There is no doubt trust and honesty are more important than ever in financial services, and a new survey confirms that it can be difficult for companies to regain it once they break that trust. But the most striking finding of Morning Consult’s 2022 Most Trusted Brands Report is that a bad customer experience is by far the leading reason consumers would stop using a financial services provider.

The message is clear: As banks and credit unions strive to enhance their brand, they must put customer experience at the forefront, without diminishing focus on quality products and data privacy. All three are key trust factors.

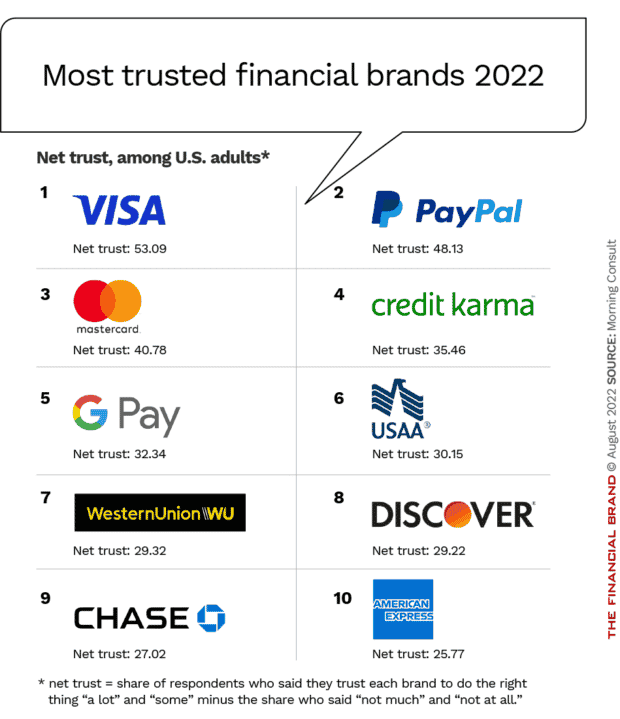

That’s a tall order, but reflects the new demands consumers place not only on banks but the full range of financial services providers to deliver reliable and standout everyday experiences. Of the top ten financial brands ranked by Morning Consult on the basis of net trust, only two were banks.

Key Point:

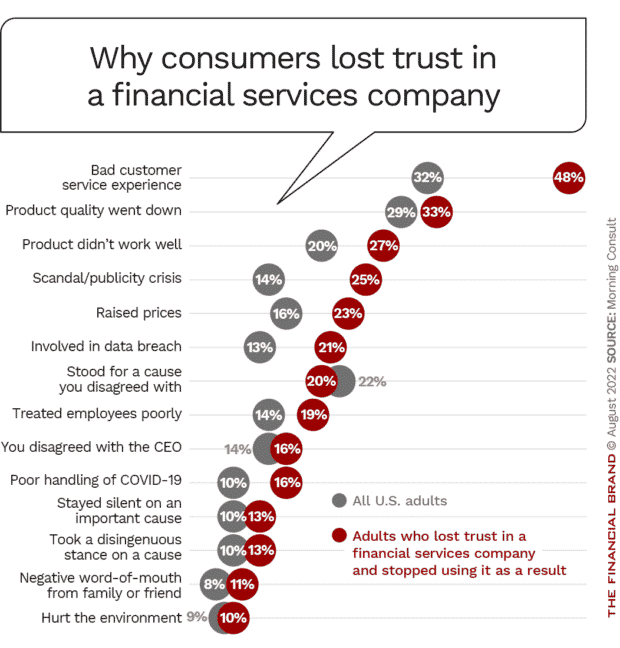

Half of those who lost trust in a financial services company said it was because of a bad experience.

Banks Must Clear a High Bar in 3 Key Areas

The importance of an exceptional customer experience in banking should not overshadow the importance of trust, honesty and data privacy.

Morning Consult surveyed thousands of consumers across the globe on more than 4,000 brands to learn more about what they think and how they perceive companies and their products. Morning Consult released several industry breakout reports, including one on banking, investment, and payments.

