Non-banks are capturing more and more of the banking value chain, providing services such as payments, checking and even savings accounts that could erode as much as one-third of traditional bank revenues by 2020 according to Accenture. These new entrants pose a threat to banks by raising service expectations and coming between banks and their customers.

According to a new report from Accenture, entitled “The Everyday Bank,” the response is not just about closing branches, improving online and mobile banking offerings or making current products and services “more digital.” Instead, banks need to move further into the daily lives of customers, providing assistance before, during and after the financial transaction.

Customer behaviors and expectations are quickly adjusting to a world where products and services are recommended based on past behaviors and where location-based offers are provided instantaneously on their mobile device. Customers want information to be fingertip-ready.

The Everyday Bank

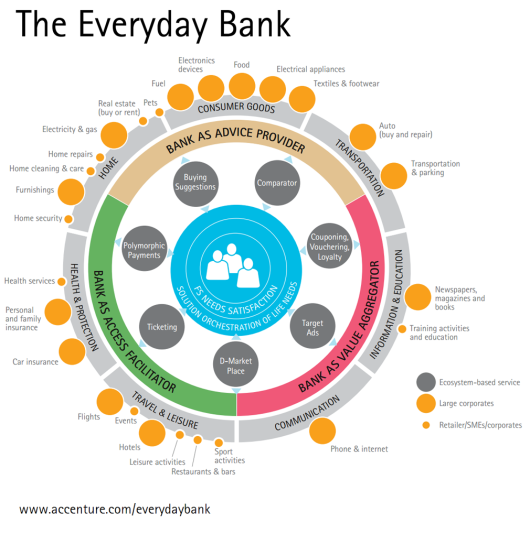

According to Accenture, an Everyday Bank leverages the vast amount of insight it possesses to become central to a customer’s financial and non-financial digital ecosystem. The Everyday Bank reinvents itself as a value aggregator, advice provider and access facilitator, acting proactively on the customer’s behalf, improving reputation and trust.

An Everyday Bank drives continuous daily interaction by building partnerships and connections with provider partners who offer goods and services in every area of area of consumption, including retail, home services, health and security, travel and leisure, communication and transportation. By tapping its wealth of transactional data, without ever sharing analytic information outside of its four walls, the bank reaches out to the right third-party providers and other key players to build a digital customer experience combining mobile, big data, analytics, digital marketing coupling, ticketing capabilities (at ATMs?) and more.

The Everyday Bank uses its digital engine to automate front- and back-office processes to optimize for speed, efficiency and scalability. According to Accenture, a highly functioning Everyday Bank can:

- Slash back-office effort by as much as 80 percent

- Reduce its managed applications portfolio by 70 percent

- Cut time to market by 40-50 percent

- Increase operating income by 25-30 percent

In a real-life example, an Everyday Bank has the rich customer data to know when a customer may want to purchase a car (based on the age of current vehicle, family structure, etc.). After offering the customer assistance if they agree that a car purchase is in order, the bank can recommend vehicle models that might fit their lifestyle, personal preferences and budget.

Next, because the bank is in a position to negotiate thousands of car deals on behalf of their customers, they can get a price that meets both the customer’s and dealers needs. After bundling in insurance and any other after-market products, the bank then recommends a payment plan that is best for the customer.

According to Accenture, the five critical elements of an Everyday Bank include:

- Provides services that are digitally optimized across a variety of platforms

- An omnichannel approach

- Uses big data and predictive analytics to help anticipate customer financial and non-financial needs

- Offers a human touch for high value interactions

- Is attuned to their customers’ moments of truth

The Everyday Bank also brings pricing transparency, trusted advice, social recommendations and transactions – as easy as one click.

Benefits of Becoming an Everyday Bank

For banks that build the capabilities of an Everyday Bank, the rewards are significant. According to Accenture, banks that exploit their rich customer purchasing data and secure data management capabilities can increase customer interactions by 250 percent.

“An Everyday Bank leverages the vast amount of insight it possesses to become central to a customer’s financial and non-financial digital ecosystem.”

— Accenture

Most importantly, the bank’s customers enjoy the benefits of a financial partner who can anticipate their needs, looks out for them and rewards them for their loyalty by recommending ideal providers. They enjoy an improved experience that saves them time and money with a much more personalized relationship. Merchants and service providers also benefit from the bank’s customer insights through improved targeting driven by the bank and increased sales volumes.

By acting as a digital value aggregator, the bank is rewarded with deeper relationships, increased loyalty and improved profitability due to a higher volume of lower-cost transactions and additional service fees.

It is important for banks to act quickly to become the indispensable Everyday Bank, moving customers from doing occasional interactions to being embedded into their digital lives with daily interactions. Banks need to develop the digital partnerships with merchants, suppliers, small and medium size businesses, telcos and other digital companies to deliver new products and enhanced service for the customer.

By collaborating with these partners as opposed to competing, the bank can be repositioned at the center of the customer’s everyday life, becoming integral to both financial and non-financial needs. The Everyday Bank has the opportunity to acquire all segments of customers at an efficient cost (including underbanked, unbanked or unhappily-banked populations), using the number of interactions with these customers to offset the lower income per transaction.

Everyday Banking in Action

Below are examples provided by Accenture where banks have leveraged their customer insight and extended beyond traditional banking services to provide value to customers.

The Commonwealth Bank of Australia

Using augmented reality in a mobile application, The Commonwealth Bank of Australia helps its customers looking to buy a new house. The mobile app provides details on 95 percent of the residential properties available for sale throughout the country.

Included is data related to recent sales and prices, information about the neighborhood, and the location of each property in relation to where the customer is at any time. Integrating financial services into the application, the bank offers details about mortgage loans and insurance that can be purchased through the bank’s website.

BBVA

BBVA of Spain supports its customers when they purchase a new car by equipping the customer with information on both the list price and selling price of the car. The app also offers loan and insurance information. The bank’s goal is to ensure that its customers can negotiate the best deal.

To become an Everyday Bank, BBVA could expand this partnership with the customer by anticipating when the customer may be in the market for a car. This could be achieved by using outside insight into the age of the car owned by the customer and recent purchase cadence (the customer has shown a history of purchases every 3 years), upcoming auto loan final payments, or change in household structure (marriage, birth).

The bank could also build relationships with several dealers, allowing itself to negotiate prices on behalf of the customer and even provide offers related to after sale service, etc.

The Everyday Bank Challenge

To be a profitable industry, banks cannot simply rely on providing accounts and access to funds. Competitors are eating away at significant parts of the banking value chain with the potential of limiting banks to becoming nothing more than utilities.

The future of the industry will depend on its ability to leverage the power of customer insight and digital technology to provide services that help today’s tech-savvy customers save and better manage their everyday lives. If banks don’t move quickly, however, competitors will insert themselves into the buying process, gaining the valuable purchase insight that is the domain of the banking industry today.