When almost everyone is facing some sort of a challenge during the coronavirus pandemic — personally, professionally, or both — only those financial institutions that are able to react quickly and adapt to the specific needs of their customers will be rewarded with long term loyalty and trust. Those institutions incapable of adapting will most probably face very harsh times.

Customers in crisis are not ready to forgive shortcomings and wait peacefully for them to be eliminated. People are vulnerable now, they are nervous, they need a solution right away, and the solution must be perfect. That’s why 100% remote financial products that solve customer problems in the right way are more in demand than ever.

Every financial institution was well aware of the need to digitize long before COVID-19 appeared. Some managed to do it fully, some did it partially, and some put it off, telling themselves that there is still time left. Waiting is no longer an option.

How can banks and credit unions improve the customer experience in the right way, and so prepare themselves to face the aftermath of the pandemic?

It can’t be done overnight. But with a carefully considered plan, improvements can have a more lasting impact than if decisions are hastily made. In the rest of this article we present the three factors that determine the quality of digital performance and show how to purposefully create an advantage in this difficult time to turn the crisis into growth.

The three factors are:

- How well the customer’s context is taken into account.

- How well your institution’s culture meets the modern requirements.

- How effective your business strategy is in terms of the COVID-19 situation.

1. Customer Context: Find How to Exceed Users’ Expectations

Financial institutions are trying to find ways to cope with COVID-19 and provide the best service to their customers. Unfortunately, these efforts can become meaningless if they haven’t dived deep into exploring the user context, motives and actions — three elements that are crucial for truly satisfying consumers and solving the problems they are facing.

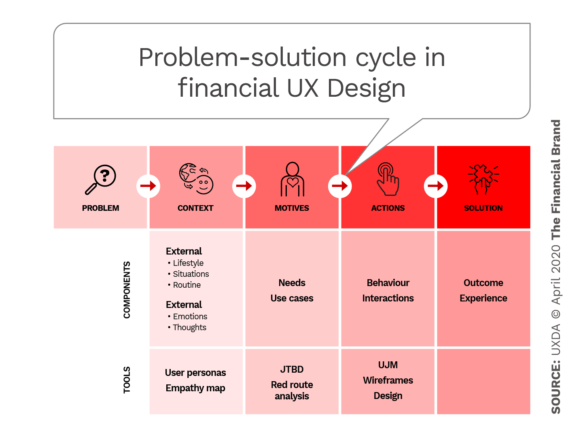

To better understand these three conditions, we need to explore the problem-solution cycle from the human perspective. It starts with the context, which defines the motives that then lead to actions. At each point, you can use specific tools that reveal the process and give you an idea of exactly how a financial service should work in order to solve a specific customer problem.

Context. First of all, a person who is facing a problem has a context — two of them. First, there is external context: for example, the situation in which the problem arose, the routine in which a person operates and the lifestyle of the person in general.

The different threats and restrictions that have come with COVID-19 have led to significant shifts in the customer lifestyles and daily routines. For example: People working from home or those who have lost their jobs or who’s once-successful businesses have stopped producing income. This has a direct impact on their short and long-term situation. Also, social distancing restrictions complicate coming to banking branches to get a personal consultation, advice or get paperwork done.

There is also an internal context such as emotions, thoughts and hopes. The pandemic creates countless questions and worries, many of them regarding money and finance. All of this creates a wide range of mostly negative emotions that have a direct impact on human behavior and actions.

To identify the external context, you have to collect information about the potential users of your digital financial service. Then create a user profile that describes the lifestyle and habits of the user persona.

After that, you should create an empathy map to uncover the deepest understanding of the internal context. This uncovers the limitations and/or opportunities associated with the product use context. If you do not get to know your user’s habits, lifestyle, environment, emotions and cognitions, you cannot understand how your product can help solve their daily tasks and problems.

The banks and credit unions that do their homework and find out how their customers feel and what kind of financial help they need will be the ones who will maintain their customer base and even attract new clients.

Motive. The context determines a person’s expectations in searching for a solution to a problem. How consumers perceive the problem, where they will look for the solution, and how they will evaluate the effectiveness and quality of it defines the motive for using your banking product or service.

In the case of COVID-19, there could be plenty of motives that the customers apply to financial products. For example: get a credit card without leaving their home; deposit some cash into an account for online purchases.

Tools such as a Jobs To Be Done framework (JTBD) and Red Route Analysis can help at this stage.

Actions. When the consumer uses the product, your task is to ensure that the product provides the user with a clear, enjoyable and effective solution to their initial problem.

This is where a User Journey Map (UJM), user flow map, wireframes (visual representations of a user interface), user interface design and testing come in as user experience (UX) design tools.

None of the above will be possible if your institution’s culture is product/profit focused and not customer-focused. Let’s find out if your culture is ready for the challenge of COVID-19, and what can be done if it’s not.

