The financial services industry has been working hard to deliver a better experience on digital channels. Building on an early foundation that focused more on cost savings than customer experiences, most banking institutions now realize they must improve delivery of financial services on digital channels to keep pace with tech organizations like Google, Amazon, Facebook and Apple (GAFA).

PwC’s 2017 Digital Banking Consumer Survey provides insights into the rapidly changing behavior of the digital banking customer. The most significant finding was the rise of a very specific group that PwC referred to as “omni-digital.” This segment uses only digital channels such as mobile phones, PCs and tablets to conduct their banking, avoiding traditional physical channels and call centers altogether.

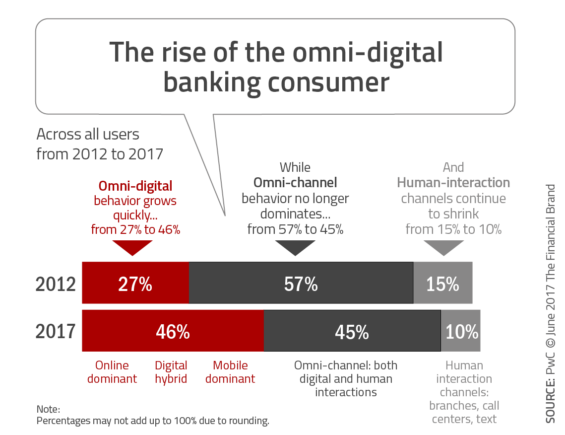

The research found that 46% of consumers use only digital channels today. This is an amazing increase from the 27% share that was seen only four years ago. Other highlights from the research include:

- Millennials bank by phone, period – 82% of 18 to 24-year-old smartphone owners say they use mobile banking. This should be a wake-up call to organizations who are building branches ‘to reach Millennials”.

- Smartphone banking has gone mainstream – 60% of smartphone users report using mobile banking in some way, up from 36% four years ago.

- The branch is not dead – 62% of survey respondents felt it was important for their bank to have local branches. In the future, however, “branches” could refer to sophisticated ATMs or a small office providing virtual capabilities since the frequency of visits have dropped from “a few times a month” to “a few times a year.”

Read More: Banks May Still Need Larger Branch Networks to Find Sales Success

The Rise of the ‘Omni-Digital’ Segment

For the past several years, the financial services industry has talked a great deal about the “omni-channel” segment. These customers use a variety of channels (both digital and physical), with the goal of most financial organizations being to provide similar experiences across channels, and to allow for travel between channels to be seamless.

PwC found that this segment of omni-channel customers has been significantly shrinking over the past four years, being replaced by the “omni-digital” customer who only uses digital channels. The size of this segment is massive (46%), with implications for branching strategies, investment prioritization, staffing models, etc.

If the access to banking will be through phones, computers and tablets for the majority of customers, how does this shift impact product development, product sales, customer service, design of mobile banking applications, etc. Should branches be closed, moved or resized? If an organization has differentiated itself on personal customer service, how does this translate to a digital platform?

Digging deeper into the digital channel usage, in 2012, only 1% of consumers were ‘mobile dominant’, interacting with their banks primarily by a mobile device. In 2017, this has increased to to 7% according to PwC. And the ‘digital hybrids’ (customers who switch between laptop and smartphone) have grown from 4% to 16% during the same period. The result? … the ‘omni-channel’ segment has shifted from almost 60% of customers in 2012 to less than 50% today.

The Impact of Demographics

As would be expected, consumers in the 18- to 24-year-old bracket are the heaviest users of mobile banking, with 82% of smartphone owners in this demographic segment using mobile banking. As reinforced by many channel use studies, the penetration of mobile banking decreases as age increases. In fact, only 29% of smartphone owners in the 65+ age group reported that they use mobile banking. While income level is positively correlated to digital banking use, affluence doesn’t have as much of an impact on the behavior of the youngest and oldest consumers.

What this means is that determining channel preference goes beyond simple demographics (age and income), requiring deeper analysis of consumer behavior, product use and life stage. For many consumers, the use of channels is even based on the type of transaction and geographic location. According to the research report, “For a bank to deliver against its customers’ needs, it now needs very sophisticated analytics and personalization capabilities.”

Read More: Gen Z Prefers Banks to Big Techs, But Shuns Branches

Beyond Demographics … Digital Experience Matters

Even with perfect data, analytics and targeting, the digital consumer is very aware of options and can quickly shop for the digital experience that meets their needs for any particular financial services solution. For instance, if an ‘omni-digital’ consumer is in the market for a loan, and their primary financial institution proactively connects with them with an offer, the digital consumer still does their due diligence. If the application, approval and funding is not seamless, the customer will look elsewhere.

The digital customer demands experiences that are easy to use. The online retailers, travel, hospitality and tech companies have set the expectations for omni-digital customers. Prospects will appreciate the ability to do a quick click on an email offer link, but they’ll frequently abandon the process if there are too many steps. They know there are options.

What About Branches?

Any analysis of consumer preferences for branches is difficult at best and inaccurate at worst. The challenge is that nobody wants to eliminate something they have become used to, even if they may never use one in the future. Add to this bias the fact that most banks and credit unions have not provided enough support to digital channels for the consumer to avoid using a branch altogether.

PwC found that branches continue to be an important channel for a variety of services. Almost half of those surveyed said they’d prefer to open a new deposit account or apply for a new loan in person (the percentage was closer to two-thirds only 3 years ago). Moreover, 25% said they wouldn’t open an account with a financial institution that didn’t have local branches.

While the frequency of branch visits has been declining, some interesting ‘aberrations’ come to light in the use of physical facilities. For instance, many Millennials prefer to visit a branch to open a new account, learn about budgeting, understand retirement options, and to understand and apply for a mortgage.

When looking at the importance of branches, financial organizations need to take into account the higher cost to serve in a bricks and mortar facility. On average, branches cost banks $4.00 per transaction, according to PwC. On the other hand, online (PC) and mobile banking cost $0.09 and $0.19 per transaction, respectively. This comparison makes the big assumption that support staffs will be reduced when the digital shift happens (an assumption that could be argued).

In addition, omni-digital customers also use more services and provide more revenue. The survey indicates that consumers who use self-service channels (mobile, online, tablet) also report a greater need for a range of financial products.

Responding to the Digital Shift

So, how should banks and credit unions adjust their priorities to respond to this transformational shift in the way consumers do their banking? According to the report, “At the very minimum, this should be a wake-up call for many US financial institutions. They may think that they’ve got more time to adapt than they really have.”

The trend toward greater digital interaction is strong and growing. As an industry, we need to realize that many transactions being done in physical channels are done so because users have no choice. The vast majority of banking organizations do not provide end-to-end digital engagement options. From new account opening to customer support, the omni-digital customer is forced into a channel they may not prefer.

To keep pace with consumer expectations, PwC suggests that banks and credit unions will need to do a much better job of:

- Selling to buyers at the time, place and channel they prefer

- Using digital strategies to make products easier to use (think ‘one-click’)

- Offering personalized products and services that are both timely and relevant

- Moving to a real-time delivery of information that can help consumers manage their finances

While the strategies and priorities of each financial institution may be different based on their digital maturity, all organizations must speed up their digital transformation efforts to keep up with the rapidly changing expectations of the digital consumer.