Just because more consumers than ever have moved to digital banking options doesn’t mean that they no longer want their financial institution to know them, look out for them, and reward them on an individual basis. In fact, in an increasingly digital world, the ability to connect on a human level may be more important than ever. For those financial institutions that can find the right mix of digital and humanity, the reward will be an increasing level of trust and relationship growth driven by personal connections.

As consumers move out of branches and increasingly use their computer or phone to shop for financial services, open accounts and conduct daily transactions, many banks and credit unions believe they will lose the ability to get to know their customers and differentiate their institution based on engagement and service. Nothing could be further from the truth. In fact, for those organizations that focus on combining human and digital engagement, the rewards can exceed what would be possible from a single channel alone.

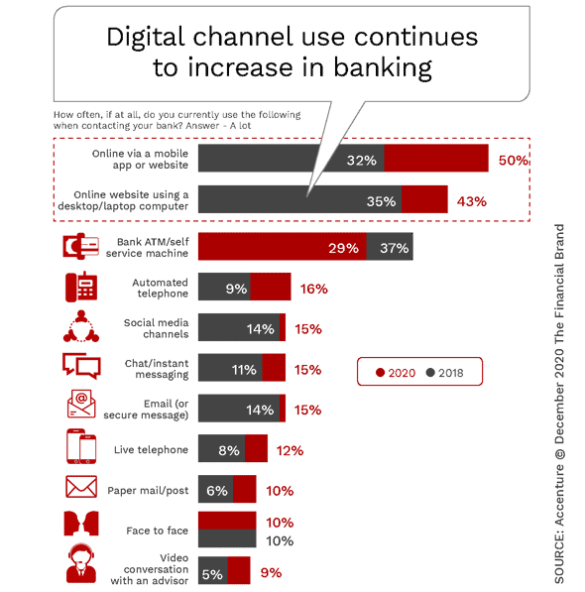

As outlined in the chart below, from an Accenture study, the use of online and mobile channels skyrocketed as a result of COVID-19. In addition, the use of ATMs, call centers, instant messaging, email and even traditional mail increased while in-person engagement remained rather anemic. The onset of the pandemic also increased the use of contactless payments as opposed to cash. It is expected that the movement from physical banking options will not ever return to pre-pandemic levels.

From both an efficiency and effectiveness perspective, financial institutions must aggressively embrace the ability to provide the best digital experiences by reducing friction and improving the user experience. At the same time, banks and credit unions must use data, advanced analytics and modern technology to deliver products and services with the highest level of personalization and contextuality in much the same way that the best concierge delivers unique experiences for hotel guests by understanding needs.

Read More:

- Now is the Time for Intelligent Digital Banking Experiences

- 7 Essentials of Digital Transformation Success

- Digital Transformation Requires More Than Technology Upgrades

The Pros and Cons of Digitalization

There is little argument that the use of digital channels is beneficial to financial institutions from an economic perspective. While online and mobile banking have increased the number of transactions and engagements compared to what was previously done in branches, the cost of any digital transaction is far lower than a human engagement. From making a deposit, to transferring funds or opening a new account, banks and credit unions can reduce the cost of serving a consumer by providing a strong digital alternative.

But providing a digital alternative is not enough. Digital interactions must be fast, easy and have a level of personalization and humanity that more than matches what was available in physical locations. Without a strong user experience, and one-to-one understanding of the needs and best next action for the consumer, trust can be lost and financial institutions will be viewed more as a utility than a trusted advisor. The commoditization of banking should be one of a banker’s worst nightmares, where loyalty is minimized.

Read More:

- Digital Banking CX Boils Down to One Word: Speed

- Financial Institutions Benefit from AI, But Consumers Remain Skeptical

Trust in Banking is at Risk

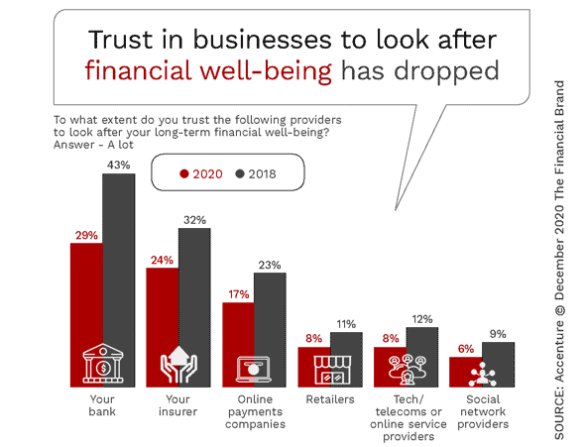

While the majority of consumers believe their financial institution responded adequately to the challenges of the pandemic, the ongoing trend of diminishing trust in banking has continued. In fact, only 29% of consumers said they trusted their financial institution to look after their financial well-being, compared with 43% two years ago. This is the largest drop of any industry category, while the overall level of trust remains higher than payment companies, tech firms, retailers and social networks.

