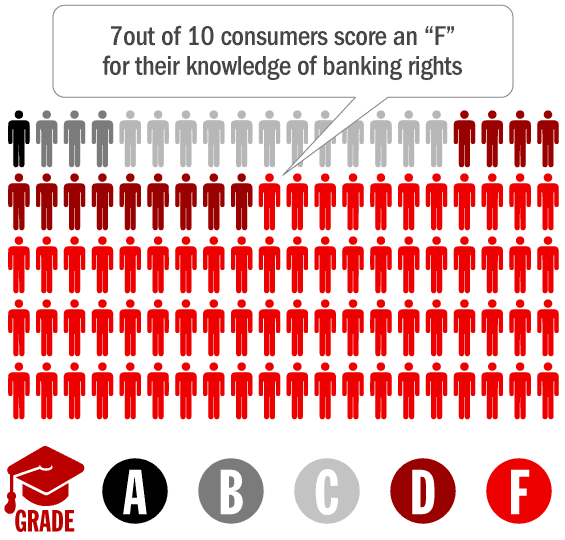

A survey of U.S. bank customers conducted for FICO found that only 30% of consumers got a passing grade when it came to knowledge of their financial rights. In the survey, consumers were asked 12 questions about their banking rights. Out of nearly 1,000 respondents, only ten of them earned an “A” grade, scoring 92% correct. Another 30 people scored a “B” (83% correct).12% got a C (with three-quarters of their answers correct), and 14% got a D (with two-thirds of their answers correct). That means 71% of consumers are flunking.

Consumers were stumped on a broad range of topics. 81% thought a credit reporting agency did not need their written consent in order to provide their credit report to their employer. 79% did not know that debit card transactions are protected by the federal government. 78% did not realize that consumer information agencies can report negative information that is more than three years old. 75% did not know that while settling credit-related disputes, their credit rating is protected by the government. 74% of consumers thought they could always get access to their files at a credit reporting agency for free. Half of respondents did not know that if they are denied credit, they can receive a free credit report within 30 days of denial.

Consumers were better informed on other topics. 73% of respondents knew they have the right to dispute inaccurate or incomplete data on their credit report. 69% knew that if their bank fails, their savings/checking account is protected by the federal government. 69% knew that information on annual percentage rates and annual fees must be included on applications for new credit cards. 60% knew their bank must send them information if a rate increase occurs on their adjustable rate mortgage. 57% knew that their bank must send information about annual fees prior to renewal of a credit/charge card. And 55% knew that if they are denied a credit card or auto loan, their bank must send them written notification explaining the reasons for the denial.

As a group, younger consumers fared worse than their parents’ generation. Only 48% of Millennials (aged 25 to 34) could answer half the questions correctly, while 57% of Generation X (35-50) and 62% of those over 50 years old answered more than half of the questions correctly.

Consumers who answered at least 50% of the questions correctly were also more satisfied and engaged with their primary banks than those who did not. The consumers who were most satisfied with their banks answered on average 47% of the questions correctly and the consumers who were most engaged with their banks answered 50% correctly. In contrast, disengaged consumers answered only 42% of the questions correctly, and unsatisfied consumers answered only 40% of the questions correctly.

“The study showed a correlation between financial literacy and better customer engagement, more use of bank services and decreased likelihood to switch banks,” said Anthony Sprauve, senior consumer credit specialist of FICO. “Educating consumers, especially Millennials, about their financial rights makes good business sense. Basic financial literacy equips consumers with the knowledge and confidence they need to make responsible financial decisions at all stages of their lives.”

The survey of nearly 1,000 U.S. banking customers was conducted online between March 5 and March 15, 2014.