In the blink of an eye the world of retail banking has changed. Traditional branch banking, long a pillar of the sales strategy for financial institutions, has all but disappeared. Furthermore, consumer habits and behavior have permanently changed. When the current health crisis is finally behind us, we will not be returning to the high-touch world of the recent past.

Retail executives across industries know this and are racing to improve their digital sales, service, and fulfilment capabilities in the knowledge that digital-first is the only viable strategy for continued survival. For banks and credit unions that have long relied on relationships and consultative person-to-person (P2P) selling practices, a rapid shift in channel priorities and tactics will be necessary to remain viable.

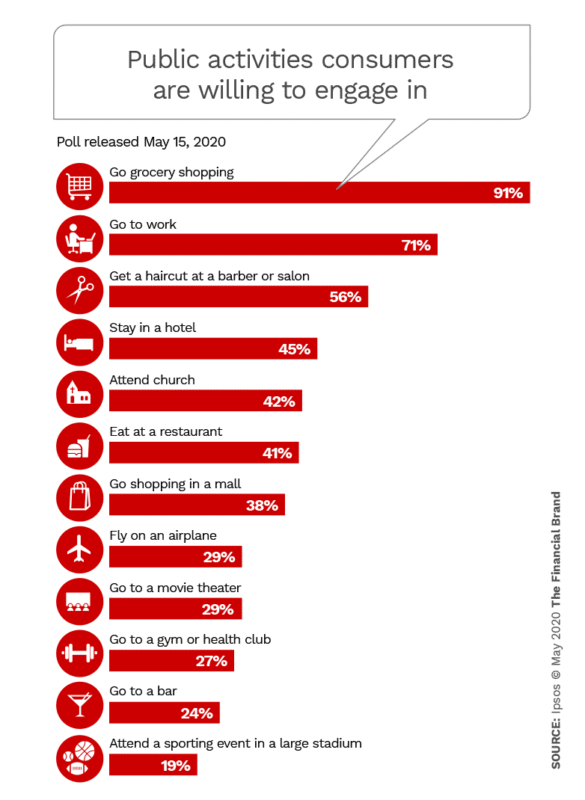

Data and polling reinforce the consensus view that consumers will not be returning to the branch anytime soon — if at all. An ABC News/IPSOS poll released May 15th asked how likely consumers would be to venture out in public if restrictions were lifted tomorrow.

The only activities that more than half the respondents were willing to resume included going to work and getting a haircut. More than a third indicated that they were unlikely even to send their kids back to school.

Where there are safer and more convenient options, a branch visit is quickly and permanently becoming the channel of last resort.

In other brick-and-mortar retail segments, digital has grown quickly. Target CEO Brian Cornell observed that their digital sales through the first three weeks of April were up 275%. Target, a leader in BOPIS (Buy Online Pick Up In-Store), saw Cyber Monday occur almost every day, except the volume was twice the size. Even Costco, the star retail concept of the 80’s and 90’s that today maintains what is arguably one of the most basic e-commerce sites of any major retailer, saw on-line sales grow 48% in March.

Seven Drivers of the ‘New Normal’

With customers not returning to the branch and digital having gained a prominence that will not be surrendered, what will the new normal be in retail banking? Here are seven key elements from the emerging consensus:

1. The FI’s website will be the undisputed “primary branch.” The website will be the exclusive domain for shopping, educating, and comparing between competing financial institutions and product offers.

Consumers’ impressions of a bank or credit union and decision to purchase will be directly influenced by website usability and functionality, with a heavy emphasis on the ease of answering their personal financial questions, shopping, and comparing different products. Websites that fail to meet these table-stakes requirements will quickly be abandoned in favor of more helpful brands.

( Read More: Guided Selling solutions that help financial consumers self-select the right product )

2. Self-service digital will command an increasing share of new account relationships. A greater percentage of customer engagements will have no person-to-person relationship component and will rely entirely on the digital experience.

3. A segment of customers will seek to maintain an in-person relationship with their financial institution. There will be some customers that will want to establish or maintain a P2P relationship with their banker outside of the branch. This group will comprise a mix of higher-needs customers for whom digital self-service or the relationship afforded by the call center alone will not suffice. For this segment, banks and credit unions will need to offer tele-collaboration tools which bring the traditional customer branch experience to a digitally enabled one.

4. Branch locators will be replaced by banker locators. Customers will no longer use a mobile banking app to look for a building. Instead, they will look for a local banker that is well regarded and easy to contact directly via the website when they seek a P2P interaction to address a financial need. The banker will need to be able to help the customer from the point at which they left off on their self-service journey. (See: BankXpert and CU Xpert for connecting digital shoppers to bankers.)

“The geographically indifferent digital playing field will now be where banking business is won or lost.”

5. Geography will be less meaningful. Banks and credit unions that have relied on a local branch presence as a counter to better digital experiences from outside competitors will find this advantage rapidly eroding. The geographically indifferent digital playing field will now be where business is won or lost.

6. Investment will be required. Providing all of the capabilities now required in this digital-first age will not come without a significant investment. Fortunately, many of the nation’s banks and credit unions have strong balance sheets and are well positioned to make transformative investments in their digital channel.

7. Digital transformation is about talent and technology. In addition to technology, investments in expertise will also be required for a successful digital transformation. Whether in-house or in partnership with vendors, many banks and credit unions will need to seek additional expertise to help in designing the way forward.

Local Knowledge and Touch No Longer Enough

To serve and compete in a post-pandemic world, banks and credit unions must start immediately to ensure their existing web and digital capabilities are best-of-class competitive, with full resources for customers wishing to research, shop, and compare. Attention must be paid to interactive learning, investigative and selling tools, as well as basic servicing functionality.

A profound re-thinking of the customer journey from a digital starting to a digital ending point will be required.

No longer will credit unions and community banks be able to depend on the value of personal banking relationships and intimate knowledge of local markets; they’ll also have to build robust digital front doors that compete with the larger national banks.

“We’ve seen two years’ worth of digital transformation in two months,” observed Microsoft CEO Satya Nadella about the impact of the pandemic. Banks and credit unions that move quickly to position themselves for this new reality have the opportunity to turn this crisis into opportunity.