As mobile technology evolves and customer journeys are digitized, being able to gather data and conduct post-event analysis is no longer enough. Consumer expectations are being set by companies like Google, Apple, Facebook and Amazon, where real-time predictions about future needs and behaviors build enhanced experiences.

The marketplace is quickly moving from “mobile-first” to “AI-first”, evolving from a descriptive analytics model (rear view mirror view) to a predictive analytics model (insight GPS view). With predictive analytics, we are in a better position to ‘know the consumer’, ‘look out for the consumer’, and ‘reward the consumer’, learning from previous experiences and predicting future behavior.

Banks and credit unions that are not yet leveraging predictive analytics need to begin harnessing the power of this technology today to ensure competitiveness in an increasingly digital marketplace. This is the perspective advanced by the Predictive Analytics Working Group at Mobey Forum, in its report entitled ‘Predictive Analytics in the Financial Industry – The Art of What, How and Why‘.

“Banks have great data but if they want to compete in the digital age they need to get more strategic and more professional about how they use it,” comments Amir Tabakovic from BigML and Co-Chair of the Predictive Analytics Working Group at Mobey Forum. “The huge influx of new, specialist, data-centric players in digital financial services also means that (predictive analytics) is already becoming commonplace among the ‘new breed’; new services underpinned by predictive analytics are enabling the next generation service providers to extend their lead.”

Why Predictive Analytics?

Digital banking has reduced the cost of banking for the financial institution, but has made the relationship between the bank and the consumer more distant. There are fewer face-to-face interactions, but significantly more opportunities to interact with the consumer overall.

Analysis of these interactions, combined with already available customer insight, provides an opportunity to make banking more personalized, more real-time and more solution-focused than in the past. Advance, predictive analytics can improve the customer experience throughout the digital journey of a consumer, adding value for both the customer and the bank.

According to Mobey Forum, there are four reasons why now is the time for banks and credit unions to embrace predictive analytics:

1. The Consumer. As mentioned in numerous reports and journals, consumer expectations are growing exponentially based on the digital experiences they have with non-financial organizations. They expect the organizations they interact with to have accurate data and to be able to provide proactive, personalized insights and recommendations that will save them money, make them money and improve their daily life. Predictive analytics provides the foundation for these interactions.

2. The Mobile Device. The smartphone is the perfect digital device for the collection of insight and the distribution of real-time insights and solutions. Mobile transactions and geolocation insights are tremendous data sources for predictive analytics. Wearables and the Internet of Things (IoT) will only enhance the accuracy of insights.

3. The Data. The advanced data storage and analytic capabilities that were viable for only the largest of technology firms just a few short years ago are now within the financial and intellectual reach of the smallest of firms. “The costs of storing data have fallen below the costs of deciding which data to keep and which to delete,” stated Mobey Forum in their report.

4. The Competition. As the ability to collect, process and apply data becomes easier and less expensive, non-bank and challenger fintech firms are in a better position to ‘catch up’ to legacy banking organizations in the ability to deliver a personalized digital solution. The current window of opportunity is closing for legacy banking organizations.

Types of Business Analytics

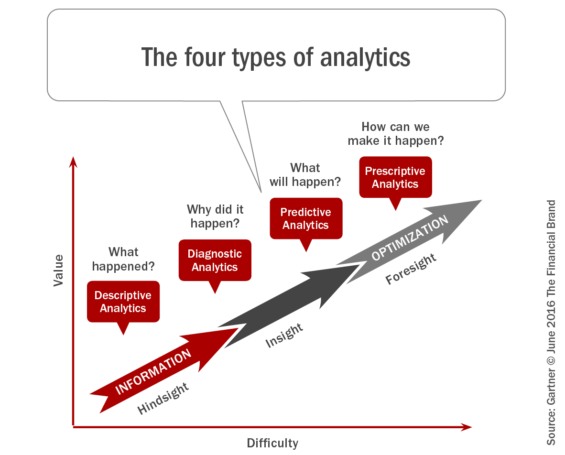

According to Gartner, if an organization is using data to understand the past, the process is usually referred to as either ‘descriptive’ or ‘diagnostic’ analytics. These tools answer the questions, ‘what happened and why?’.

‘Predictive analytics’ moves the view from an historical orientation to a forward-looking perspective. The objective of predictive analytics is not just to describe and understand the past, but to explore ‘what is likely to happen’. Unlike descriptive or diagnostic analytics, predictive analytics is not as precise and is based on probabilities.

The fourth type of analytics is ‘prescriptive analytics’, which tries to answer the question “How can we make it happen and what should we do?” According to Gartner, only 3% of companies are currently using prescriptive analytics. With each step up the ‘analytics ladder, the difficulty of analysis increases but the potential value of the insight also increases.

Many financial services organizations confuse descriptive analytics with predictive analytics. According to Mobey Forum, the following questions must be answered positively for the analysis of data to be considered predictive analytics:

- Is there a fact-based prediction of a future value of a variable (action or event)?

- Is this prediction obtained by relevant past information in similar contexts?

- Is a rational decision made based on the fact-based prediction of the future value?

