Making digital banking experiences convenient and easy should be a top priority for all financial institutions. With over 75% of the U.S. population banking online in 2022, according to eMarketer, ensuring that digital experiences are frictionless is imperative to providing overall satisfaction with your customer service.

In contact centers across the country, call volumes are drastically rising and maintaining trained support staff to handle these incoming calls is growing increasingly difficult. The symptoms of this challenge are lengthy wait times for consumers desperate for support help, and a frustrating customer experience that erodes loyalty and sends the institutions CSAT metric into freefall.

Many banks and credit unions recognize the growing pain point, but are attempting to tackle the issue through traditional means. While pursuing costly but straightforward solutions like increasing the size of their call centers, they often miss one of the main cruxes of the problem: About 80% of the traffic directed at call centers are simple, routine transactions.

These are the kinds of questions and requests that most consumers, if provided with adequate self-service tools, could solve for themselves without ever needing to contact customer support in the first place.

Solutions aimed at decreasing volume, not increasing staff, are the most effective way a bank or credit union can ensure their customers and members are spending less time waiting on hold and more time getting satisfactory results for their requests.

A Deeper Look:

Although 80% of call center traffic typically relates to a handful of topics, the actual issues involved can often be complex.

While it’s true that the majority of routine transactional requests can easily be handled by self-service tools, such as chatbots, most existing digital platforms don’t allow for users to adequately help themselves in this manner. This is because while this 80% of traffic is indeed made up of a small subset of repeated topics, there is much more granularity within these topics than simpler tools are able to handle and requires an intelligent tool to understand the user’s needs.

A solution that is capable of interpreting the complex mechanics of natural language is required in order to adequately service the majority of user inquiries and actually lower call center traffic.

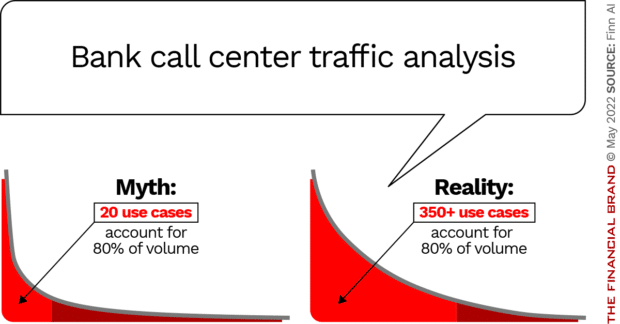

The Myth About Call Center Requests

There’s a misunderstanding by financial service executives regarding support requests that ultimately results in well-intended technology projects that do not succeed: The executives see that 80% of requests are made up of only about 20 or so different topics of discussion. Banks and credit unions may therefore underestimate the degree of sophistication needed in a tool to resolve these support requests automatically. If a self-service tool is deployed based on the idea that only a small fraction of topics are driving traffic, then the tool will prove ineffective at significantly lowering call volumes and truly resolving support requests leading to the cyclical problem of burdened call centers and frustrated users.

A chatbot that can only recognize and respond to a handful of broad topics will only deliver an accurate response a fraction of the time. For example, if a bot can recognize when a user is asking about credit cards and can show them a list of credit card product offerings, this will work only when the user is asking about what cards the bank or credit union offers. What if they’re asking about a problem with their existing card and get the same response?

The categorization of call-center traffic into these broad buckets is useful for gaining a general understanding of support inquiries and customer needs, but is insufficient for determining the actual kinds of questions and requests being received.

These broad topics of conversation are not themselves what drive the majority of call volumes — it is the many distinct inquiries within these topics that truly generates traffic. An ideal self-service tool must be able to direct answers at these granular, specific questions and requests rather than simply at the broad categories they are contained within.

The Reality of Bank Call Center Traffic

In reality, the 80% majority of call center traffic is really made up of over 350 different user questions and requests. These questions, while all categorized into broader topics, often have nuance and granularity to them that means simple chatbots will prove ineffective at properly diagnosing the specific problem that a consumer is having. If a member or customer is unable to have their specific query resolved — and instead is only left with more generalized assistance — they are left frustrated and still need attention from the contact center.

