Technology companies continue to impact the way people socialize, purchase goods and services and even bank. With each new iteration of the smartphone, or introduction of new digital applications, proactive organizations have integrated the best new innovations within their solutions. From one-touch purchases at Amazon, hailing a ride with Uber, or making P2P payments with Venmo, consumers appreciate these ‘new and improved’ digital capabilities that can make their lives easier.

The banking industry is no different (albeit somewhat slower to embrace new technologies). Different perspectives on the urgency of innovation have created a gap between ‘early movers’ and self-proclaimed ‘fast followers.’ A great example is the introduction of voice banking functionality by Capital One, American Express, RBC, Moven, USAA, Paypal and others. While there is a vast consumer acceptance of digital assistants overall, the majority of banking organizations have been slow to embrace digital voice technologies.

Over the past ten years, smartphones have disrupted almost every part of the banking experience. From checking balances, to transferring funds and paying bills. From shopping for and opening a new account, to applying for a loan. Even depositing a check and managing a budget, a consumer can do all of their banking without ever setting foot into a branch.

With the introduction of the iPhone X, is a new wave of mobile disruption about to occur? And will the banking industry participate?

Read More: America’s Smartphone Obsession

Demand for the iPhone X

While the iPhone 8 models come with brighter screens, better cameras, and faster processors, the real innovation in the new Apple line-up of smartphones comes from the iPhone X model. The anniversary version features a larger 5.8 inch super retina screen that fills the entire face of the phone, a biometric security face recognition feature, and a new augmented reality software and developer kit. The new iPhone X provides banks and credit unions with the opportunity to completely re-engineer mobile customer experiences. But, will there be a consumer demand for these services?

First, we need to look at the sales figures for the new phones. The iPhone 8 and iPhone 8 Plus were both made available for pre-order, yet analysts believe that pre-orders for these phones are weaker than anticipated because of consumers waiting to buy the iPhone X. Although the iPhone X is the most expensive iPhone ever ($999 starting price), it appears that consumers eligible for an upgrade will be willing to pay for a brand new generation of phone with unique functionality. If this is true, the first organizations to leverage the new capabilities will be able to differentiate their mobile banking offering to a larger than expected consumer base.

Enhanced Visuals and Performance

Possibly the most dramatic feature of the iPhone X is the high quality OLED screen, with an edge-to-edge “Super Retina Display” and 1125 x 2436 pixels of resolution. In addition, the new A11 processor has speed performance unseen in any other smartphone. In fact, the iPhone X’s new chip is considered to be more powerful than the Intel chips powering some of Apple’s newest MacBook Pros.

The higher resolution screen not only provides financial institutions with a larger palette to build upon, but the clarity and speed that will make a difference as consumers transact business. From enabling complex calculations, to providing improved video (or virtual assistant) viewing, there are new opportunities for enhanced mobile engagement.

Facial Biometric Authentication

In 2013, Apple introduced its TouchID fingerprint authentication system as part of the iPhone. Since then, many retailers, travel organizations, healthcare providers and financial services organizations updated their mobile apps to allow customers to use their fingerprint to validate their identity.

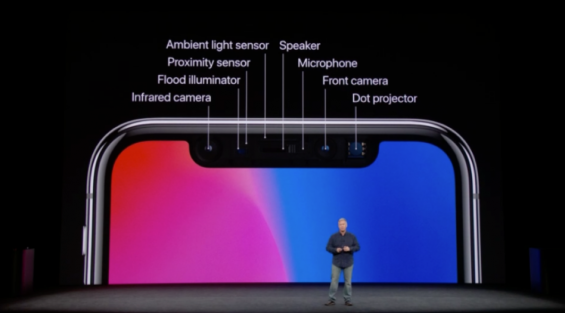

The iPhone X takes biometrics to the next level, by introducing facial recognition technology (FaceID) to unlock the device and authorize transactions. FaceID captures a 3D scan of a user’s face from all angles using the front-facing camera, a dot projector and an infrared camera. It uses this biometric scan to authenticate users while they hold the device.

