While convenience is the primary benefit cited by mobile banking customers, security fears remain the number one barrier to mobile banking growth. As opposed to a ‘one-size-fits-all’ approach, financial institutions should consider segmenting the mobile banking universe for improved resource allocation and to optimize customer acquisition, utilization, retention and differentiation.

Mobile devices, including smartphones and tablets continue to transform the way consumers bank, budget, make payments and shop. In fact, having a mobile banking offering is now considered ‘table stakes’ to consumers when selecting a financial institution. According to the 2013 Federal Reserve Consumers and Mobile Financial Services Report:

- 87% of the U.S. adult population has a mobile phone

- 52% of the mobile phones are smartphones (internet-enabled)

- 87% of smartphone users access the internet regularly (in the past week)

- 28% of mobile phone users have used mobile banking over past 12 months

- 48% of smartphone users have used mobile banking in past 12 months

While some financial institutions may be satisfied with this level of acceptance, mobile banking leaders understand that checking balances using a phone is not ‘full engagement’ and that growth of use beyond this level will require a better understanding of the mobile customer base and the barriers that keep non-users from using mobile banking. Banks and credit unions also realize how important this understanding will be as they try to optimize channels, reduce operating costs and identify new revenue sources.

According to a report released by Monitise and Cognizant entitled Segment-Based Strategies for Mobile Banking, financial institutions need to better understand the mobile banking customer universe and may want to consider segmenting their customers based on mobile adoption, desired features and benefits, mobile devices and monetization potential. By segmenting the mobile customer base, the following questions could be answered:

- What is the best way to segment the mobile customer base?

- How do mobile adoption levels vary across consumer segments?

- What mobile banking features and applications are preferred and by whom?

- How do tablet users differ from smartphone users?

- What opportunities exist for further monetization?

- How can the mobile channel be leveraged for differentiation?

Understanding the Mobile Banking Consumer

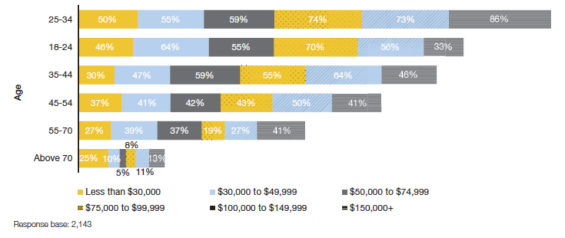

Despite all of the industry discussion around the importance and growth of mobile banking, adoption levels still only average 33% across all segments and age categories. While younger, wealthier and more tech-savvy consumers are more engaged with the mobile channel, the challenge is to replicate these higher adoption levels with other segments.

As can be seen above, the highest adoption rate for mobile banking is in the 25-34 age bracket with annual income above $75,000. Mobile banking is accessed primarily through mobile phones (32 percent) and tablets (7 percent), with 24 percent using both devices. As can be expected, the majority of consumers prefer smartphone and tablet apps as opposed to mobile banking web sites to access their accounts. The very oldest segment prefers text banking.

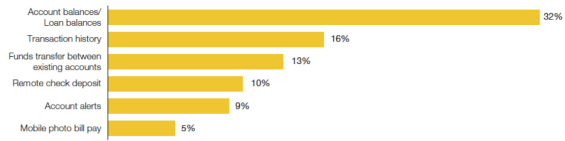

Consistent with the reality that the mobile banking channel is still in its relative infancy, the primary features offered by banks and desired by consumers are aligned around basic banking transaction functionality. Unfortunately, these functions have minimal potential for differentiation and do not increase engagement that will reduce potential attrition. In other words, these are nothing more than table stakes.

To move beyond a standard mobile banking offering, banks and credit unions need to provide increased functionality. We are beginning to see a response to this need with the introduction of remote check deposit and increased promotion of real-time alerts and advanced bill payment. The impact has been that some consumers are beginning to switch financial providers based on these features according to the research from Monitise and Cognizant.

More than 75% of the consumers surveyed also found the ability to personalize their experience important. Similar to the way in which financial institutions allow consumers to customize their ATM experience, consumers want to be able to rearrange tabs and functions within their mobile application, change appearances of their app and other customization.

While this personalization may feel like window dressing, the research believes these capabilities could increase retention similar to personalized debit and credit cards.

