The Gallup organization researched how customers prefer to interact with their bank for 14 of their most common needs. They also evaluated the difference between channel preference and actual channel use and the impact on satisfaction and engagement when a customer uses a channel they didn’t prefer.

While this is some of the most detailed research on channel preference and use, Gallup only evaluated single channel preferences as opposed to researching how a customer may use multiple channels for some transactions (researching providers or services, opening an account, managing an account, receiving account information, etc.). Despite this weakness, the research is still helpful in determining how to best migrate customers to an optimal channel mix.

Financial Impact of Channel Use

Recent regulations that have impacted the ability for banks to generate fee income from retail customers has required banks to rethink their business models and even the customers they serve. In addition, banks and credit unions have had to reconsider the optimal mix of channels their customers use to interact with the institution and to transact their business due to the costs associated with different channels.

According to a 2010 TowerGroup study, the costs of handling a customer transaction varies widely by channel, from as much as $3.75 for a call agent interaction and $1.34 for a branch transaction down to as low as $.60 for an ATM transaction and $.14 for a mobile transaction. Based on just these numbers, it would seem prudent to move as many customers as possible to automated or digital channels and away from branches and call centers. Unfortunately, it’s not that easy.

Banks and credit unions have found that as they introduce new channels, the typical customer’s overall number of interactions also increases (there is not a direct offset of more expensive channels as a customer uses online or mobile channels). In addition, lost in a purely cost-based analysis is the more important questions regarding how a customer feels about using various channels to transact business.

Customer satisfaction with different channels influences that customer’s future banking behavior, which in turn affects key factors such as additional cross-sell, increased profitability, and reduced cost to service. The Gallup research explores how customer preferences for the banking channels they use affect key performance indicators such as satisfaction with that channel and engagement with the bank itself.

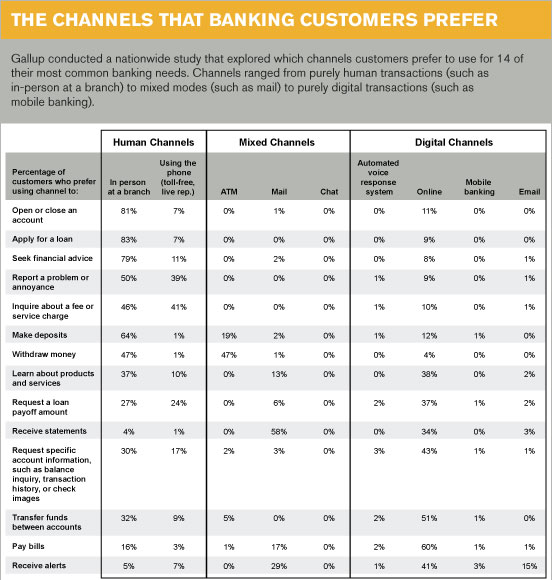

Customer Channel Preference

Every customer has a channel (or channels) they prefer as they interact with their bank or credit union for various needs. Some may prefer a branch, while others prefer an ATM, online or mobile channel. The Gallup research explored which channels a customer prefers to use for 14 of the most common banking needs across a variety of channels. Primary findings of the study included:

- To open or close an account, apply for a loan, or seek financial advice, about three out of four customers prefer interacting in person at a branch.

- To report a problem or inquire about a fee or service charge, customers prefer using a branch or interacting with a live call center representative.

- To make deposits, customers prefer using a branch. Customers who want to withdraw money prefer using a branch or an ATM.

- To learn about new products and services or request a loan payoff amount, the most preferred channels are: going online, using a branch, or speaking to a live call center representative.

- To request specific account information or transfer funds between accounts, most customers prefer going online, although a number of customers also prefer using a branch.

- Not surprisingly, to receive statements and pay bills, mail and online are the preferred channels. More customers prefer to receive statements by mail, while customers prefer the online channel to pay bills.

