Artificial intelligence (AI) is not new to banking. If we consider that the definition of AI is the ability for machines to interact and learn to do tasks previously done by humans, the history of AI goes back to the 50s in the banking industry. Through machine interaction and learning, natural language can be processed and decisions made faster and more accurately than was possible in the past.

One of the outcomes of artificial intelligence is that machine learning improves over time as more data is processed and more positive results achieved. In fact, Ray Kurzweil from Google estimates that AI will surpass human intelligence by 2019. Despite this achievement, and successes in virtually all industries, banking has taken a more cautious approach.

Heightened interest in AI has occurred because of both capabilities and business needs. The explosive growth of structured and unstructured data, availability of new technologies such as cloud computing and machine learning algorithms, rising pressures brought by new competition, increased regulation and heightened consumer expectations have created a ‘perfect storm’ for the expanded use of artificial intelligence in financial services.

The benefits of AI in banks and credit unions are widespread, reaching back office operations, compliance, customer experience, product delivery, risk management and marketing to name a few. Suddenly, banking organizations can work with large histories of data for every decision made.

Adoption of AI in Banking

Most banks and credit unions are in the early stages of adopting AI technologies. According to a survey conducted by Narrative Science in conjunction with the National Business Research Institute, 32% of financial services executives surveyed confirmed using AI technologies such as predictive analytics, recommendation engines, voice recognition and response.

For those firms not adopting AI, challenges such as fear of failure, siloed data sets and regulatory compliance were cited. Based on the Narrative Science survey, 12% of the overall group weren’t using AI yet because they felt it was too new, untested or weren’t sure about the security.

Another key challenge for many organizations was that there is no clear internal ownership of testing emerging technologies

— only 6% of those surveyed having an innovation leader or an executive dedicated to testing new ideas and processes. Not having a person or department assigned to testing new ideas is obviously a problem.

Data, Data, Data

Data is being collected, analyzed and applied to solutions more extensively and faster than ever before. AI makes it possible to automate vast amounts of data, analyzing and applying it at record speeds.

New cognitive-based solutions also enables a more pro-active and personal customer experience at a lower cost than was ever possible before. This is driven by AI’s ability to build knowledge at high speed, understand natural language, and run operational processes in a fully compliant fashion.

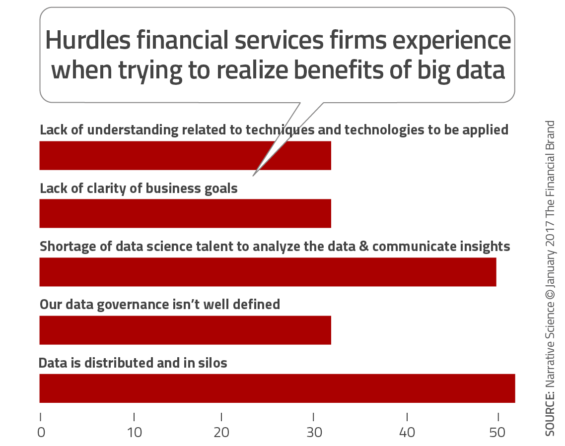

Two of the biggest challenges that remain in banking is the absence of people experienced in data collection, analysis and application and the existence of data silos. This was reflected in the research done by Narrative Science. The good news is that many data firms now have the capability to do a ‘workaround’, collecting data from across the organization.

The Benefits of AI in Banking

Despite early hesitation in the industry around the commitment to AI, there are several use cases.

Enhanced Customer Personalization

The number one trend identified in the 2017 Retail Banking Trends and Predictions was a renewed focus on the customer experience. In another Digital Banking Report, The Power of Personalization in Banking, it was found that consumers want to share their personal information if they can receive custom advice, offers and service based on this shared insight.

Personalized communications and advice as enabled by AI can be reflected by robo advisors – online wealth management services that provide automated, algorithm-based portfolio management advice without the help of a human counterpart. With AI, algorithms can regularly rebalance the portfolios to maintain the original investment guidelines and operate at costs less than 100 basis points (compared to 2 – 3% for traditional brokers). Initially promoted by fintech firms like Betterment and Wealthfront, robo advisors are now part of the offerings at traditional brokers as well.

Beyond robo advising, many other of the larger financial institutions globally are using AI to improve the personalization of offers and communication. Going forward, it is believed that custom marketing and solution development to improve the customer experience will be the primary use case for financial organizations.

Productivity Gains

From customer communication flows to basic back office processing, AI can take rather routine, repetitive processes and make them both more efficient and effective. What once was a very tedious process of new customer onboarding communication can now become highly personalized interactions based on individual activity post opening. This level of personalization was almost impossible to achieve without the benefits of machine learning and AI.

Another application is the ongoing update needed to compliance requirements, customer informational documentation and even product ‘frequently asked question’ responses. With a foundation of continuously changing facts and product updates, all related communications can be changed immediately.

