In a presentation to financial institution executives, Scott Edwards, Marketing Director at Simple, described how Simple is trying to meet the growing expectations of their customers. Unlike most other organizations that have built their mobile banking solution as an outgrowth of traditional branch and online banking processes, Simple built their solution with a mobile-first perspective, following the lead of non-financial firms who have great mobile experiences.

Everything at Simple is designed to drive out complexity and make sense to the customer. From product design, to marketing, to customer service, each move is made by considering the consumer’s point of view, not necessarily the bank’s view.

By learning from Simple’s approaches, financial institutions can be inspired to build products based on how consumers want to use their smartphones, manage their finances and connect with their bank or credit union.

“Great retailers not only have better products, but they’re training consumers to have higher expectations. They’re training people that they can get anything they want, at any time, anywhere in the world.” – Scott Edwards, Simple

The following are some of the ways Simple continues to try to improve the mobile banking experience.

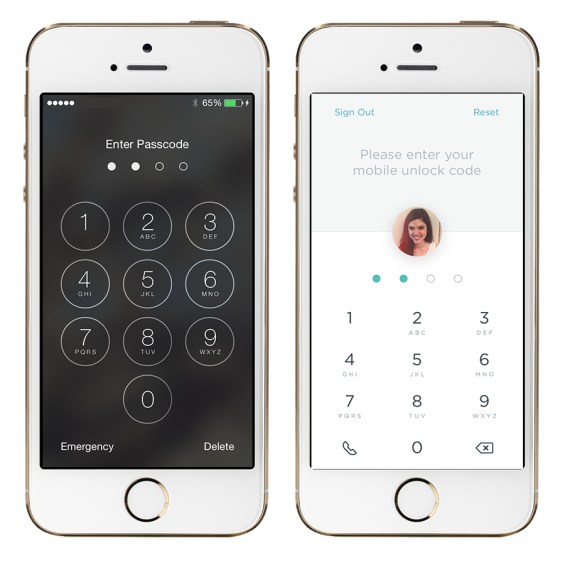

Passphrase, Mobile Unlock Code and Touch ID

When creating an account, consumers are able to choose a “passphrase” — a phrase with words separated by spaces, rather than a commonly used one-word password. After the user initially signs into the app using that passphrase, they simply enter a 4-digit “mobile unlock code” each time they revisit the app.

This is designed very similar to how consumers already interact with their phones every day — they slide and unlock with a 4-digit “passcode.” Not a 4-digit “pin” and not a 6+ digit password with $peciaL characters.

Even faster access has become available with Simple 2.1, the version of the app optimized for iOS 8. The app includes Touch ID, allowing consumers to use their fingerprint as a passcode. Plus, thanks to Simple’s partnership with 1Password, a separate app that conveniently stores all of the user’s passwords in one place, consumers can use Touch ID for both sign in and app access, eliminating the need to ever re-enter the passphrase or unlock code.

Using this type of relevant, up to date mobile technology is a perfect example of designing for the customer, not the financial institution.

Support for Wearables

While the market for consumers using wearable computing devices may be comparatively small, Simple is supporting real-time financial capabilities to more than just a phone. Simple customers now can receive push notifications on both an Android smartphone and Wear device, seeing push alerts and transaction notifications immediately on their watch. It is anticipated that Simple will follow suit with the Apple Watch as well.

“No Longer My Banking App. Just My App”

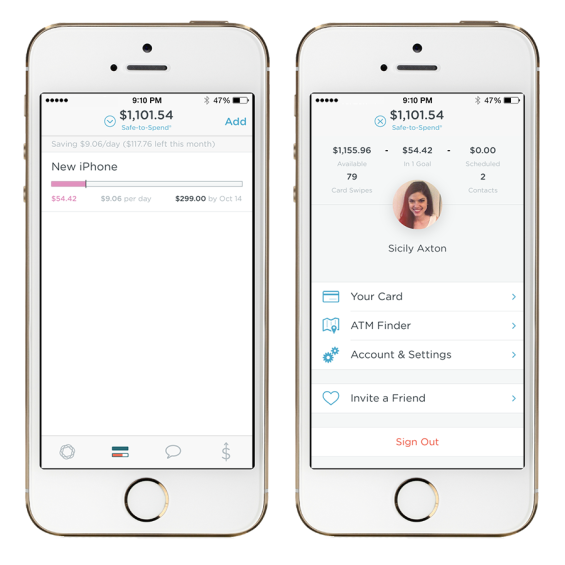

Notice the selfie on the login screen? From pictures to budgeting, Simple understands how personalization can transform a product into becoming part of the consumer’s lifestyle.

Let’s say a consumer wants to budget every transaction during a business trip to Orlando. They can use the hashtag #orlando with all purchases, grouping all expenses and allowing for a future search of transactions the way consumers are used to doing. Most bank apps don’t provide the opportunity to customize categories, but instead automatically categorize by transaction types … such as checks, deposits, ACHs, direct debits, etc.

This, along with the Safe-to-Spend feature, allows the app to become customized for a consumer’s personal goals.

If the consumer sets a financial goal, the app only presents the Safe-to-Spend amount – not an available balance – putting desired saved money in the Goals section. This allows for easy budgeting and saving, making sure the consumer doesn’t spend money they would rather not spend if the goal is a priority.

