The mobile customer experience has become an important battleground for financial services, with both established players and fintech startups developing new offerings that put a greater level of convenience into the hands of consumers. Mobile payments, mobile wallets, dedicated banking apps, and even offerings outside of the banking industry are setting an increasingly higher level of expectations around what consumers are looking for in terms of an improved user experience.

The ability to collect and process both structured and unstructured data to create actionable insights is becoming a competitive differentiator and focus of financial services leadership. Unfortunately, much of the available data is not being fully utilized by the majority of organizations.

In conjunction with the development of new digital channels, improved data analytics and mandates to improve the customer experience, the development of the CX role within financial institutions has become part of an accelerating arms race that will ultimately benefit consumers, according to a report from WBR Digital and OpinionLab.

The research found that the majority of financial services firms are in the process of expanding their CX projects, with mobile representing a significant area of opportunity. Unfortunately, adoption is stymied by the difficulty of gaining resources to pursue new projects.

“It is no surprise that we are continuing to see a growing focus on CX throughout the financial services industry, especially as customers increasingly make their decisions based on the ease with which they can interact with a financial business,” stated from Jim Reitz, Head of Financial Services Practice at OpinionLab. “Firms need to find ways to integrate unstructured customer feedback into the customer data that drives business insights, especially in the area of mobile customer experience, if they want to remain a competitive force in the current industry landscape.”

Key findings from the survey include:

- The majority of financial services businesses are in the process of expanding their CX projects

- Mobile represents a significant area of opportunity, but adoption is stymied by the difficulty of gaining resources to pursue new projects

- Interpreting unstructured feedback into actionable insights is an area where the majority of institutions are struggling

Customer Experience is a Priority… Sort Of

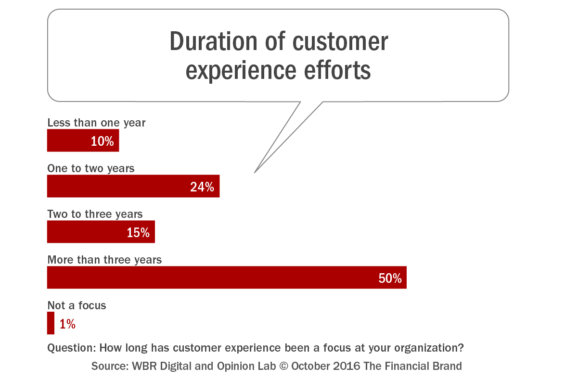

Customer experience represents a recognized priority for financial organizations, and virtually all of those surveyed for the research indicating that CX has been a priority for at least a year. Only 1% of respondents claim that customer experience is not a focus, while 50% have been focusing on customer experience for over three years.

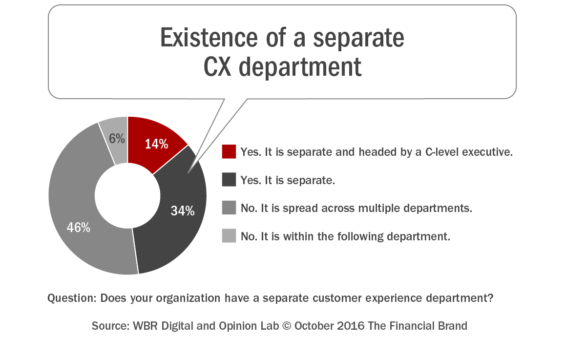

Despite the apparent focus on an improved customer experience the research found that majority of respondents have not yet created a dedicated department with a C-level executive leading the charge. In fact, less than half of those surveyed had a separate department for managing the customer experience (with 14% of those departments headed by a C-level executive). By contrast, 52% of respondents don’t have a centralized CX team in place, with the majority of these organizations (46%) having the CX function across multiple departments.

Resources for CX Initiatives Hard to Come By

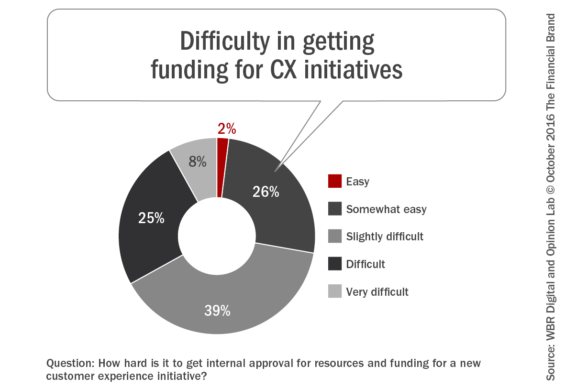

Again, in the category of “actions speak louder than words,” receiving funding for customer experience initiatives is far from a slam dunk. According to the research, “The difficulty in getting the resources needed for CX initiatives will depend on how effectively CX stakeholders can make their case to business leadership and coordinate the execution of new initiatives across the business.”

