To serve a changing market and respond to new competitors, retail banks and credit unions are rethinking and expanding the role of Chief Information Officer (CIO). Beyond improving the front-office and back-office digital functionality, the focus is increasingly on improving the consumer experience across the entire customer journey.

A survey of 50 banking CIOs by Cognizant sought to identify best practices for digital banking CIOs — in particular, how they partner with other department heads while integrating digital business capabilities into their organizations. The research also explored the challenges facing CIOs in their efforts to transform their organizations.

Among the key findings uncovered by their research:

- A large percentage of CIOs (45%) say they are leading the digital transformation charge, followed by the CEO (38%) and CMO (8%)

- 70% of CIOs identified organizational culture as the primary obstacle to digital business success, with 66% citing a lack of commitment from the board and/or CEO

- 55% of the CIOs feel their digital efforts have been successful, while 26% believe they have been moderately successful

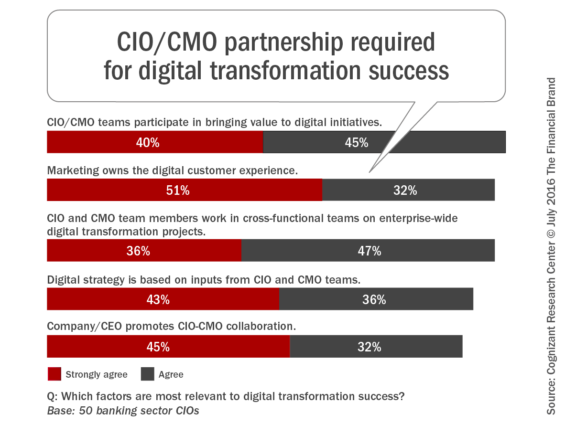

CIOs also cited an increasing need to collaborate with chief marketing officers (CMO), sharing insights to improve multichannel experiences, product development, needs identification and personalization. Responding to these new challenges and expanded role, CIOs see the need to continuously remake and aggressively up-skill themselves and their organizations, according to Cognizant.

Drivers of Digital Transformation in Banking

Cognizant identified five primary drivers of digital banking transformation that provides the foundation for the CIOs new role and responsibilities:

1. Accelerated pace of innovation. New technologies are providing new opportunities for CIOs to advance their organization’s product and service offerings.

2. Expanded customer-centric initiatives. A more technologically fluent consumer has forced banking organizations to focus on improved insight-driven personalized experiences. Beyond basic digitization of processes, CIOs need to understand consumer expectations being set by non-financial organizations.

3. Multichannel distribution and consumption. The digital consumer expects a consistent experience across touchpoints and channels. While digital banking has changed basic transactional interactions, branch banking still remains strategically important. As a result, CIOs must consider all channels and customer touchpoints as part of a strong digital strategy.

4. End-to-end process digitization. CIOs need to digitize the entire systems landscape, from the front office to the back office.

5. Enhanced customer service through digital tools. CIOs need to utilize digital tools to deliver new service offerings (P2P lending, crowdsourcing, PFM, etc.), and provide meaningful and relevant customer service experiences.

The CIO as a Collaborator

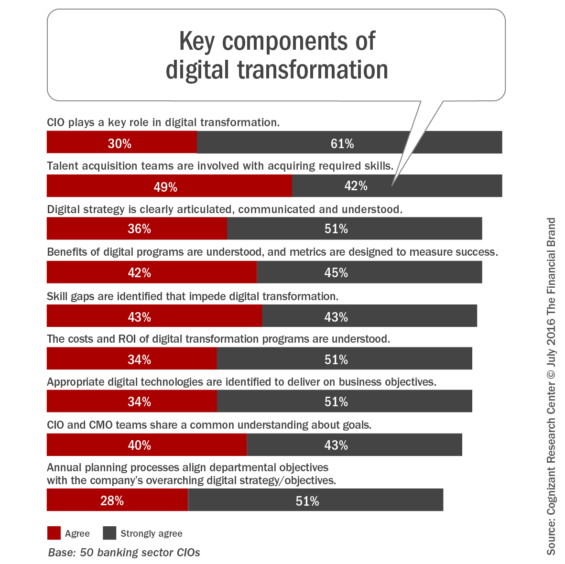

As the importance of digital technology, delivery and innovation increases, so does the collaborative responsibilities of the banking CIO. According to the Cognizant research, “Banking CIOs believe the essential elements for a successful digital transformation revolve around leadership, filling skill gaps, developing a clear strategy and understanding the benefits enabled by ‘being’ (vs. merely ‘doing”’ digital.” This requires expertise beyond the capabilities of the CIO.