The main benefit of biometric security (fingerprint, face scan, iris scan, voice, etc.) is that it is more difficult for an unauthorized person to use the phone or access the data contained within. Biometric security is also popular because it eliminates the need for a passcode, making access easier for the owner. The reason for moving from touch to facial ID for Apple was both aesthetics and to improve security.

According to Apple, there is just a one-in-a-million chance of another person’s face being close enough to pass its FaceID test. This compares to one in 50,000 chance for its thumbprint scanner. The integration of FaceID could be an important differentiation for banks (and Apple) at a time when identity theft is becoming an increasingly serious problem.

While some organizations and phone manufacturers already offer facial biometrics (USAA, Citi, Samsung, Alibaba, etc.), others are testing alternatives such as iris scans and voice recognition. One drawback of biometric security is that if the technology is compromised, you can’t change your face, eyes or fingerprint as easily as a passcode.

Mobile and P2P Payments

Despite a lot of industry promotion from financial institutions and solution providers, the acceptance of mobile payments (especially in the U.S.) continues to fall far short of expectations. Beyond lackluster merchant acceptance, the value proposition of using a mobile device for payments has never been strong enough to change credit card and debit card user behaviors.

Apple hopes that FaceID will make Apple Pay mobile payments easier and more secure. As other P2P payment alternatives (Zelle, Venmo, Square Cash, PayPal) integrate facial biometrics into their processes, the concept of using a facial scan vs. a fingerprint will be more accepted. Apple’s new operating system (iOS 11) will also enable P2P payments with iMessage, making Apple Pay a direct competitor to these other P2P options.

Read More: The Future Hinges on the Mobile Banking Experience

Augmented Reality and Gamification

One of the less covered enhancements for the new iPhones was the introduction of a mainstream, mass-market mobile product that for the first time has an Augmented Reality (AR) engine baked right into the OS. Although AR is still relatively new as a mass market technology, consumers may be familiar with applications like Snapchat (which applies filters to a selfie), Pokemon Go, (which placed characters in live environments), or Google Translate.

There are several potential applications for the banking community. For instance, IKEA has developed an app, “Place”, that uses AR to simulate how items of furniture will look in your house, automatically measuring spaces and even replacing existing furnishings. What if a financial institution integrated financing information on top of an app like IKEA’s. How about the same application of the technology for a new car or house? Some financial firms already overlay property and financing details on a mobile device as prospective homebuyers pass a house for sale.

There is also the potential for gamification AR that can encourage saving, paying down debt or budgeting. For instance, in a panel discussion at Finovate, Tim Hong from the budgeting and lending app MoneyLion introduced a new feature called “Grow Your Stack.” With this feature, a consumer gets a visual interpretation of the power of saving over time with stacks of money. What would $1,000 look like? How about retirement savings of $250,000?

While some may consider this application of AR a bit simplistic, the connection of daily saving and the value of saving over time is made more personal (and fun) with visualizations made possible with AR.

Read More: Will Augmented and Virtual Reality Replace the Bank Branch?

Mobile Banking Leader or ‘Fast Follower’

In a great article written by my friend, JP Nicols entitled, “Leaders, Learners and Laggards,” he mentions that in his discussions with banking leaders, many describe their approach to innovation as being a “fast follower.” His response is that they are half-right — most of them are definitely followers, but there usually isn’t anything fast about their approach.

While many financial organizations may be concerned with avoiding and managing risk, the risk of sitting on the sideline may be greater as technology advances and consumer expectations follow lock step. Banks and credit unions must find new revenue sources and create better customer experiences. According to Nichols, “The gap between the laggards and the learners and leaders will only expand, and many laggards will be acquired by faster moving institutions.”

“Many laggards are simply unable to sense the shifting landscape, while others have willfully disdained what they perceived to be the riskier path of trying new things. The true cost of their inaction and ignorance will be borne out in the coming months and years.”

So, the question is whether an organization embraces the new innovations introduced with the iPhone X (and assuredly other big tech responses), or whether they sit and allow others to out-innovate and steal potential (and current) customers.