To explore trends affecting the retail banking experience, PeopleMetrics compiled customer feedback from both banks and credit unions, then examined how consumer behaviors and preferences change based on a customer’s age. Here are a few highlights from this analysis, and some ideas on how to put these insights to work at your financial institution.

The Financial Services Consumers Need Evolve With Age

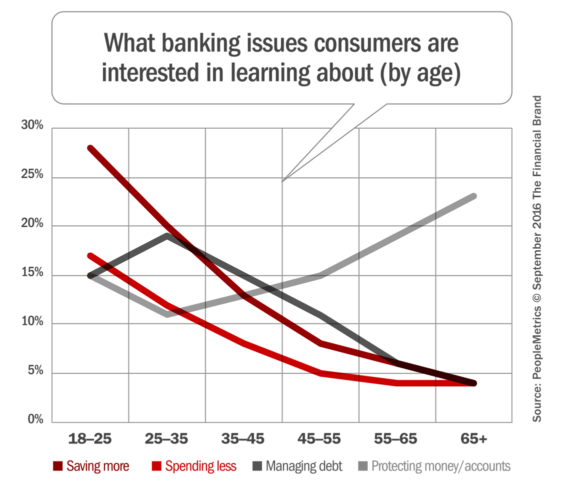

Money is very personal. And how someone relates to it shifts dramatically over their lifetime, right along with their health and family responsibilities. So it’s no surprise that age has a meaningful impact on consumer behaviors when it comes to retail banking products and services. The chart below is a fantastic reflection of just how much a person’s financial priorities change with time.

You see younger consumers primarily concerned with saving. But even among Millennials (18 to 35 year olds), behaviors are already changing. Older Millennials show less concern with saving. By age 30, many people are on an established career path and their financial concerns are already beginning to shift.

From 35 on up, you see people showing increased concern with protecting their assets. Generation X is building their wealth, while Baby Boomers are concerned with protecting it, and both groups want their financial partner to help them. Smart banks and credit unions are rolling out services specifically geared toward the security/protection concerns of the older demographic segment.

Age Correlates With Channel Usage

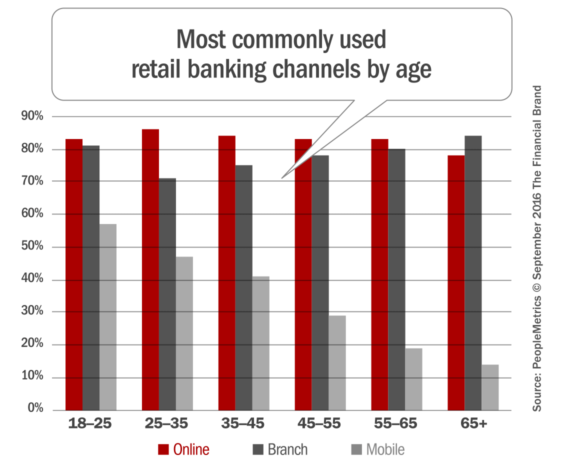

Now this can be a little tricky. Much has been made about how Millennials prefer online and mobile banking, and this was reflected in the PeopleMetrics research as well.

As you can see in the chart, an upward tick in branch usage occurs beginning with customers at age 25. While it’s a safe bet that Millennials will always be more comfortable with technology when they are 65 than Baby Boomers, as Millennials age, their financial needs will become more complex, and their channel preferences will change as well.

Cam Marston, a generational expert, brings up some similar considerations:

“Money has always been intensely personal and will continue to be so — both for Millennials and future generations. That means bankers may want to be wary of jumping to conclusions based on the current behavior of Millennials. In fact, the younger generation may turn out to have a lot more in common with older generations as they transition through the next stages of their lives. As with all generations, when you have little money, you tend to cherish what you have, manage it closely, and safeguard it. And, when you have more money… you do the same.”

The bottom line? As Millennials take on increasingly complex financial lives, the ways in which they interact with their banking providers will change as well. Just because they prefer self-service and digital technologies today does not mean they will have the same preferences and priorities in the future.

The Older You Get, The More Help You Need

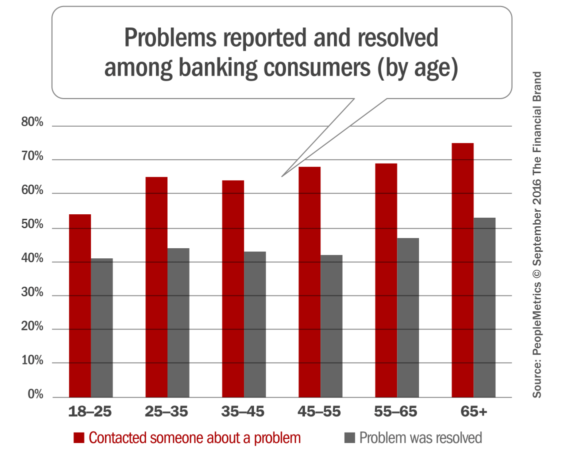

Differences manifest again when consumers encounter a problem and need service/support. The chart belows shows a correlation between age, how much support they need, and whether their problems were resolved.

Splitting this analysis out by age reveals just how much consumer behavior changes over time. Half of young Millennials (those ages 18 to 25) have contacted their financial institution about a problem, and most of those say their problem was ultimately resolved. Contrast this with Baby Boomers, where 75% contacted their banking provider about a problem, and only half of them got their problem resolved.

Increased willingness to get in touch with customer support as someone ages may reflect an ever more complex set of financial needs. As a person ages, the scope and size of their financial situation increases — more important assets to protect — so consumers no longer just cross their fingers and hope a problem will resolve itself on its own. Of course, this also begs a question: If younger customers aren’t contacting you about problems, how can you resolve them? Coupled with the fact that Millennials are the least loyal segment, this presents some challenges that could affect long-term retention.

For younger consumers in particular, banks and credit unions should be looking for ways to proactively identify and solve problems. That might include systemic alerts when a mobile deposit is declined or an account is overdrawn, so a support rep can proactively reach out to the accountholder. Or you might consider seeking feedback from various age segments on a regular basis.

Look Beyond Those Averages

Statistical averages feel reliable though, don’t they? It’s comfortably reassuring to hear something like “75% of people think this” or “42% do that.” But as marketing analytics expert Avinash Kaushik says that “the interesting thing about averages is that they hide the truth very effectively.” The real truth — truth you can make decisions on — often lurks at a layer deeper.

Consumers’ financial concerns change dramatically as they age, as well as their expectations affecting their interactions with their banking provider. As you think about how to deliver a better experience for your customers, you’d be smart to keep age front of mind. When you hear statistical facts, the first thing you should wonder is: “How would this data look if it were parsed by age?”

Age continues to be a valuable segmentation tool that can help financial marketers identify actionable insights that can be concealed by broader averages. For example, on your next customer survey, you may consider asking those over the age of 50+ how satisfied they are with your services when it comes to helping them protect their money and their accounts. Or you may work to identify the 14% of consumers age 65+ who use your mobile banking channel, and find out what features they’re like most, what they don’t, and what you could do better.

The data behind averages holds valuable insights on customer behavior. Go, find it, and act on it.