Banks and credit unions know the value of personalization — how it can lead to greater loyalty and an increase in primary account relationships. But that expectation is largely unfulfilled.

That’s because creating primary relationships has typically been approached through product acquisition. And those acquisition efforts have been personalized in only the most rudimentary way — using name, address and sometimes (but surprisingly seldom) other data such as product usage and product relationships.

It’s not that financial marketers aren’t trying. But whether the barrier is data silos, data movement or lack of confidence in the quality and depth of data, there are major challenges to executing fully personalized strategies.

The Customer Journey Has Greatly Changed

Marketers often use words like “journeys” to explain how people interact with brands. They also talk about the sales funnel and divide tactics up by “top of the funnel”/awareness, “mid-funnel”/performance and “bottom of the funnel”/conversion. But the explosion of signals and channels has meant buying and shopping and research behaviors are no longer linear, with people moving up and down the funnel during the buying process.

No More Straight Lines:

Buying journeys used to be relatively linear. The digital explosion has completely altered the sales funnel and the way people shop for financial products.

People today may emit buying signals by clicking on an ad, but then spend weeks doing comparison research before visiting the financial institution’s site and filling out an application. They will have interacted via mobile device, desktop and possibly tablet, clicking ads and visiting sites and social media pages. All these interactions are opportunities for the bank or credit union to recognize them, determine a message and present that message.

Each interaction emits a digital signal. But who sees the signals? The answer is nobody — unless the signals can be pulled out of the channel or app silo and into a “customer intelligence framework.”

Customers Become Happier Only When You Know Them

Imagine a scenario where a bank or credit union uses insights about a customer to deliver solutions when the customer needs them, cultivating a sense of trust, loyalty and financial wellness. This translates into more profitability and longer customer tenure for the institution.

But in truth, converting all the raw data available into insights about customers is extremely difficult to pull off.

Raw data generated by a customer interaction can live in apps, in channels, in product lines, in marketing and enterprise databases. This challenge could be replicated across business lines, channels and product lines.

The Data Conundrum:

There are often several versions of the customer relationship within an institution, none of which are the complete truth.

Relying on raw data to personalize communications can lead to a disjointed and confusing narrative for a customer, who is probably wondering why the institution doesn’t seem to know them. The miss is often as simple as an existing credit card holder getting an offer for the same card, or a checking customer being offered a home equity line of credit when the customer doesn’t own a home. This is still all too common.

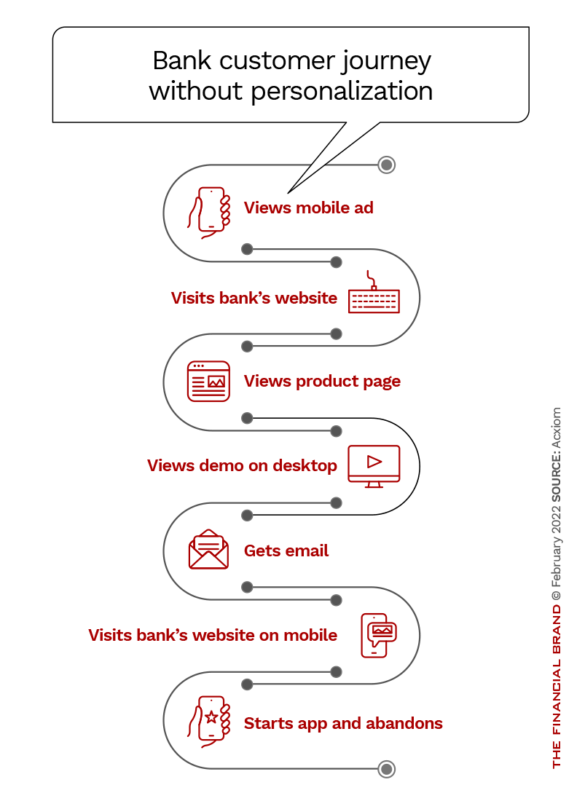

Below is a depiction of a typical non-optimized digital journey for a banking product.

What a More Effective Framework Looks Like

A customer intelligence framework could avoid the failed conversions resulting from disjointed marketing. Such a framework is made up of technology, data and strategy. To be successful, a financial institution needs to look at all three elements:

Technology

Optimized Identity. Identity resolution is a process by which people’s signals are collected in a centralized repository at the individual level. Data indicating life changes — moving, getting married, divorced, etc. — can be tied together to build a more complete view of a person.

