The financial institutions occupying positions 10 to 75 in the asset-size ranking of U.S. banks have increasingly been regarded as terminally challenged.

Their leadership is considered too traditional and conservative, the thinking of several observers goes, and they can’t keep pace with the investments in technology necessary for how banking is evolving.

No doubt there is some truth in these observations, but it’s also fair to say that asset size is no assurance of market success. Well-run institutions with forward-looking leadership and supportive shareholders can succeed no matter what size bracket they fall into.

Case in point is Huntington Bank. Founded in 1866 in Columbus, Ohio, the Midwest-focused institution has largely operated in the shadow of much larger financial institutions. Its merger with TCF Financial, announced in late 2020, thrust it into the spotlight, and will bring it into the ranks of the top 20 institutions by size at about $168 billion. (Pre-merger, Huntington’s total assets were $120 billion as of Q3 2020.) But even so, Huntington will still be just one-twelfth the size of Bank of America.

Well before its TCF deal was announced, though, the regional bank had been quietly putting the building blocks in place to fulfill its promise of being a “people-first, digitally-powered bank.” It has launched more than 100 digital products since 2018, and has invested heavily in the modern technology infrastructure needed to support that kind of digital advance. For 2021 management has committed $150 million for further digital development.

Much of the innovation has been on the retail side of the bank, headed by Senior Executive Vice President Andy Harmening, who also is responsible for small business banking and payments. He tells The Financial Brand that at the time he joined Huntington in 2017 they had roughly 100 employees on the bank’s digital and omnichannel teams. That figure now stands at close to 500.

“Our biggest risk is the status quo,” says Harmening.

Digital Banking Revolves Around ‘The Hub’

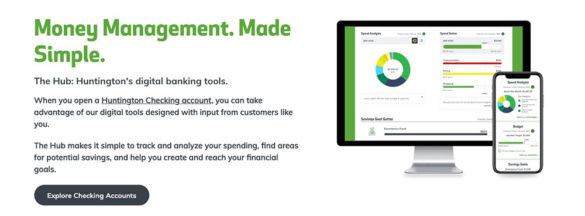

While Huntington hasn’t been first out of the gate on every digital feature, by any means, it’s been ahead of most financial institutions and sometimes even ahead of the biggest. Much of what if offers, especially in terms of advanced money management features, resides in an online and mobile dashboard it calls “The Hub.”

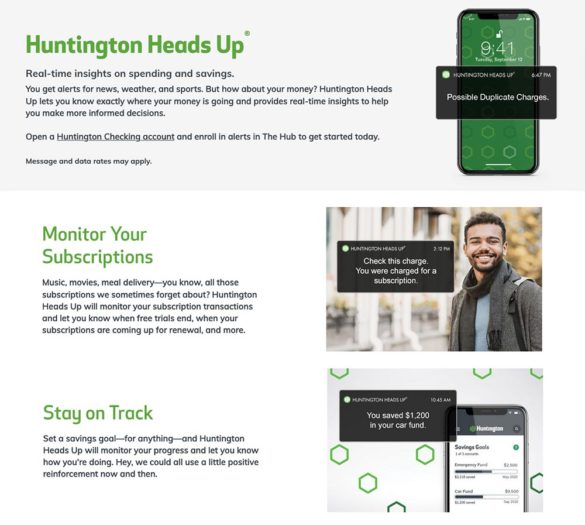

The Hub offers customers numerous tools, including spending analysis, spending goals, a calendar for tracking upcoming money flows, a savings goal-setter, and a feature called Heads Up. The latter is an artificial intelligence-powered application that provides real-time alerts and insights via text, push notifications or within the app or website. The alerts cover such things as duplicate charges, the achievement of a savings goal, or low-balance alerts based on a person’s normal spending pattern and scheduled payments.

Spend Analysis is the most popular feature, according to bank spokesperson Emily Smith. With it, customers can see details of historical spending, income, spend versus income, spending category and more.

The Hub is free and does not require any enrollment or even set up, except for specifying the type of notifications you want. However, various settings and categories can be tailored by the customer.