- To receive alerts, customers prefer using multiple channels, including online, mail, and email.

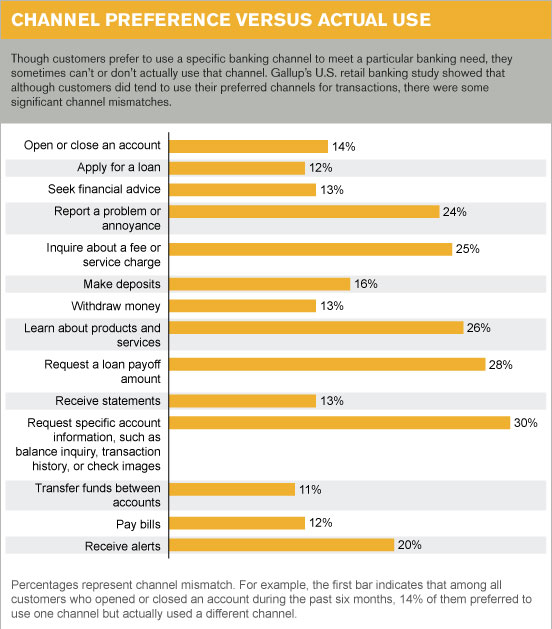

Customer Channel Use

As can be expected, customers don’t always use their first choice of channel when transacting business. While customers tended to use the channel they preferred, they actually use another channel due to convenience, cost, etc. Gallup found that there were some significant ‘channel mismatches’ for interactions such as balance inquiries (30%) and other specific inquiries (loan payoff, service fees and even learning about a product), while there was far less variance between preference and actual use for more involved transactions such as transferring funds, paying bills, opening an account or applying for a loan.

Impact of Channel Preference Mismatch

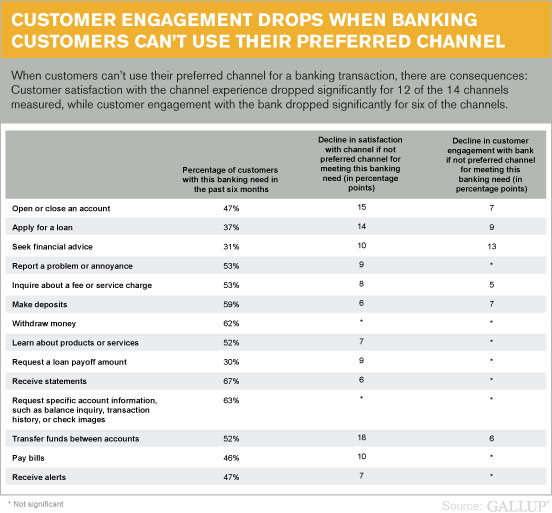

The Gallup research found that when a customer is not able to use the channel they prefer for a banking transaction, both satisfaction and levels of engagement drop. These reductions in both satisfaction and engagement differed across the 14 banking interactions reviewed, with significant declines in satisfaction for more than half of the banking activities and moderate reductions in engagement in more than a third of the activities.

The drops in both satisfaction and engagement appeared to be directly correlated to activities that are traditionally 1:1 interactions (account opening and closing, advice seeking, applying for a loan) and where the risk was perceived to be greatest (transferring funds, paying bills, making deposits). These reductions in satisfaction and engagement also may be caused by banks and credit unions not building strong customer-facing applications in some of these areas (account opening, funds transfer, paying bills) that help the customer feel comfortable with online and/or mobile channels.

While this is one of the better studies regarding channel preference, a flaw is that customers are becoming increasingly comfortable with using multiple channels for many interactions such as account opening, funds transfer, product education, etc. In addition, as Gallup points out, the impact of lower satisfaction or engagement needs to be analyzed on a more finite level based on different segments of the customer base. For instance, what is the impact of potential loss of accounts and related revenue and profitability if satisfaction and engagement are reduced in key customer segments?