Newest Thinking on Identity:

People’s digital profiles should be as robust and vital as their offline profiles, and should be stored and managed compliantly within a first-party identity graph.

Clean and complete data when resolving identity gives financial marketers the best chance of reaching people where they are now. This isn’t just a point-in-time solution, it is the backbone of the modern marketing technology stack and critical to orchestrating good, personalized experiences.

Optimized decisioning. Decisioning is a combination of business strategy and technology. It’s choosing the right message for the individual and activating that message. Most commonly the tools used to execute decisioning are a combination of real-time data stores housing offer databases, and customer data platforms, or CDPs.

The decisioning tool should be fully integrated with the identity graph, ensuring accurate recognition and activation.

Data

The identity solution can accommodate offline and online data and can also be informed by third-party marketing data, CRM data and other enterprise data. Ideally these disparate sources will be integrated and stored in a repository that can be accessed for campaigns.

Read More:

- Banking Needs To Prepare For Marketing’s Data Arms Race

- Internal Data Unlocks Improved Consumer Banking Experiences

Strategy

Strategy in this context is the focus on creating personalized, relevant and valuable experiences for the customer and the financial institution. It starts with developing top use cases, understanding the desired outcomes and behaviors that will deliver business results, while creating loyal customers.

Change the Focus:

Too often banks and credit unions prioritize product sales above good experiences. If they focused on experiences, product sales would naturally occur.

Personalization should be additive to customers’ experience with their bank or credit union; it should make them feel known and, ideally, understood.

That’s why financial institutions need to ensure their customer intelligence strategy delivers on three key objectives that, when met, will create better customer experiences and more loyal primary relationships:

Objective one: Provide a consistently delightful experience in every channel, whether digital, call center or branch.

- Deliver personalized and contextual experiences.

- Be preference-driven.

Objective two: Focus on customer lifetime value.

- Understand the unique needs of customers at each stage and message accordingly.

- Show you know people by delivering relevant messages at each interaction.

Objective three: Take advantage of every interaction.

- Be purposeful in servicing messaging.

- Quickly identify site visitors.

- Leverage data and technology to build robust customer profiles.

Starting Small Often Makes Sense

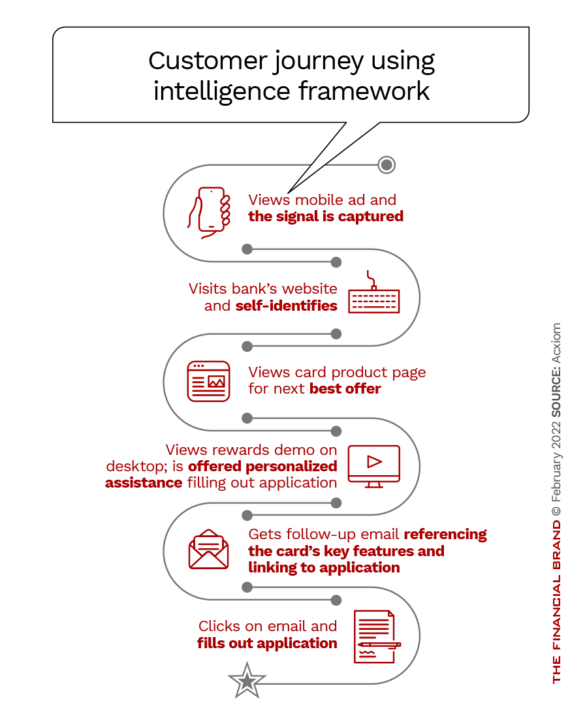

Building such a comprehensive data framework can seem daunting at the outset. In fact, it may make sense to start with a single use case, such as identifying site visitors, or enabling tellers or call center agents to make the next best offer to a customer. Below is an example of an improved customer journey based on the three framework factors.

Even starting small, however, financial marketers will need to make sure they’ve considered the technology, data and strategies involved to make the use case work.

With a customer intelligence framework in place, banks and credit unions can begin to fulfill the promise of creating great personalized experiences for consumers. Better experiences drive loyalty and propensity to consider additional products and services. In short, they create primary customers.