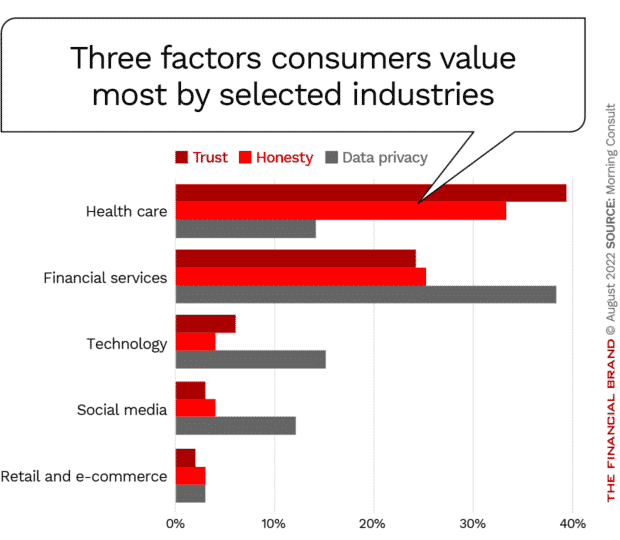

That report identified two major themes. First, trust and data privacy remain pillars of the financial services relationship and matter more than in any other industry except healthcare. Additionally, 53% of those who bank mostly online say that data privacy matters most in their financial services relationships, more than they noted in any other industry.

“Data privacy is most important to consumers in their financial services relationships, and this is true across all generations,” said Charlotte Principato, financial services analyst at Morning Consult, during a webinar on the survey results. “It’s an important opportunity for differentiation and marketing that is frankly being left on the table by a lot of financial services providers.”

Read More: The Top 10 Most Valuable U.S. Banking Brands in 2022

Lost Trust Is Tough to Regain

Many banks and credit unions may take consumers’ trust for granted and could be doing more to demonstrate that trust in their brand. A 2021 survey by Ernst & Young revealed that fintech firms are more trusted than legacy financial institutions across almost all age segments.

In fact, Morning Consult’s survey revealed there are high stakes for financial brands, as 29% of consumers said they would never use a financial services company again if they broke their trust, the highest percentage of the nine industries studied. Further, while 31% of consumers said they would consider returning to a food and beverage provider after a breach of trust (think Chipotle), only 17% would return to a financial services provider. These sentiments are consistent across all demographics and generations, Principato noted.

Read More: The Future of Loyalty in Banking is at Risk

Digital Redefines Trust in Banking

In today’s complex world, trust is a broad-based concept. While many financial institutions may feel pressured to think about social issues and other environmental — or “ESG” — policies, the biggest threats to customer relationships and trust come from the basics of customer service and quality of service.

When most banking was done in person, success was easier to measure and achieve. In the current environment in which the branch visits are much fewer and interactions mainly digital, the challenge is far greater.

As shown above, nearly half of consumers who lost trust in a financial services company said it was because of a bad experience. That’s significantly above the one third attributing loss of trust to declining product quality and the 25% pointing to a scandal as the reason.

Read More:

- Keeping Your Bank’s Brand Out of The ‘Cancel Culture’ Crosshairs

- Why Strong Visual Branding and Communication Are Vital in Banking

- Can Your Brand Become the Nike of Banking?

Why Payments Companies Have an Edge

This emphasis on good customer service has worked to the benefit of payment companies over banks in the past few financial brand studies conducted by Morning Consult. Principato attributes payment companies’ vast distribution, scale and frequent touchpoints with customers as a primary advantage in building trust.

Their high ranking emphasizes the importance of digital interactions as these brands don’t have physical locations. “It’s proof that trust in financial services companies are not built on in-person or even personal relationships with employees but instead reliability, consistency of interactions, even if they are digital,” said Principato.

Only two bank brands, USAA and Chase, made the top ten list. Morning Consult analysts attribute the absence of other bank brands to consumers’ high expectations for their banks specifically and the difficulty these institutions face in building and maintaining strong trust.

As consumer trust is directly correlated with ubiquity and regular use, fintech and digital wallet providers are a “very real threat to the role of traditional banking providers,” said Principato. The ability to add digital IDs, cards, investments and cryptocurrencies to new “super wallets” like Apple Pay, Google Pay and Cash App is a trend that could diminish banks’ roles significantly.