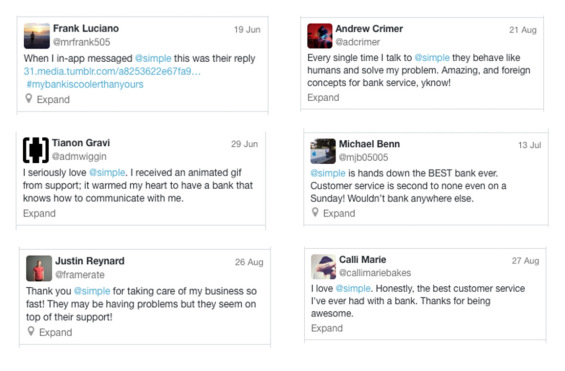

In-App Messaging For Customer Service

According to research by Simple, consumers have a 5 to 1 preference for in-app messaging for customer service allowing for a conversation, rather than a series of message exchanges.

Instead of asking the consumer to send an email or message that disappears and gives no evidence that it was even sent, leaving a history of the conversation within the app holds Simple to more accountability and allows consumers to easily recall that their issues were resolved. Plus, those positive experiences can’t help but be shared.

While some Simple customers expressed concern after back-end technical issues at Simple, there are plenty of loyal fans expressing their love of the Simple app.

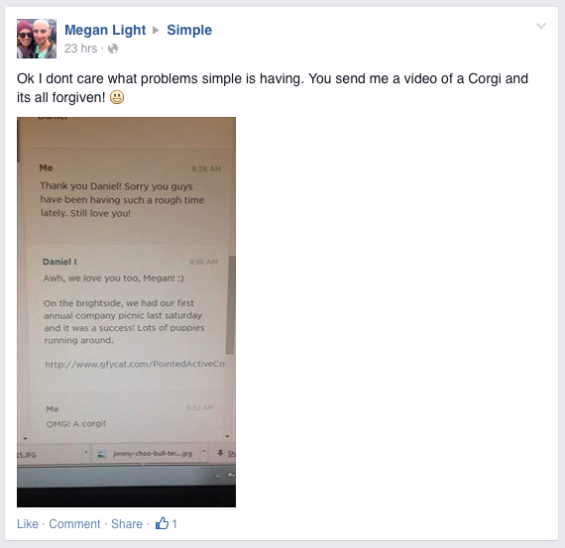

Being Human

In the world outside financial services, communication between a solutions provider and the consumer are expected to be human, using human terms and human language. Unfortunately, that is not usually the case between a bank or credit union and a consumer. We tend to fall into a form of ‘bank speak.’

The best way to speak in ‘human terms’?:

- Remember that people don’t buy what you do, but the benefits you provide. Talk less about product features and more about the benefits offered.

- Don’t expect consumers to learn our bank terms. Describe accounts and features in ways everyone can understand.

- Use inspirational language and help consumers validate their choice to bank with you.

- If your mobile app is easy to use, show how it works. Use a short demonstrative video (optimized to mobile) to teach people how to use your product.

#dogshaming

As Simple’s customer service began getting calls from people to replace their debit cards, on occasion their reasoning would be “my dog ate my debit card.” With a focus on humanizing the banking experience, Simple decided to have some extra fun with those customers and ask for pictures of the culprits. In response, more and more people were glad to send in photos of their guilty, yet adorable pets.

Simple seized the opportunity to dig deeper into their customers’ stories and allowed their own users to inspire social media interaction that also marketed their product in a personal and unique way. They even collected enough material to create a “wall of shame” in the Simple office dedicated to just dog shaming pictures.

One Consumer, One Account, Many Devices

Eliminating too many account choices with too much complexity makes the purchasing decision easy for the consumer at Simple. And, while Simple recognizes how important mobile is to the experience of the digital consumer, they still support the online channel. As with mobile, Simple leverages the best of their online banking capabilities, such as providing infinite scrolling of transaction views similar to the design of a Facebook News Feed.

When the customer visits Simple.com in a browser on a mobile device, smart app banners are used to redirect the customer to the app. So while multiple platforms are available to access the one account, the consumer is encouraged to use the channel that’s best suited for the experience.

Learn From Your Competitors

Without understanding the products of other financial services companies, retailers and other heavily used mobile applications, banks and credit unions can’t effectively compete. Edwards shared features from other mobile financial tools like Acorns, Square and Betterment that are building experiences other financial services apps aren’t.

Simple is also dedicated to measuring their own key insights. By studying bounce rates, for example, they can use retargeting tags to show ads to visitors who abandon the sign up process. They also study time spent on the page, click throughs and conversions, plus use Facebook Custom Audiences to generate lookalike audiences for low cost advertising.

Financial services marketing and customer usability can no longer be afterthoughts, but instead, they need to drive everything that we do. So while companies like Simple are teaching consumers to have higher expectations of banks, the banking industry has to also have a higher expectation of the role that marketing plays in the success of our industry.

Sicily Axton is the communications manager for StrategyCorps, a Nashville-based company that works with financial institutions nationwide to deliver mobile and online consumer checking solutions that enhance customer engagement and increase fee income.