Security Concerns Remain Primary Barrier and Opportunity for Mobile Channel Growth

As innovator and financial industry futurist Brett King says, “Banking is no longer somewhere you go, but something you do.” With more consumers moving away from the branch network, concerns surrounding mobile banking security remain the primary barrier to widespread adoption, especially in key demographics. This challenge can become an opportunity, however, for banks that provide enhanced security capabilities or possibly even guarantees.

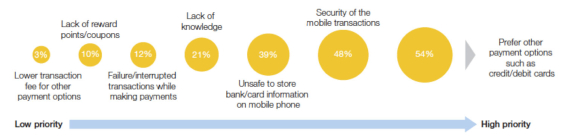

According to the research conducted by Monitise and Cognizant, 71% of respondents rated security features as ‘highly important’ in choosing or switching banks. Security is a major concern with mobile banking users (70%) and is the most important consideration for non-mobile banking users.

Security concerns are not only prevalent with mobile banking usage, but are the most significant deterrent to mobile payment usage (the most engaging mobile banking function). Based on the results of the research, it appears there may be an opportunity to gain mobile payment usage if banks provided safeguards and guarantees for mobile transactions similar to those provided with card transaction. Otherwise, the value proposition of conducting a mobile payment vs. card payment does not seem to be present.

The challenge is that consumers expect ease-of-use and seamless operation while also wanting effective security practices. These desires can conflict at times where multiple authentication processes are implemented. At this time, it doesn’t appear any bank or credit union has found the perfect mix of security and simplicity.

Interestingly, mobile banking users appear to be ahead of the financial community in their desire for advanced security technology. According to the Monitise and Cognizant research, 68% of respondents believed biometric security features are important, while 35% noted that they are willing to pay for such protection. Of the different biometric options surveyed (fingerprint, voice and facial recognition), Fingerprint matching was the overwhelming favorite of most consumers.

An area where banks and credit unions could respond to the consumer’s desire for personalization as well as providing a high-engagement security solution would be through mobile alerts. According to the research, the demand for these types of alerts is prevalent across all income segments.

Mobile Security Options

While this post is not intended to discuss how banks should proceed with mobile security, there are good references available that discuss options.

In an excellent report in Bank Systems and Technology entitled 5 Critical Strategies for Mobile Banking Security, it was emphasized that banks and credit unions are challenged by the somewhat conflicting consumer desires for increased security and increased ease of use. Based on interviews with leading industry analysts from Forrester Research, Mercator Advisory Group, Aite Group and ABI Research, possible strategies were provided:

- Risk-based authentication and anomaly detection

- Application based security features

- Out-of-band authentication (separate device)

- Mobile operating system security

- Expanded defense minded devices

While Bank Systems and Technology acknowledged that it would be simple to suggest that banks go all in with all five strategies, that’s not a viable option for resource-constrained financial institutions, which need to make trade-offs and allocate security budgets based on customer needs, mobile strategies and marketplace dynamics.

Tablet Banking Differentiation

Until recently, many banks simply expanded the dimensions of their mobile phone banking application for tablet use. But tablets are quickly emerging as a user interface which provides unique challenges and opportunities for financial institutions. According to the Monitise and Cognizant research, 41% of mobile banking consumers would prefer to use their tablets as opposed to their smartphones. This preference increases to 60% among tablet owners and is even further pronounced among affluent consumers.

The research stresses that consumers use their phone and tablets for different purposes. While smartphones are used for more simple and immediate needs (balance inquiries, balance transfers, etc.), tablets are less transaction-driven and are used more for personal financial management (PFM) functions. The tablet’s unique functionality also provides an excellent platform for advanced cross-selling and relationship building.

Mobile Banking Segmentation

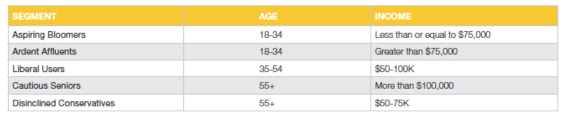

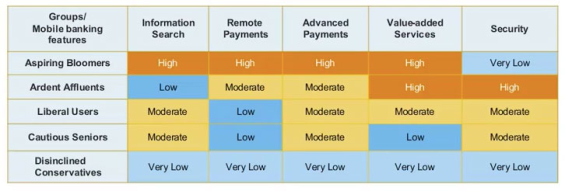

The Monitise and Cognizant research identified five consumer segments based on the use of mobile banking services, age and income level of the consumer. While this segmentation may not be perfect for every organization, it is a very good starting point for identifying mobile banking segment needs and ways to increase usage and wallet share.