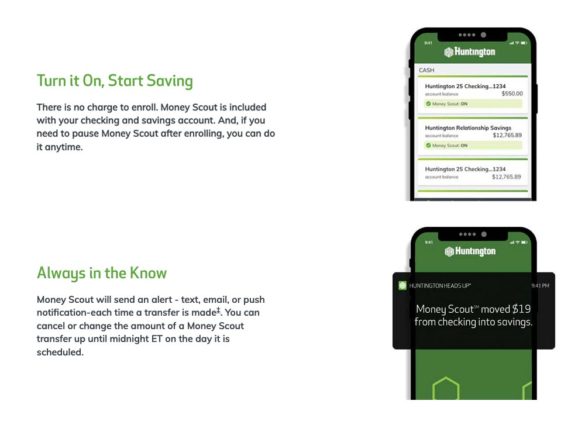

“Money Scout,” an automatic, AI-driven savings tool, was introduced into the bank’s digital lineup in August 2020. During a November webinar conducted by Personetics, the vendor the bank works with for Money Scout and other AI-driven tools, a bank executive said that since the launch, “close to 10,000 customers had signed-up and a few million had already been saved.” On average, Money Scout moves about $100 to savings per month per user, according to the bank.

A version of The Hub also exists for business users and another version has been created for private banking customers.

The money management functions that are part of The Hub are in addition to other digital banking capabilities such as mobile check deposit and bill pay. The capabilities in total resulted in Huntington’s mobile app being ranked highest among regional banks in J.D. Power’s Banking Mobile App Satisfaction study for 2019 and 2020.

Read More:

