunately, while there has been some progress made in digitizing some account opening and transaction processes by traditional banking organizations, the speed of change is not keeping up with the expectations of the digital consumer who are conditioned by the likes of Amazon, Apple, Uber, etc. For instance, less than 30% of the largest banks in the US provide an end-to-end mobile account opening process. Fintech firms also have built platforms where engagement with products is as easy as one click.

Awareness is Fintech’s Biggest Obstacle

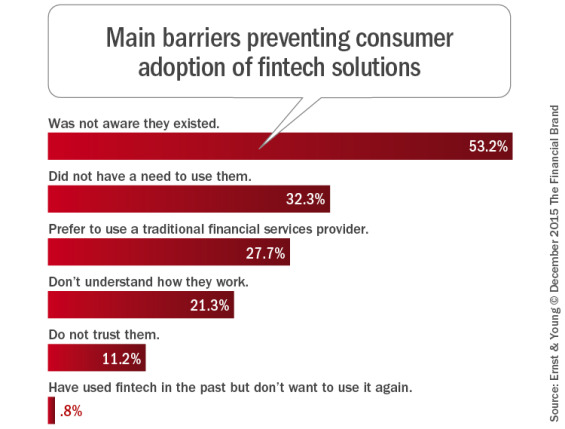

While ease is fintech’s calling card for success, lack of awareness is the primary impediment to a broader adoption in the marketplace. Bottom line, the majority of non-fintech users are unaware that most fintech products exist, which provides a potential springboard for growth.

According to the research, for digitally active respondents who had not used two or more fintech products in the past six months, 53.2% said they were unaware the products existed, followed by 32.3% who say that they did not have a need to use the products. In addition, 27.7% preferred to use their traditional financial services provider, while 21.3% said they do not understand how the products worked.

Interestingly, trust was not a major impediment for fintech use, with only 11.2% of respondents saying they do not trust fintech providers.

“The fintech firms are focused on under-served niches,” wrote Gulamhuseinwala. “The fact that they are skewed toward city-based, young professionals reflects their reliance on variable cost marketing strategies such as digital marketing, word of mouth and referrals. As successful fintechs become better funded and more established, they can afford fixed-cost marketing strategies such as TV advertising and sponsorship, which will put them in more direct competition with the banks.”

The Opportunity for Collaboration Between Fintech and Legacy Banks

Not taking action on the trend toward digitalization is dangerous since the industry’s older customer base is shrinking. According to EY, the “Facebook Generation” will reach peak earning potential within the next ten years. This new breed of customers will demand anytime, anyplace, contextual tailored experiences facilitated by smart devices and ubiquitous internet access. Most banks currently struggle to meet the demands of this digital-first consumer.

Fidor and Atom are both newly licensed digital banks operating in Europe. Simple, Moven, BankMobile are growing in the US, with many other challenger banks close behind ready to introduce new banking services. It is only a matter of time before these mobile-first banks become the new normal.

The response to the fintech movement will differ for each organization, with the options of building internally, buying, partnering or playing “wait and see” all being options. But with the penetration of smartphones and wearables increasing and the expectations being set outside the financial services industry, there is the need for a logical approach for transformation and differentiation.

Matt Hatch, EY Americas Fintech Leader, said, “This index shows that the innovations and changes of fintech are here to stay. A co-existence and collaboration between the new and old market players will be inevitable. There is much that traditional financial services firms can learn from how fintech firms think about the customer proposition and harness technology to deliver a compelling service.”