“It is important to emphasize that predictive analytics is not about the size of the data, but about using the data to improve decision support,” states Mobey Forum. “Since organizations already face challenges in ensuring the quality

of current data, there is an incentive to start small, rather than directly incorporating ‘Big Data’ in predictive analytics cases. Said differently, more low quality data is not likely to improve predictive capabilities.”

Ways to Create Value with Predictive Analytics?

There are several ways to create business value from using predictive analytics including product/service effectiveness, risk control, operational efficiency and financial controls. Some of the examples discussed in the Mobey Forum report include:

- Card-linked offers (merchant funded rewards)

- Next best action marketing (offers, service, financial advice, etc.)

- Pricing (relationship-based or activity-based)

- Risk assessment (predictions of future behavior)

- Predictive maintenance (predicting equipment failures)

- Claim handling (prediction of fraudulent claims)

- HR analytics (finding good potential employees based on current staff)

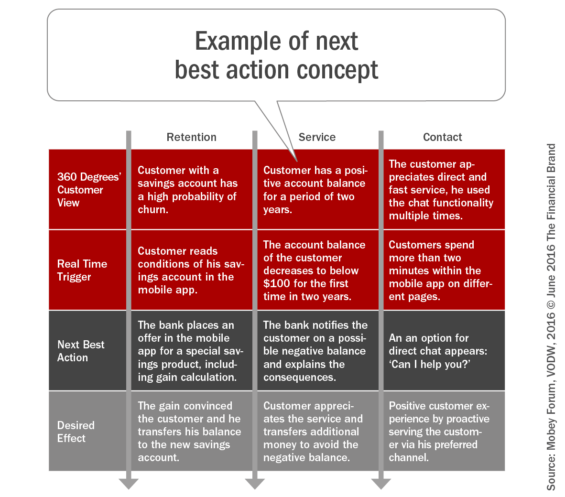

The Power of Next Best Action (NBA) Opportunities

The digital consumer is interacting actively and passively at every moment, through transaction, interactions and even movement. Each interaction provides a bank or credit union with knowledge about the customer, allowing the organization to better serve that customer, constantly adjusting service and offers based on the real-time context of that customer.

In the past, offers were delivered to pre-set segments at set times based on market intelligence around buying patterns. There was no differentiation based on individual customers, needs or recent events.

Next best actions driven by predictive analytics provides real-time recommendations, or real-time automated actions. Beyond determining offers/recommendations, NBA concepts also consider the optimal channel for the offer or interaction based on current channel, channel preferences, or even location (branch, store, ATM, etc.).

As opposed to delivering offers or recommendations at a set time for a segment of customers driven by periodic analysis, next best actions take all historical data and combine this insight with real-time event triggers. The analysis of these opportunities is done in real-time on an ongoing basis. This results in significantly better results, since the personalized communication is delivered at the time and channel identified by customer activity.

“Using next best action in the mobile journey is therefore not just focusing on sales, but it is a way to constantly help customers in their financial mobile journey,” states Mobey Forum. “When the timing and context are right, the personalized customer experience will boost customer loyalty and profit in the long term.”

Moving Up the Analytics Ladder

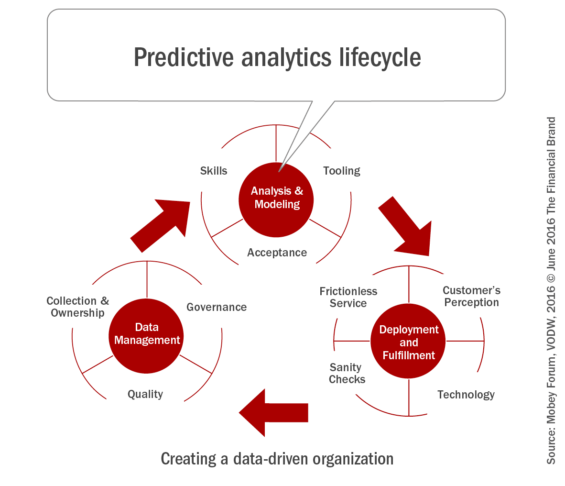

Moving up the analytics ladder from a ‘rear view mirror’ view to an ‘insight GPS’ perspective comes with challenges, not the least of which is whether or not an organization is prepared and equipped to embrace a data-driven culture. To succeed, an organization needs to use data and advanced analytics in every part of the organization and with every decision made. It also means transforming from a product oriented organization to a consumer-centric organization.

In the report, Mobey Forum examines the ten challenges on the predictive analytics lifecycle that frame key questions about an organization’s readiness for successful use of predictive analytics. The report also contends that financial institutions should ‘think big, start small, but start now’ and work on building a digital services infrastructure with data analysis at the center, which can be leveraged to support the whole business over the long term.

“There is also huge opportunity for banks with predictive analytics,” states Sirpa Nordlund, Executive Director, Mobey Forum. “From now on, it’s all about the data. With predictive analytics, banks and credit unions can not only generate a 360 degree view of their customers’ financial behavior, they can anticipate their needs and create highly personalized services that surprise and delight them too, cementing their relationships for the long term. Banks can establish greater relevance and appeal, increase trust and ultimately create a more stable commercial and operational footing in the digital age.”