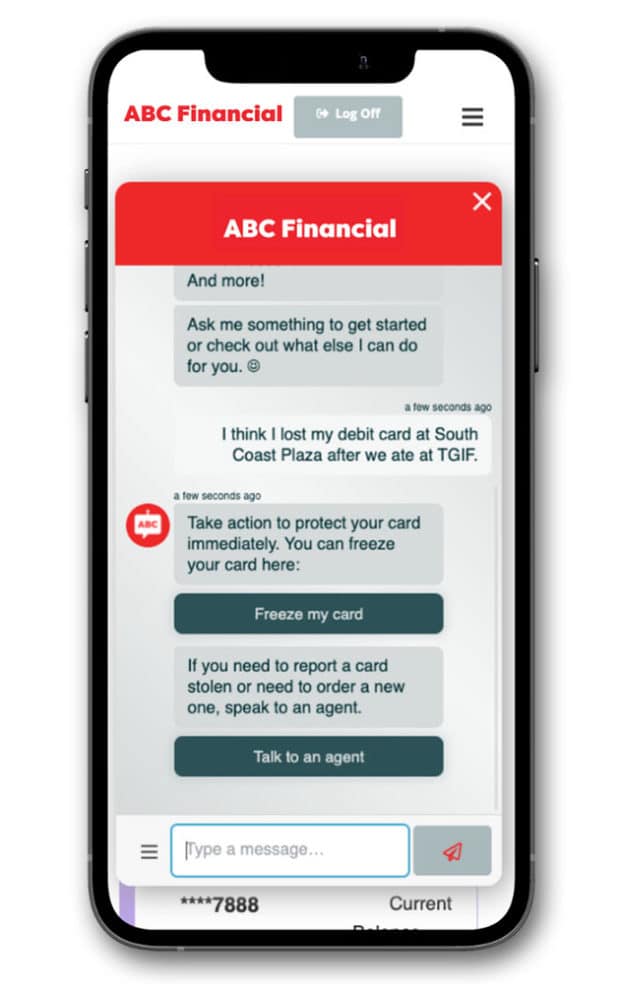

For example, within the topic of “Debit Card Support,” there are many different types of issues a user may be having with their card with each one possibly requiring a different method of service: Their pin could be not working, there could be an issue with the physical card, or the user hasn’t been able to identify what the exact issue they are having is and need troubleshooting. All of these different issues cannot be resolved by a chatbot that can only address the broad “Debit Card Support” topic.

Another reason why a more complex chatbot is necessary is the ways that consumers ask for information, and how user intent can be difficult for an automated solution to understand. Being able to determine which topic is being asked about is easy for a human, but most automated solutions struggle to parse user intentions when asked for in a natural, conversational manner. Understanding the context is necessary to provide an accurate response that prevents a consumer from needing to seek further assistance for their inquiries.

When financial institutions implement self-service tools, they must be intelligent and built using natural language processing (NLP) to ensure that users get accurate responses for their specific needs that don’t prompt them to seek further information.

What is Natural Language Processing?

NLP is a blend of linguistics, AI and computer science that can understand the nuances and dynamics of human conversation and emotion.

A Solution That Learns

A virtual banking assistant, much like a live human agent, excels at understanding the specific problem that a user is having within a broader category. An AI-powered chatbot is purpose-built for retail banking and trained on hundreds of the most common call center questions and requests (in the case of Finn AI’s chatbot, more than 800). Such an intelligent chatbot is able to get down to the fine details and figure out exactly what the user is asking. In 80% of cases, the inquiry can be resolved to completion, avoiding the need to escalate the request to the call center staff.

A well-trained chatbot can ensure that users can get instant help for the routine yet granular and complex transactional requests. For the other 20% that require human help, consumers will experience shorter wait times and deal with support staff that has more time to adequately assist them. A chatbot unable to achieve this same level of granularity, however, will act in a counterintuitive manner by preventing consumers from finding appropriate answers on their own, eroding customer satisfaction by leaving them unsatisfied and still seeking a proper answer.

Empowering members and customers with a set of self-service tools that can intelligently pinpoint their exact problems will free them from the menu-maze of hunting for answers online, and give them immediate access to the help they need. This provides the kind of frictionless, convenient digital customer service experience that drives up CSAT scores and encourages retention.