To succeed in the new digital banking environment, Cognizant found a need for CIOs to expand the depth and breadth of their relationships within their organizations, particularly with senior leaders in business and marketing, as well as with specialists in digital strategy, enterprise architecture, infrastructure management and data management. CIOs should also be actively involved in shortlisting and selecting third-party partners, and in developing relevant performance requirements and measurement approaches.

Because of the increasing capability to economically and efficiently transform data into insights with new advanced analytic tools, there is an increasing need for the CIO to share insights with marketing (CMO) to enable the delivery of personalized solutions which yield a better customer experience. This partnership may not feel ‘natural’ to either the CIO or CMO, but it is required to compete against new start-up organizations that use well designed and easy to use digital tools as a competitive differentiator.

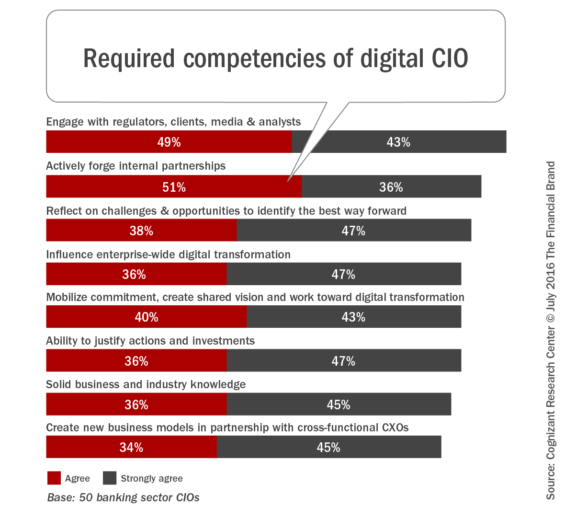

The CIO as an Agent of Change

While the CIO must manage legacy systems, they also must be the voice of change within the organization, actively embracing and nurturing a startup mentality. They need to be at the forefront of innovation within the organization, engaging stakeholders on the promise and challenge of integrating digital tools and techniques into current and new processes. According to Cognizant, “CIOs must act as innovators who are willing to stake their reputation on rethinking traditional banking approaches and investing in new financial technologies.”

Wearing the ‘change agent’ hat will be new to most CIOs within banking. But there are other roles and responsibilities that the CIO needs to assume to be successful as shown below. Unfortunately, significant barriers to success remain. According to the research, roughly 70% of respondents identified corporate culture as the primary obstacle, and 66% cited a lack of commitment from the top levels of the organization.

CIO Imperatives: Where Are We Today?

As banks and credit unions transform to increasingly more digital organizations, there are several imperatives for the banking CIO.

Transform the customer experience. One of the primary imperatives of the digital bank CIO is to transform the customer experience. According to the Cognizant research, more than half of the CIOs (55%) feel they have been very successful in meeting these digital goals, while an additional 26% say they have been moderately successful.

Multichannel integration. The survey found that most banks are not yet taking an integrated, multichannel approach despite making major investments in digital services. Only 38% of respondants are providing some digital services to customers, with limited channel integration. Only 25% are providing advanced services, such as a mobile wallet, with a high degree of channel integration, and just 19% are providing advanced services with full, multichannel integration. About 38% of respondents said their institutions have integrated online and mobile banking channels, and roughly 30% have integrated social and mobile channels. A smaller number (23%) have integrated their online, social and mobile channels.

Digitize middle-office and back-office. Only 38% of CIOs said their banks are seriously considering the digitization of middle-office functions, and about the same number (36%) said they are considering a transformational solution for the back office, such as their core banking platform.

Digital tools for customer-facing personnel. Beyond direct-to-consumer digital solutions, there is still a need to provide digital tools for customer-facing employees. Cognizant found that approximately 45% of CIOs found these type of tools to be a high priority.

Where Will We Be Tomorrow?

While CIOs may be relatively well positioned for today’s needs, there appears to be significant challenges on the horizon that will require expanded skill sets and capabilities. The most significant challenge may be the integration of legacy and modern digital systems, capabilities and expectations. Some of these needs can be met through improved collaboration with other leaders within the organization, such as the CMO and customer experience officer (CXO).

Central to the need to improve the digital customer experience will be the collection, analysis and deployment of customer insights to enable the personalization of products and offers similar to what has been achieved in other industries. This collection and application of insights will need to be across traditional internal silos and across distribution and communication channels externally. The key will be to achieve this seamlessly from the consumer perspective.

“CIOs who remake themselves and their organizations into digital beings will be positioned to seize the high ground, particularly as digital proficiency continues to separate winners from also-rans in an increasingly congested and competitive retail banking market,” states Cognizant.