Simply mentioning artificial intelligence may evoke thoughts of the malevolent HAL 9000 from “2001: A Space Odyssey.” But this isn’t sci-fi; AI is going mainstream.

Most of us have already encountered AI, but probably didn’t realize it. Google’s hallowed search algorithm is pure AI. Same thing for Facebook. Apple’s Siri and the Amazon Echo are virtual assistants built on AI backbones that can respond to a robust range of voice commands. AI has many different shades, flavors, variants and alternate names. Some call it “machine learning.” Others think of “predictive analytics.” Me personally, I like TechTarget’s simple definition of artificial intelligence: giving computers the ability to learn without being explicitly programmed.

While AI has been gaining traction, the use of messaging apps has also been on the rise. Research from GlobalWebIndex shows that 63% of those who use mobile apps are also active mobile bankers. And while the titans of Silicon Valley get the AI + messaging trend — Facebook Messenger, Google Talk, WhatsApp — not everyone in banking is on the same page. Deutsche Bank, for instance, recently banned the use of messaging apps for all employees on work phones (they, of course, cited compliance issues as their reason).

The future of banking interactions will be built using a combination of both AI and messaging apps for customer service, payments, content distribution and alerts. Citizens Bank uses an app called Relay to drive loan completions. They previously noted that customers were not receiving notifications via mail and phone calls, so began using the messaging app to send reminders. Called the “Citizens Bank Wire” service, the app has helped increase loan completions by 10%.

For banks and credit unions looking for an entry-level platform, Facebook Messenger is probably the most user-friendly and easy to set up. They have released developer tools allowing users to customize their own chatbot. You can also work with developers to help you set up chatbots that mimic your brand’s tone and messaging. When a customer sends a message, the chatbot will respond with pre-programmed questions or information to help guide the customer to a solution. CenterState Bank says this approach should be particularly attractive for small to mid-sized community institutions with a small customer service department or limited hours.

Read More:

- Financial Institutions Bullish on Chatbots

- Hello, May I Speak to My Personal Bot?

- The Use of AI in Banking is Set to Explode

- Banking Must Move From Mobile-First to AI-First

- The AI Marketing Revolution Comes to Banking

To Bot or Not to Bot?

There are pros and cons to leveraging AI and chatbots. Let’s start with the benefits.

First, AI saves time. If your institution has limited resources, using an app like Facebook Messenger and creating a chatbot, can reduce or eliminate your team needing to answer basic frequently asked questions. This is one of the main reasons that chatbots have the potential to reduce labor costs for financial service companies by as much as $15 billion, according to Business Insider.

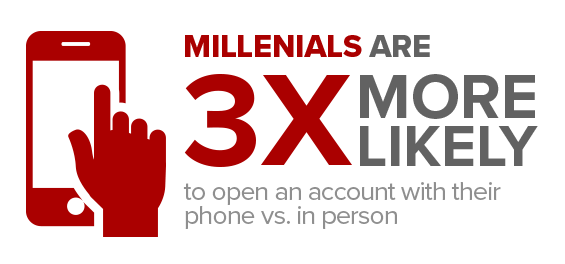

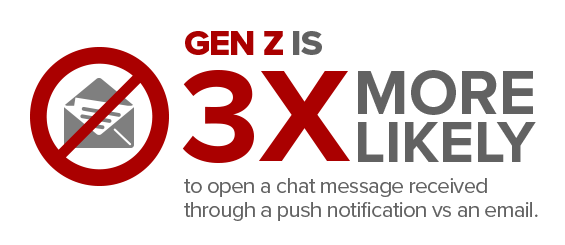

AI also expands your reach. Banks and credit unions that are trying to reach Millennials absolutely need to invest in these technologies. And Gen Z isn’t far behind. According to a study by the American Bankers Association, Millennials are 3x more likely to open a new account with their phone vs. in person. Gen Z takes it a step further. They are digital natives, and mobile features like chatbots are not options, but requirements. Another report revealed that Gen Z dismisses email as an antiquated form of communications. They are 3x likelier to open a chat message received through a push notification.

Banks and credit unions planning to stay competitive with large institutions and fintech payment players like PayPal had better consider how their digital offerings will resonate with future generations.

Now, let’s explore a few of the cons.

AI is next-level technology, and it can get really complex very quickly. You will have to decide what questions your bot will respond to, and provide the correct answers. Turnkey platforms like Facebook will give you step-by-step instructions for creating chatbots, but developers will need to create the code to make sure all actions are executed properly.

https://developers.facebook.com/docs/messenger-platform/guides/quick-start

AI also still requires human intervention. As with any social media or digital channel, the technology is only as good as the people managing it. One example of a bot gone bad was Microsoft’s “Tay on Twitter” chatbot. Tay was taken over by internet trolls who manipulated the bot to praise Hitler and several inappropriate topics before Microsoft could shut it down. And while bots may be able to take people up to a certain point, you must be prepared with a response strategy in cases where the dialogue warrants human intervention. Developers need to be prepared for technology updates and bugs that might interfere with the user experience.

What’s the Bottom Line on AI and Chatbots?

It’s not really a question of if, but when your institution needs to begin exploring messenger apps and AI. Larger banks such as Wells Fargo and Bank of America have already launched robust messenger bots. A survey conducted by Personetics shows that over three quarters of financial institutions view chatbots an opportunity, and that most plan to launch a chatbot in the very near term.

For banks and financial institutions looking for new business from Millennials and Gen Z, leveraging chatbots will be a necessity. This technology is set to skyrocket in the next 12-24 months. AI is getting smarter, it’s evolving quickly, and going mainstream — not just in banking, but in our day to day lives.

Mikki Ware is the Digital Marketing Director at Gremlin Social, a social media marketing and compliance software company in St. Louis. Mikki is a digital marketer with seven years’ experience in B2B marketing and software as a service. Mikki develops and executes integrated web and social media marketing strategies, and assists Gremlin clients looking to leverage digital strategies to achieve their business goals.