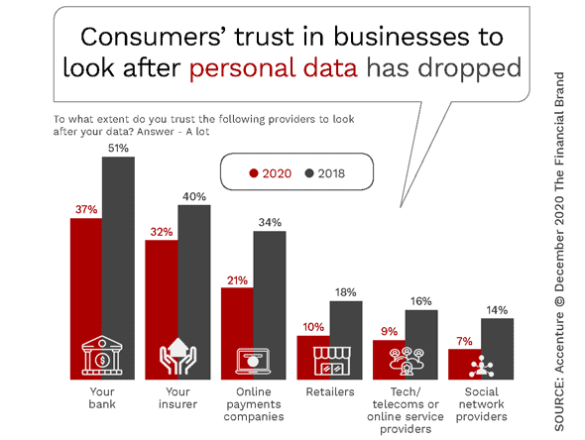

The level of trust in banking to keep personal data secure also has diminished substantially over the past two years, from 51% in 2018 to 37% this year. This lack of trust by consumers of financial institutions could negatively impact the ability for banks and credit unions to undertake digital initiatives that would use personal data for improved experiences and advisory benefits.

In fact, only 53% of consumers are willing to share more personal information with their bank in return for added benefits and a more personalized, relevant service, according to Accenture. This is a slight drop from two years ago.

Building Trust Through Personalization and Humanization

Banks and credit unions can’t deliver a smiling face or dog biscuit across digital channels. That doesn’t mean that digital consumer journeys need to lack personality, an understanding of the customer’s needs, or a positive brand experience. In fact, digital engagement can more than replicate the personalization that consumers crave and the human connection consumers need.

Despite many surveys that give the impression that consumers want to visit a branch to open a new checking or savings account or apply for a loan in person, this physical interaction has been driven more by habit and necessity than by a desire to sit down and complete lengthy forms.

According to Accenture, consumers have equal preference (47%) for using online channels (desktops and laptops) to open accounts as they do going to a branch, with mobile channels ranking third (37%). It is believed there would be an even more significant shift to digital banking if these options were faster and easier to use.

While consumers still shop for financial services based on price, more and more consumers really desire a strong value proposition for their relationship. As economic uncertainty decreases in a post-pandemic world, the importance of value delivered by banks and credit unions will increase even more.

The ability to use personalization and humanized engagements to demonstrate a commitment to a consumers’ long-term financial well-being will become a requirement in the future. Instead of a set of products that can be replicated by any financial institution, consumers want personalized solutions and advice based on real-time changes in their financial life. This can range from automated savings programs, to always-on credit availability, to one-to-one advice serving as a ‘financial concierge’.

For the most part, financial institutions continue to fall short of consumer expectations by failing to demonstrate an understanding of financial needs on an individual basis, and by pushing products over solutions. Trust is built when organizations offer tailored solutions based on an understanding of a consumer’s unique challenges and goals. This equates to showing empathy … a humanized trait that can be demonstrated over digital channels.

In a world changed by the pandemic, consumers no longer will accept a rear-view mirror perspective of what has already occurred with accounts. Instead, consumers will require their financial institution to provide a GPS perspective of what they should do to prepare for, and respond to, financial opportunities and challenges. Consumers will also require this level of understanding and delivery of advice across all channels as connected experiences.

The Risk of Poor Digital Experiences

Financial institutions must rebuild trust by genuinely looking after the long-term financial well-being of consumers and small businesses, and by delivering tangible value in return for the sharing of data. Instead of using customer insights for great internal reports, financial institutions must convert this data into action that is felt by the customer.

Deterioration of the customer relationship is the risk of not providing personalized recommendations and advice at a time and through a channel that is desired by the customer. In a digital world, this deterioration may not be reflected in the complete closing of an account, but by the utilization of alternative financial options provided by more customer-centric organizations.

Initially, the challenger bank, neobank, fintech firm or big tech competitor may have a secondary position as it relates to the financial portfolio of the consumer or small business. But over time, as the competitor generates more trust by providing exceptional digital experiences, the role of the traditional bank may start to become more of a utility than a trusted relationship.

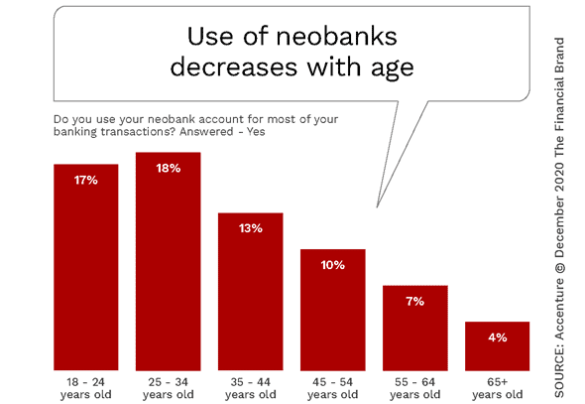

Accenture found that, while many challenger bank relationships remain secondary in nature, more and more consumers are using a digital bank as their primary financial institution. This is especially true with younger demographic groups, but is increasingly occurring with older consumers who have become aware of digital alternatives during the pandemic.

In the future, a great experience will not be defined by a financial institution’s price or the services offered, but by how well an organization helps customers and small businesses achieve the financial outcome desired. This requires translating data, analytics and advanced technology into action, product and service innovation, a commitment to an easy and seamless user experience, and an embedded platform that expands beyond traditional financial services.

More than being the responsibility of the chief marketing officer or the head of customer experience, becoming a customer-obsessed financial institution will become everyone’s job in the organization.