Most Americans now shop online for new financial accounts, including loans and deposits. They either head straight to their primary financial institution’s website, or they Google around to review offerings from multiple institutions. While everyone in the financial industry seems to intuitively accept this fact, most banks and credit unions are dropping the ball when it comes to helping online shoppers, particularly at that critical final stage when people want to actually open an account or apply for a loan.

According to Mark Riddle, Director/Research and Content Delivery at BAI, consumers spend an hour or more shopping for financial services, but they can’t finalize the process digitally.

Riddle says there are still major shortcomings when it comes to the digital experience most banks and credit unions deliver. Among the many weak spots in banking providers’ digital capabilities, many cannot track how consumers shop for products on their own websites.

Riddle is especially critical of the online account opening process in the retail banking sector. Most institutions cannot accommodate those who want to open an account digitally.

“There’s a lot of work to be done,” observes Riddle.

What’s worse, many consumers see financial institutions stuck in this state of affairs, and don’t expect things to change in the next few years. Riddle noted that only 35% of Millennials surveyed by BAI think their main banking institution will be able to open accounts online within the next few years.

When incumbents in every industry get compared to Amazon and other ecommerce giants, Karl Dahlgren, Managing Director at BAI, says financial institutions are often left in the dust.

Financial marketers recognize that it’s now harder to build and retain relationships with consumers in an increasingly digital era, thanks to Amazon, Netflix, Apple, et al . When BAI polled financial institutions in both 2017 and 2018, they asked if new digital capabilities made it any easier to manage relationships with consumers. Even if you think things aren’t great today, you would probably assume that the banking industry is making progress. Not so. Sentiment actually darkened in the 2018 research, with only 25% of respondents saying things were easier, versus 32% in 2017. 41% of the sample said things were tougher — about the same as in 2017.

If You Build It, They Will Come

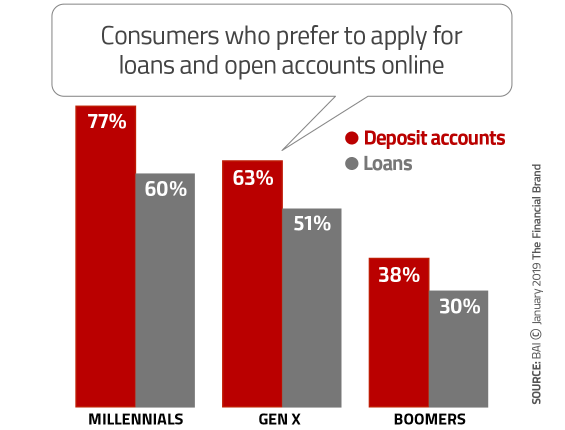

According to BAI research, online account opening has become the method of choice among consumers, with six in ten respondents preferring it for deposit account and nearly half for loans. Among Millennials this preference is even stronger.

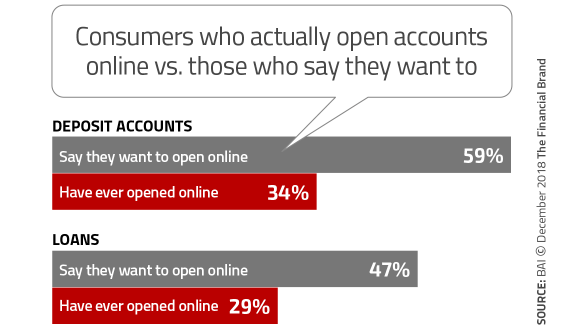

While these preferences are strong, the percentage of the sample that have ever opened a deposit or loan account is much lower. Only three out of every five consumers who want to open accounts online actually do so. Why this huge gap? The reality is that many institutions — even if they offer some form of opening accounts online — don’t allow someone to open their first account digitally due to identity verification concerns and fraud prevention, among other reasons.

“There’s a big gap between supply and demand here,” observes Dahlgren, who says online account opening is no longer a “nice-to-have” but a “must-have.”

“There are people who have figured this out,” says Dahlgren. “And the people who get to this quicker are the people who are going to win.”

Online-Only Banks Shaping Up as Tough Competitors

According to BAI’s research, most consumers who can’t open accounts online wind up going to branches… at least for now. But a factor at play is that consumers are making the connection that online-only direct banks typically pay more on deposits than banks with branches.

While only 20% of consumers prefer the online model versus the traditional experience, but other facts indicate such feelings may be misplaced.

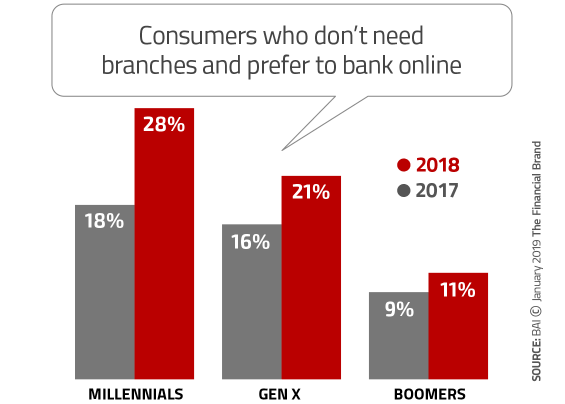

Dahlgren notes that the percentages favoring online jumped massively in just one year, with this preference becoming more and more exaggerated the younger you go. The greatest year-over-year shift was seen among Millennials, skyrocketing a full ten percentage points higher (a 55% increase).

“That’s a huge change,” says Dahlgren.

“Do you want someone else to eat your lunch? Or would you rather be the one to eat your lunch?”

— Karl Dahlgren, BAI

Reality Check: Nearly two-thirds of consumers who opened accounts online opened them with online-only banks.

BAI research has found that Millennials consider large ATM networks more important than convenient branch networks. At first, this may seem like good news for brick-and-mortar legacy banks and credit unions. But online-only bank accounts piggyback on existing networks, so that generally negates any competitive differences.

The bottom line, Riddle cautions, is that digitally-savvy providers will continue to gain an advantage if more traditional institutions don’t improve their online capabilities.

That helps explain why a growing number of mainstream retail banks have started online-only subsidiaries. These include the Millennial-oriented Finn from JPMorgan Chase, and Capital One 360.

“This strikes me as a Netflix-Blockbuster choice,” says Dahlgren. “Do you want someone else to eat your lunch? Or would you rather be the one to eat your lunch?”

Hitting The Millennial Moving Target

“Millennials never met a channel they didn’t like.”

— Mark Riddle, BAI

Millennials have a lower preference for banking providers with branches than other generations in BAI’s research. Roughly half (49%) of Millennials say they want branches, compared with 58% of Gen Xers and 69% of Boomers.

Reality Check: Millennials may say they need branches less than other generations, but they actually use branches more. In any month, Millennials use branches an average of 5.1 times versus 3.3 for Gen Xers and 2.5 for Boomers.

“Millennials never met a channel they didn’t like,” said Riddle.

More than one quarter (28%) of Millennials would prefer to do business with an online-only bank, citing two reasons: because (1) they feel they don’t need branches, and (2) for better rates. However, BAI’s research also found that of all the generations analyzed, Millennials have the most interactions with their primary banks. They interact with their banks 107 times a month on average, versus 68 times for Gen Xers, and 55 times for Boomers.

Pessimism about bank and credit union offerings getting better appears to be growing among Millennials. That could spell trouble, because just over half of Millennials — much more than other generations — would switch to another provider for a better mobile app and other superior digital capabilities, Dahlgren noted.

At the same time, nine out of ten Millennials say they are happy with their current banking app.

“They’re happy,” cautions Riddle, “until they’re not happy.”