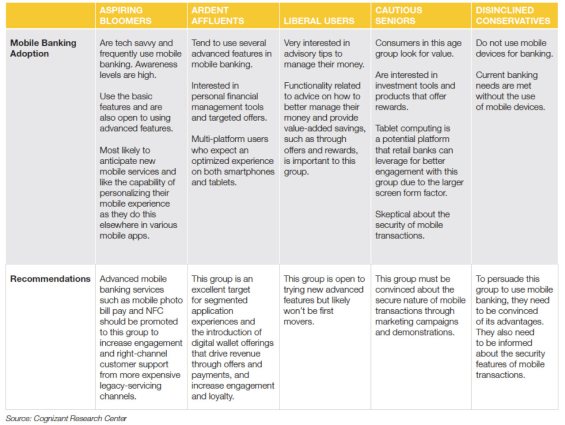

Aspiring Bloomers. This segment is digitally inclined but not among the first to adopt mobile banking. However, they access mobile banking services at least once a week. Mobile banking features such as checking account balances, transferring funds and remote payments are important. Consumers in this segment are willing to try and adopt advanced features such as mobile photo bill pay, virtual wallet services and near-field communication payments. To retain and further penetrate this segment, retail banks can educate these consumers about advanced features through direct marketing campaigns.

Ardent Affluents. This segment is highly engaged with their mobile devices. They use advanced features such as mobile photo bill pay, and are interested in receiving expert guidance on personal finance and investments. They seek value-added services such as spending pattern analysis, loyalty rewards/points, shopping updates and portfolio monitoring. Sustaining this segment’s interest in mobile services by keeping up with their innovation needs can help retail banks acquire and retain this segment.

Liberal Users. This segment consists of consumers between the ages of 35 and 54. Their average annual income is between $50,000 and $100,000. They use mobile banking, but not extensively. They also seek advice to help them improve how they manage their finances. This segment will respond best to services related to money management.

Cautious Seniors. These consumers are value seekers. They are interested in products that offer tangible rewards. This segment is also highly sensitive to mobile security concerns. To make mobility more palatable to them, retail banks can extol the virtues of mobile banking, including its safety and security.

Disinclined Conservatives. This segment has serious concerns about the safety and security of mobile transactions. Currently available banking services meet their existing needs. Retail banks can gain from informing them about the benefits of mobile banking and alleviating their security concerns. This could encourage this segment to try mobile banking.

Addressing the needs of individual segments (or deciding to ignore some segments) provides the foundation to increase adoption of mobile banking services within a bank or credit union. By targeting efforts to specific segments, as opposed to marketing to all consumers in the same way, will better optimize marketing investments and lead to quicker returns on investment.

Based on the research, the following recommendations were provided to mobile banking developers and financial marketers:

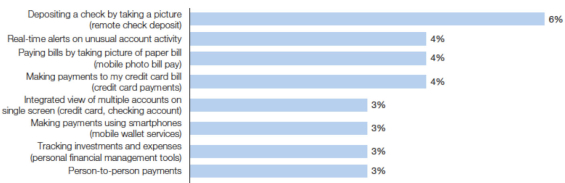

- Remote check deposit should continue to be promoted due to being rated as the most important mobile banking feature

- Additional innovation must be ongoing since consumers are making buying decisions based on mobile capabilities

- Real-time, customizable alerts should be given top shelf attention and promoted aggressively due to their importance as a security and financial management tool

- Other security features need to be enhanced and promoted. This is the key to future mobile banking (and mobile payment) adoption

- Personalization of the mobile experience should be given priority since this can reduce attrition

- All functionality should be simplified on the mobile platform. This is especially true of mobile payment processes that do not provide additional value compared to alternatives today

- Tablets applications should be customized, with capabilities matching the advanced functionality of the channel

- Leverage advanced technology for a better user experience (online chat, voice activation, videos, etc.)

- Segmented customer experiences addressing the unique needs and usage of the various segments similar to the recommendations below.

Survey Methodology

This survey was conducted online among a nationally representative sample of approximately 2,100 U.S. consumers, roughly 700 of whom are mobile banking users, during March and April 2013. Data was collected on mobile banking sentiments, preferred features of smartphones and tablets, attitude towards mobile payment services and the major concerns regarding mobile banking.