Read More: The State of Digital Banking Transformation

2. Culture Adjustment: Become a Disruptor to Win the Crisis

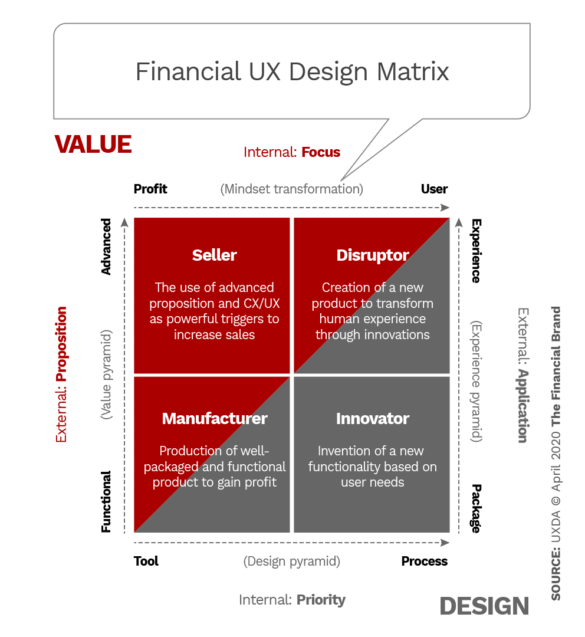

Many financial institutions are not adapted for a new and fast digital world that looks to last well after the COVID-19 crisis is over. In the digital world, companies that are disruptors have the greatest potential. The secret of their success is to base all of their operations on two basic components: value and design.

Both of these elements significantly affect the formation of customer experience within any business. Let’s take a look at how the use or the lack of the use of design and value distinguishes four different company types.

If you spot your financial institution as one of them, we present practical steps you can take right away to get closer to becoming a digital disruptor mastering this crisis with confidence.

Here’s are some brief comments for each of the four categories:

Manufacturer. This is an institution that is focused more on “production process” than on its customers. The management of this type of institutions is convinced that basic functionality is enough for users. Design, in this case, is just a tool to create packaging — to bring the product to the market in an attractive way.

“Manufacturer” is an outdated category for financial institutions. Facing the COVID-19 crisis is extremely difficult for such a company.

Steps for transformation:

- Switch the mindset from profit-oriented to user-oriented.

- Review the role of design in order to turn it into a customer-centered growth factor that improves product quality.

- Reinvent products and services according to an advanced value proposition.

Seller. Unlike “manufacturers,” banks and credit unions that are “sellers” are more focused on promotion than on production functionality. Sellers are well aware that it is necessary to use something more attractive to users than boring and standardized functionality. Therefore, they use an advanced value proposition and user interaction design as powerful promotional triggers.

The problem is that, instead of sincerely understanding how to help customers and how to improve their experience, sellers perceive a customer-centered approach as a magical way to increase profits. So, in a crisis they cut service expenses to keep profit, thus ruining customer loyalty and relations.

Steps for transformation:

- Change the culture of the organization and goal setting, making customers a top priority.

- Make the customer-centered design approach the number one priority by integrating it at all levels, starting with business processes.

- Hire and provide authority to UX specialists for digital products.

- Rethink performance indicators and bring to the forefront such metrics as customer feedback, ratings, reviews and comments on social media.

Innovator. Innovators in our matrix use design thinking as a creative process aimed at finding new solutions. Innovators are sure that the functionality of a new level provides high value for consumers. Therefore, they are much more interested in researching and developing a new technology than caring about the customer experience.

Steps for transformation:

- Get rid of the idea that functionality is enough.

- Adapt a deep understanding that the main value for consumers is the experience.

- Take the extra step to orient the new technology to create a better experience for consumers.

Disruptor. These are companies or institutions that leverage the maximum potential of all four vectors of the UX Design Matrix and are extremely customer-oriented. Very often, they reinvent experience, offering something new that is much more convenient, efficient and enjoyable than the standard alternatives.

Disruptors often use the functionality that innovators have created but develop it at the higher levels of the value proposition. Disruptors see profit as the result of maximum user satisfaction, which provides them with long-term competitive advantages, customer loyalty and community support, all of which are vitally important in a crisis such as COVID-19.

Read More: Digital Transformation Will Flop if You Don’t Also Transform Staff

3. Business Strategy: Use the Appropriate Formula for the Digital-Only Covid-19 World

Global digitalization and the current situation with COVID-19 have completely changed the rules of the game in the banking industry. When the main goal was to make a profit, it was enough to have products, a business model and market distribution to ensure the institution’s success. It doesn’t work that way any more.