Encouraging Channel Migration

Despite potential drops in satisfaction and engagement, it is still important for banks and credit unions to find ways to migrate customers from more expensive channels to less expensive online and mobile banking. Thus is especially true with customers who are less profitable to the bank.

While there are many strategies that can be used to encourage a customer to use digital channels, it is important to first determine the optimal channels that will meet both the bank’s and customer’s needs and the consequences (by customer segment) of channel mismatches.

Not surprisingly, customer’s preferences of channels are almost always more complex and expensive than the channel(s) the bank would prefer the customer to use. This is why the closing of branches generates such a highly charged dialogue both within the industry and with customers. While a customer may not use a branch, they always want to know one is easily accessible.

Channel migration strategies are further impacted by the fact that customers are very unique in their channel use. For instance, Gallup found that in a randomly selected sample of 3,000 retail banking customers, customers used more than 750 unique combinations of channels to accomplish their banking needs.

It was also found that is is much more difficult to migrate a customer from their current channel habits than to build an optimal channel use strategy at the start of a relationship (or to use a best-in-class channel strategy to acquire customers who use the channels desired by the bank.

Gallup found three overarching strategies for banks wanting to migrate customers to online and mobile channels:

1. Offer positive — or negative — incentives. Examples of using incentives for online and/or mobile use is the waiver of fees or even the paying of small incentives for performing specific transactions through lower cost channels. According to the Gallup research, more than 70% of customers would be willing to switch to digital channels if offered fee-based incentives, while incentives that enhance functionality were less effective.

Disincentives include the use of fees for paper statements. Banks need to be careful, however with fees since there is a hypersensitivity to any fees that may be applied to interactions that have traditionally been free. The Gallup analysis showed that half of all customers will look for another bank if fees are imposed (for example, if the bank increases interest rates on current loans by 0.25%).

2. Set positive defaults. Another approach banks can use is to position the new online and digital channels as the ‘standard’. By doing so, customers would need to “opt out” of a channel strategy. This is advantageous compared to having the customer ‘opt-in’ to a channel.

To make it easier for platform personnel or to reduce abandoned online account opening ‘shopping carts’, banks and credit unions could reinforce not opting out by providing incentives or rewards for customers who agree to use the bank’s desired channel. According to Gallup, the key is to allow customers to select their own optimal channel use plan and pay appropriately for it.

3. Provide interactive education. In addition to using incentives or positive defaults to change customer behavior, banks can provide customers with interactive technology education within the branch and online to encourage channel migration. This could be accomplished through interactive kiosks in the branch or by building tablet learning tools or short instruction videos to acclimate customers to new channels.

Potential Unintended Consequences

While moving customers to less expensive channels is imperative due to the high operational and regulatory costs in banking, there can be unintended consequences to an increased reliance on digital channels according to Gallup.

One of the impacts of moving less emotional and involved transactions out of the branch is that customers will rely more on branches for involved advisory and problem solving transactions. In addition, transaction levels will continue to plummet, eliminating the need for traditional tellers. Most bank and credit union branches are not adequately configured for these changes either from a personnel or physical perspective. Without the reduction in personnel and real estate costs, moving customers to alternative channels could actually increase costs.

Another unintended consequence is that as more customers move to self-service channels, the ability to interact, provide advice and sell will be reduced. In addition, the ability to move relationships to another institution is made easier in an online/mobile world.

Your Strategy Going Forward

Moving customers to less expensive channels is required based on the economics of today’s banking industry. But migrating customers who are already set in their ways comes with both satisfaction and engagement risks which could result in attrition, reduced balances, lower profitability and the unintended consequences of digital as opposed to human interaction.

As channel migration strategies are developed, it will be important to segment a bank’s and credit union’s customer base based on profitability and current channel use to develop an optimum channel strategy. Understanding the impact of potential channel migration strategies will be important and the use of multichannel communication and training will be key to acceptance.