That said, only 28% of respondents found that gaining internal approval, resources, and funding for new customer experience initiatives were ‘easy’ (2%) or ‘somewhat easy’ (26%). Almost four in ten respondents indicated ‘slight difficulty’ when initiating new projects, with 25% indicating ‘difficulty’ and 8% stating that getting funding for CX projects was ‘very difficult’.

When digging deeper into the reasons for funding challenges, 34% indicated the challenge was related to budget constraints overall, with 16% indicating a lack of strategy and 17% referencing execution issues. The good news is that the majority of respondents (69%) report that the level of investment they are getting from the business has increased over last year, with 29% of respondents working with the same budgets as the year before.

The Mobile CX Opportunity

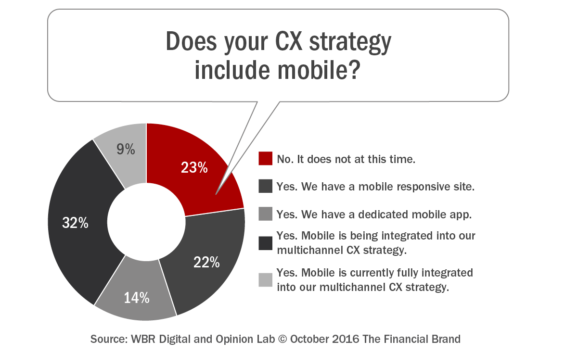

Despite the significant shift to mobile by the majority of bank and credit union customers, just under a quarter (23%) of respondents have not yet made any efforts to include mobile in their CX strategies. Only 22% of respondents indicated that they had a fully responsive mobile site, with 14% having introduces a dedicated mobile app.

The largest single share of respondents (32%) indicated that they had a fully operational multichannel strategy, and are currently ‘working on’ integrating their mobile operations with their greater CX strategies. Less than 10% have fully integrated mobile into a multichannel CX strategy, according to the research study. The biggest challenge around development of an integrated mobile CX strategy was the ability to consolidate data and insights into a single customer record.

Measuring Success

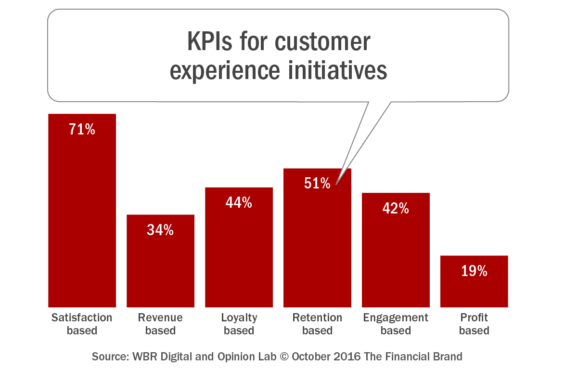

As could be expected, the research from WBR Digital and OpinionLab found that the KPIs used to measure customer experience initiatives varied based on how the company views their CX strategy as part of the greater business. Seven in ten (71%) respondents said ‘customer satisfaction’ was the primary yardstick for measuring their improvements to the customer experience.

The second most common measurement of success mentioned was ‘customer retention’, which was indicated by 51% of the respondents. It was a bit surprising that while loyalty and engagement were also strongly represented KPIs (44% and 42% respectively), just a third of organizations (34%) used financial metrics as a measure of success. According to the research, “55% of respondents have seen the success that they’ve been looking for reflected in their measured KPIs, while another 45% are still waiting to observe the results of their efforts or have yet to implement measurable CX strategies.”

Leveraging unstructured data, such as comments on social media, emails, or other “non-formal” types of feedback represent a major opportunity for brands to gain information from their customers that, when synthesized into actionable insights, can be extremely valuable states the research. The use of this data enables a financial institution to paint a more full picture of each customer or member and improve the overall personalized experience.

The share of respondents who thought they had already mastered the ability to turn unstructured data into actionable insights is just 6%. Over double that percentage (13%) stated that they were unable to utilize the unstructured data available to them.

Recommendations

The report concluded that the more data that can be drawn into understanding customer mindsets and creating actionable insights, the more decisively a CX team can act and convey the case behind their initiatives to key business leadership. This includes both structured and unstructured data that can fully personalize the customer experience.

Mobile was also indicated as an area of opportunity for financial institutions. As organizations seek to improve their mobile offerings, there is an opportunity to better integrate CX into the DNA of all digital offerings.

Finally, the research suggested increasing a focus on gathering customer feedback and data insights internally, while also leveraging third party insights, employing solutions that will reconcile customer data and feedback from multiple channels into a single data repository.