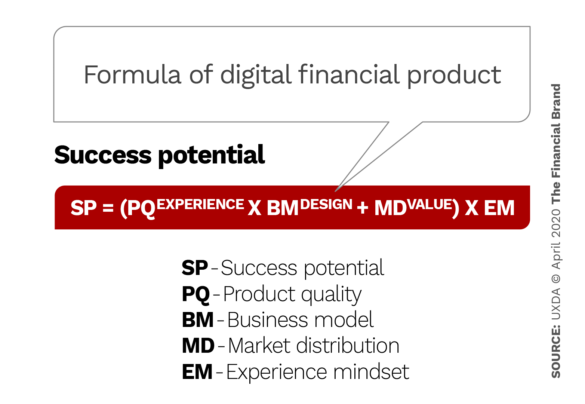

What differentiates successful digital products from failures is the experience, benefit and value that the product provides. The Digital Product Success Formula that we created at UXDA is based on the traditional operational model but adds some very important elements to the general business strategy.

When it comes to the digital age or especially to survival in the tense circumstances of the pandemic, business success potential is defined by the formula shown below.

If you want to evaluate your institution’s potential, estimate each component by a value from zero to five, taking, as a basis, the relevant characteristics of leaders and outsiders in the industry.

Overall, success potential is the ability of bank or credit union to efficiently produce and deliver to the market a product or service that will be in such high demand that it will ultimately generate a positive financial flow in the long term. Success potential depends on several factors:

Product Quality raised to the power of Experience. To increase the success rate of a product or service in the digital age, you must purposefully create a delightful customer experience.

Action plan. To create a great experience, take into account the user’s needs, wants, expectations, pains and motives for using the financial product and explore these within the Problem-Solution cycle described earlier.

Business Model raised to the next level with the power of Design. We are not talking about the visual aspect of design here, but about a generalized design approach to create and develop a human-centered business across all operational aspects and in the overall business culture. This approach allows adaptation to modern market realities.

Working with banks, I see institutions with precise functioning rules. But as the situation with COVID-19 clearly demonstrates, competitiveness in the digital age requires extra flexibility and ability to adapt quickly. Switching focus from bureaucratic legacy to flexible customer-centered company development is critical.

Action plan. To increase the focus on customer satisfaction and ensure the ability to walk out of the pandemic situation as winners, financial institutions should integrate design thinking at all levels of their business with the aim of searching and executing more disruptive and effective ideas.

Market Distribution powered by Value. The market distribution term includes both the chosen market niche with a positioning strategy and the activity of promoting and delivering information about a product or service to customers or potential partners of the company.

For the market distribution, the success multiplier is the value provided to the customers. In a crisis, people don’t buy stuff they don’t need, just because it was nicely advertised. Today, more than ever, it’s about value and the ability of the financial institution to help people.

That’s why we add, but don’t multiply, market distribution rate to the formula. Even with zero distribution efforts, business success still can be achieved by word of mouth, for example.

Action plan. It’s possible to create value if a financial product also provides pleasing usability and aesthetics that cause positive emotions as well as the feeling of being a part of a bigger mission that has an impact on the world. This may become a powerful community builder for every socially responsible business. Facebook, for example, asks people to mark their COVID-19 status to detect infection pathways.

The Experience Mindset. Thinking is a filter through which we perceive the world around us and the basis for which we set goals and make decisions. Instead of an outdated mindset focused only on sales, banks and credit unions should implement a mindset focused on finding all possible ways to help their customers. This is the only way to survive in the age of digital disruption and in the difficult times that the COVID-19 outbreak has put us in.

Action plan. A sharp focus on consumers’ expectations and behavior is critical. Don’t try to manipulate their needs, perceptions and experiences. Use empathy to become really useful to your customers, and they will provide an unexpected power for the growth of your business even in a situation of a crisis.

Building a Better UX and Tackling the Crisis 100% Remotely

Even though the situation we are facing reminds us of a state of the war, the technological advancements of today can give us superpowers. This doesn’t only apply to maintaining some processes remotely through digital channels. It also includes the possibility to execute a thorough transformation that could save your financial institution from irrelevance after the COVID-19 crisis.

If you look closely at the frame of the four business cultures in the matrix, you will find that the four coordinates — Focus, Proposition, Priority and Application correspond to the four extra elements of the formula, respectively Mindset, Value, Design and Experience. So, using the formula to enhance your business strategy will help to transform your culture into a disruptor and win the crisis. A financial institution that is fully digitalized gains an instant market advantage over competitors who lag behind.

This is the time to build relationships with your retail and business customers that will last. If financial institutions integrate customer-centricity deep into their DNA, they will be able to stand strong, despite any circumstances. If the main goal is still to make profit, not to help people, it’s nearly impossible to survive with such an attitude in the situation of a crisis.

But if customers understand that their financial institution has their back, cares about them and is actively looking for more and more ways to help them, that company will receive trust, loyalty and respect from these customers.