The personal finance world has been sharply, and unevenly, impacted by the ongoing pandemic — from employment to money management, and from payments to investing. While many people have actually benefited financially due to lower costs, investment income and other factors, millions have reported tremendous stress in their personal finances. This stress has appeared with the most prevalence among lower income people, women and diverse racial groups. In our company’s latest Future of Money Study, conducted in December, 2020, we found that those identifying as white had significant financial differences from those identifying with diverse racial groups.

Financial institutions, almost all of whom work directly with a wide consumer base, must understand how the fallout from the pandemic has affected their core audiences. Deeply understanding the unique stresses that key constituencies face can guide successful decision making surrounding products, services, marketing and communications.

Ongoing Household Income and Employment Impacts

Job loss walloped many sectors during 2020, and U.S. unemployment rates, though down from their peaks during the early months of the pandemic, continue well above normal. Naturally that trend impacts personal incomes, but, again, unevenly. Our study found that white populations reported higher average household income of $76,000, with racially diverse groups reporting average household income of $59,000. Since the onset of COVID-19, 34% of diverse groups report they were no longer working (or working fewer hours), compared to 23% of whites. Part of this may be due to job type.

Sharp Contrast:

The Economic Policy Institute found nearly 1 in 3 white Americans were able to shift their work to their home during the pandemic, but less than 1 in 5 Black Americans and 1 in 6 Hispanics were able to do so.

In the United States, the pandemic has overwhelmingly affected low-wage, minority workers. As the Washington Post states, “No other recession in modern history has so pummeled society’s most vulnerable.”

Everyone must work together in order to combat this new, unwelcome reality.

Banks and credit unions have a clear role to play. Job loss directly affects the way consumers manage their money and the type of financial needs they will look to their financial institution to provide. Financial marketers must be both empathetic and sensitive in messaging and communications, reflecting an understanding of the vulnerability that many consumers are feeling due to income and job loss.

Banks and credit unions should develop programs that directly address the strains diverse groups are experiencing, including services and options that will meet immediate financial needs. Also, take another look at fees and penalties to avoid taxing an already overtaxed population. Many institutions did this in the initial stages of the pandemic, waiving late charges and overdraft fees, for example, but many of these measures have since ended. Finally, create a customer service model that gives employees the time, data and other resources to really understand each individual’s unique needs.

Make sure that you aren’t employing a one-size-fits-all strategy for your products and services right now. Economic gaps are widening due to the ongoing pandemic, and different consumer groups often have different needs.

Money Management Challenges Differ for Diverse Consumers

During the pandemic, racially diverse groups are reporting that they are ending up short each month, without enough money to cover their bills (23% vs 16% of whites), according to our Future of Money Study. This is resulting in these consumers tapping into savings more, with 33% reporting accessing savings to cover bills. But as Pew Research Center notes, many diverse groups do not have financial reserves to fall back on to combat the impact of job loss or reduced hours on their bills.

According to CNBC, a high percentage of Latinx households (86%) and Black households (66%) are reporting serious financial problems like trouble paying bills and depleting savings, compared with 51% of white households reporting the same. Truly understanding consumers — and their current needs in the face of savings depletion and monthly expense shortages — is key to financial institution response.

Key Point:

What are diverse racial groups telling us they need from their banking provider right now? Help and support.

Read More: How Banking Providers Can Help People Gain Economic Peace of Mind

How Banks and Credit Unions Can Assist Diverse Constituencies

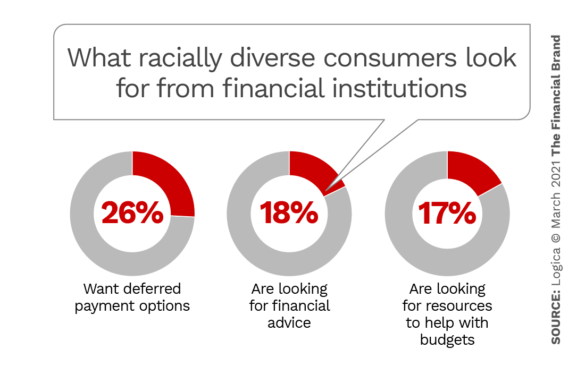

Even if the massive global vaccination campaigns are successful in tamping down the spread of COVID, the pandemic’s economic fallout will continue for some time. More and more people are turning to their financial institutions looking for help, with a higher percentage of diverse racial groups looking for very specific assistance from their banks and credit unions. 26% of such groups report a desire for their financial institution to defer payments (versus 15% white); 18% would like their banking provider to offer more financial advice (versus 12% white); and 17% want their financial institution to provide resources to help them with their budgets (versus 11% white).

3 Steps to Meet the Banking Needs of Diverse Groups

- Step One: Take a deep dive into understanding your customers, especially those from racially diverse backgrounds who have been impacted by COVID. Their needs are different during this time.

- Step Two: Identify ways you can help people with their needs today, deepening trust with them. These may include help with budgeting, digital tools, and financial advice.

- Step Three: Follow up and continue to evolve your communications and product offerings, showing an ongoing commitment. In many instances, economic challenges stemming from the pandemic will take time to overcome.