Fraud Detection

One of the earliest uses of artificial intelligence in banking was around fraud detection. By an ongoing review of account activity patterns can be monitored, with aberrations to patterns being flagged for further review. Over the last decade, AI has not only significantly improved the monitoring process, but is now able to respond in real time to potential fraud.

According to Narrative Science, “For example, Feedzai use machine learning to evaluate transactions and millions of data points in real-time. The company maintains an operational model and a challenger model that it constantly evolves as threats change. When the challenger model becomes more effective, it replaces the first model and a new challenger is created.

Better Customer Recommendations

Beyond more personalized customer communication, AI provides the ability to have improve customer recommendations and advice. Mobile banking apps like Moven and Simple let users track their spending and increase their savings with automated, personalized recommendations via a specialized debit card linked with their smartphone app.

Brett King, CEO of Moven believes AI will take over many routine tasks associated with product recommendations and advice. He told Narrative Science, “For me, advice is the next big disruption. For instance, in banking you do need real-time advice. The ability of humans to provide that is poor and, as humans, we’re inconsistent and we make mistakes. Artificial intelligence will not.”

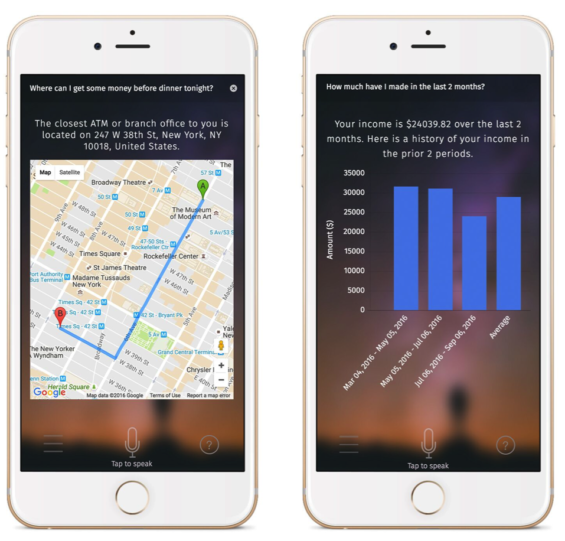

Finie: The AI App for Your Bank Account

As is the case for several innovations in banking over the past several years, one of the most exciting applications of AI in retail banking has come from a small start-up … not from a large national bank. Ann Arbor-based Clinc has created a voice-powered AI platform, named Finie (for financial genie) as a way to interact with a banking account using natural language queries (as opposed to a very limited set of rule-based commands).

Being marketed directly to banks and credit unions, Finie provides the benefits of the best AI, expanding knowledge and improving results with every interaction. Instead of being limited to a command such as, “What is my balance”, Clinc’s Finie can be asked, “Do I have enough money to go out to dinner tonight.” Instead of, “Provide list of transactions”, Finie can be asked, “How much did I spend on groceries” or “Did I spend more on coffee this month than last.”

Finie is integrated within a banks’ mobile banking application, acting as “a voice-activated intelligent personal assistant that is able to answer financial questions unique to each individual user, offer personalised spending advice, and fulfil any banking task”. Without a limited template of basic questions or tasks, it is believed consumers will become more engaged.

The Future of AI in Banking

With an origin rooted in risk and fraud detection and cost reduction, AI is increasingly important for financial services firms to be competitive. The digital consumer is being trained by firms that are becoming masters of AI (Amazon, Google, Facebook and Apple) and expect the companies they use to know them, understand them and reward them through personalized communication.

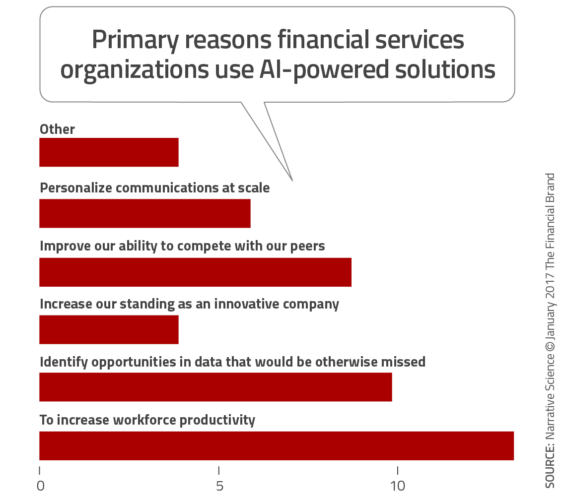

According to Narrative Science,, roughly 10% of the organizations are using AI to compete with peers and identify opportunities in their data that would otherwise be missed. This is just the tip of the iceberg. Soon, all financial services firms will leverage the power of AI to deliver better experiences, lower costs, reduce risks and increase revenues.