- AI’s Real Impact on Banking: The Critical Importance of Human Skills

- Digital Transformation Demands a Culture of Innovation

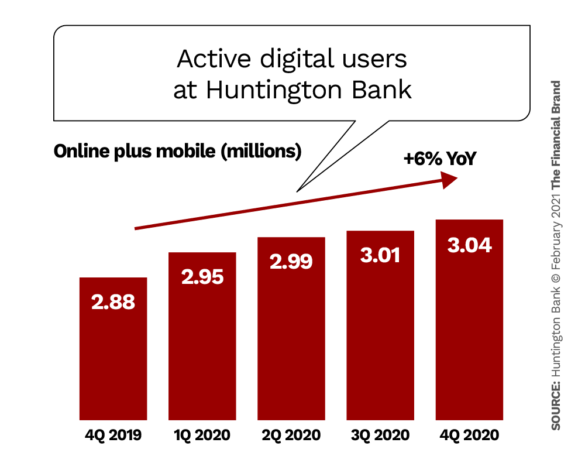

Digital Engagement Growing Steadily

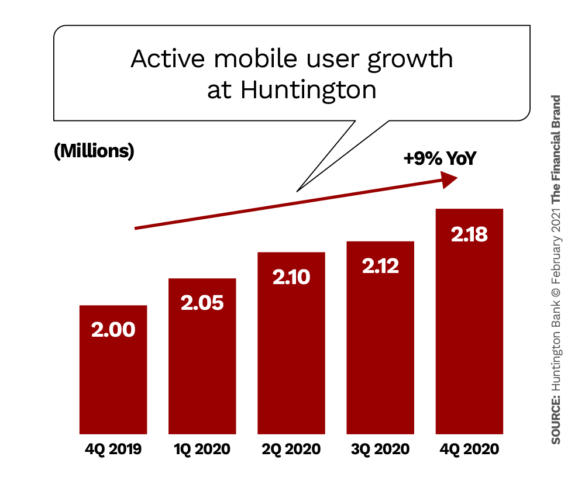

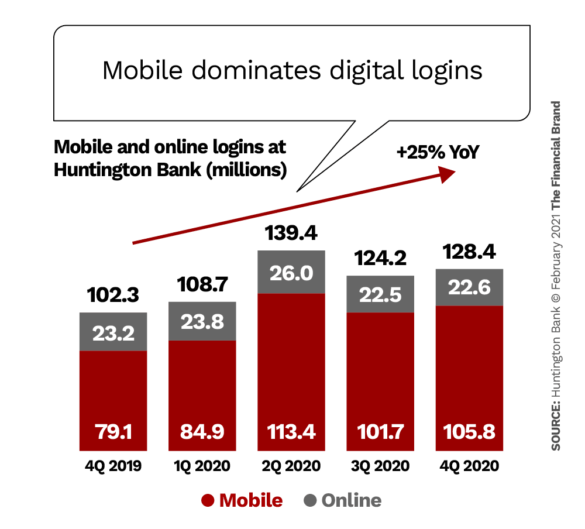

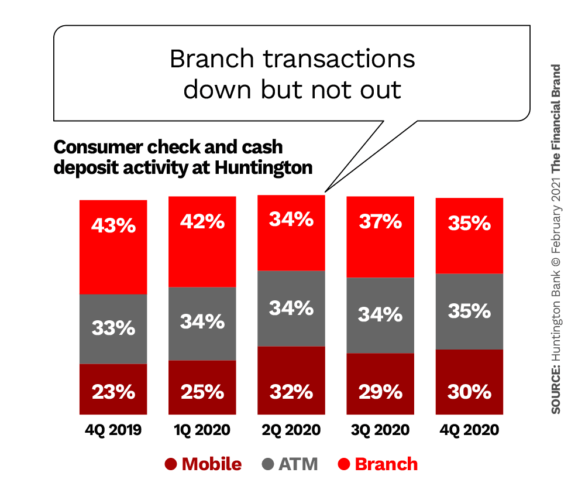

For an institution that’s been around for more than 150 years and still operates about 800 branches (not counting TCF’s), transforming to a digital-first institution doesn’t happen overnight. But Huntington considers its multi-year digital journey a competitive differentiator. While the bank doesn’t release many detailed metrics about its digital efforts, in its 2020 year-end earnings review, management highlighted several charts that depict growing digital participation.

Clearly mobile was the dominant means of digital engagement in 2020 for Huntington customers, not only in terms of the number of active users, but also in terms of activity.

Read More: 7 Essentials of Digital Banking Transformation Success

How a Regional Bank Competes with the Megabanks

Andy Harmening says he’s often asked how the Midwest regional can compete with the “trillionaire” banks. He says that in addition to the bank’s willingness to invest significantly in digital development, two factors stand out: listening to customers and collaboration.

The listening attribute runs through much of Huntington’s strategic vision. “Our philosophy is to listen to customers and then put out there what they want instead of what we want,” Harmening states. “We don’t need shiny objects, we need to serve the customer.”

The Hub, for example, came about after two years of research, which included having bank representatives meet with customers in their homes to see first-hand how they handled their finances, and the challenges they faced.

More recently members of the bank’s digital team sat and watched the use of a new account-opening process in branches (with customers’ permission) to gauge their reactions, according to Harmening. “We are proud of our work,” he adds, “but sometimes we have to step back and say, ‘It’s not how smart we are — what does the customer say?'”

Traditional financial institutions have long been hindered by operating in operational silos that stifle innovation. Harmening believes collaboration is the heart of being able to transform to an agile digital institution. He says the bank’s chief operating/chief technology officer is his key partner in this, but that collaboration among the marketing, product and data and analytics teams is essential to enable Huntington to keep up with the megabanks. “Having everyone on the same page is exactly how a regional bank can compete,” he says. Being more nimble gives them a leg up.

Key Insight:

On the question of “build versus partner,” Huntington strikes a balance. It has chosen to build its online, mobile and alert platforms in-house, while partnering to enhance the customer experience, origination and segmentation applications.

How a Regional Can Compete With Neobanks

Will the increased agility described in the preceding section be enough for Huntington to meet the growing challenge of Chime, SoFi, Varo Bank and other fast-growing neobank competitors? Or will the inherent trust of regulated traditional players be the regional bank’s trump card?

“Trust is one of the ways we compete with fintechs,” Harmening responds, “but, look, it’s also okay if we disrupt them and create a product that no one has. When you can marry strength and trust of a bank that is well-capitalized and makes good decisions with the ability to be nimble, that’s the future for a regional bank.”

His emphasis on product innovation stands out because it’s often said that banking products for the most part have become commodities, so that the only way institutions can differentiate is through customer experience. CX matters of course, Harmening acknowledges, and being frictionless with mobile features is table stakes, but equally important is building a product that meets an important customer need.

Don’t Forget:

It’s not always what you build that’s important, it’s how you get the customer engaged. Huntington has a Digital Coach in every branch. These digital “super users” assist colleagues and customers on all things digital.

Why a Digital Leader Still Believes in Branches

Huntington drew attention by announcing that it would close 198 branches as a result of its merger with TCF Financial. That figure is a little misleading, however, as many of those branches are in Michigan, where there was large overlap. Huntington has not changed its tune on branches.

“I love the digital space,” Harmening explains, “but I think we have to provide a great in-person experience in our communities as well.” He’s particularly excited about the new local market presence Huntington will pick up (or increase) in Minneapolis, Chicago and Colorado as a result of the merger.

Note This:

“The pandemic has changed digital usage,” says Andy Harmening, “but in our traditional branches we’re still at about 83% to 85% of pre-pandemic transaction volume, which is really interesting in a world where people are trying to limit exposure.”

“Branch transactions post pandemic will remain down a little bit,” the executive states, “but I don’t think it will be by 15% to 17%. Maybe 10%. But that’s still serious usage. There is still a desire of customers to talk to people, so we don’t we don’t think the branch goes away.”