During the Do it Yourself (DIY) years, brands thought they could train us to do everything ourselves. That was frustrating at times, as it turned out we often needed more skills than we possessed. Today, instead of multitasking, Millennials, Boomers and Gen Xers are striking back and want a better customer experience. They want things to be done for them (DIFM), while they focus on more important things such as enjoying life. The new wave of tech apps discovered this change a few years ago and now they’re wildly successful.

Why Do it Yourself (DIY) Has Lost Its Appeal

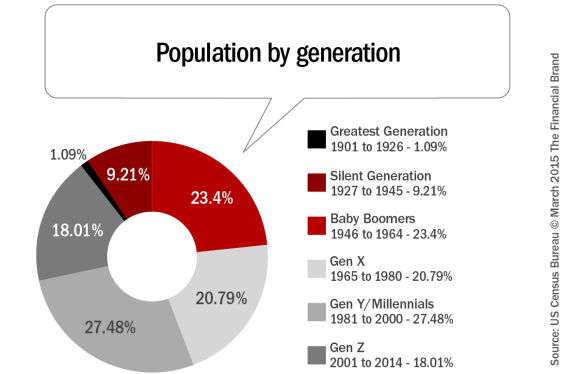

Raised by The Greatest Generation, who fought in World War II and lived through the Great Depression, Baby Boomers wanted to live the American Dream. They leveraged new technology that did work for them and looked forward to the George Jetson future when they could push one button and have all of their work done for them.

Then came the Gen Xers … the technology generation. The DIY culture was a temporary phenomenon, created for them by the early “information age” of the Internet. In fact, their revolutionary DIY drive is the root of today’s major software innovations like Web search.

But those innovations are fading, and have given way to a new Internet generation of increased application power that does the work for us. As Neil Howe writes in a Forbes article titled Generation X: Once Xtreme, Now Exhausted, “more Gen Xers are prioritizing time with their families over longer hours at the office. They see traditional full-time positions as a burden rather than a benefit.” This could also mean the Xers, the DIY generation itself, are ready to “get corrupted” by the convenience of DIFM.

Last, but definitely not least, Millennials … the multimedia, always-connected generation. They have the YOLO (“You Only Live Once”) dream, embracing nowness rather than planning for the future. Adulthood for them means increasing unemployment rates and finding ways to cover massive educational loan debts.

It’s no wonder that long-term investments, such as buying a home, are no longer a priority for this generation. Moreover, they have an aversion to owning real estate, while they value mobility and connectivity.

Why spend time building DIY skills, when you can have apps, services or people that do things for you, while you enjoy spending time doing what truly matters to you (traveling with family or friends, making long-lasting memories).

DIFM Takes Over … Again

DIFM skipped a generation (Gen X) due to Internet limitations. But now that the Internet has expanded in capability, Do It For Me (DIFM) is back in full force. All three generations are under the same DIFM roof.

Fact: We always wanted others to do the job for us. That was the building block of customer service. The information age of the Internet destroyed personal customer service and created a generation of DIY apps and customers.

Over the last 15 years, we’ve been witnessing interesting demographic shifts. Lack of DIY skills, laziness, busyness or high income is slowly driving the DIY paradigm to extinction (predicted to occur by 2050). DIFM is winning more ground as we speak.

The Internet long passed the information age. We’ve entered the digital “application age”, where consumers expect customer service again. In today’s user-centric economy, customer service is a 24/7/365 tool powered by always connected devices. It has to be convenient, interactive, compelling, personal, live AND remote.

Adios, Monolithic APPzillas!

Multi-tasking, Multi-screening, Multi-everything are all fading away. Studies prove they weren’t as productive as we thought. So now large, monolithic apps are successfully being replaced by simple one-tap apps. We’ve entered the ‘One Tap Era’, allowing consumers to plan a holiday, get favorite movies or create personalized icons … all with one tap. Everything is contextual, intuitive, quick and usually costs no more than $0.99. Quite a bargain!

Multi-tasking, Multi-screening, Multi-everything are all fading away. Studies prove they weren’t as productive as we thought. So now large, monolithic apps are successfully being replaced by simple one-tap apps. We’ve entered the ‘One Tap Era’, allowing consumers to plan a holiday, get favorite movies or create personalized icons … all with one tap. Everything is contextual, intuitive, quick and usually costs no more than $0.99. Quite a bargain!

As for customer service, people prefer live face-to-face communication – a warm smile, a personalized greeting and a friendly voice. This could’ve never have happened in the multitasking environment.

Consumers want things done their own way, for free (or inexpensively) and they want it NOW. Tech startups already know this and they’re ruling the world. Connected devices are expected to reach 50 billion by 2020 and among Forrester’s Top Trends for Customer Service in 2015, we find that customers will continue to explore effortless personal interactions with customer service representatives via mobile channels, such as video chat with screen sharing and annotation.

Amazon responded quickly with their ‘Mayday’ button which connects Kindle Fire HDX tablet owners to an Amazon customer service representative via webcam. 75% of customer service interactions initiated by tablet owners now come via the magic button. Increasing personalized user experiences and high-quality customer service define the fresh DIFM approach.

Another example comes from Fiat Live Store, the Brazilian online platform which enables webcam-enabled car browsing. The award winning innovation allows clients to connect with staff at showrooms. Via head-mounted cameras worn by Fiat staff, prospective customers can then virtually explore cars, ask questions and talk purchasing options in real-time.

From Automated Machines to One Tap Banking

Banking is another victim of DIY, struggling to get back customer loyalty. For the past decade, bankers thought that automated digital banking was in their clients’ best interest AND that by firing their best people they would reduce costs.

It turns out it wasn’t that simple, especially when financial literacy surveys show that 73 % of adults agree and 20% strongly agree that they could benefit from advice and answers to everyday financial questions from a professional (source: The 2014 Financial Literacy Survey). According to the Accenture 2014 Digital Banking Survey, “56% of Millennials are interested in having a video chat with a bank representative by accessing a link on their bank’s website, mobile or tablet application.”

Bank customers were not interested in DIY apps, except to check balances. They are interested in the convenience of banking at any time and not having to go to the branch. Until now, DIY was their only alternative. If they could have the convenience of remote banking AND also the personal assistance they need, it would disrupt the traditional digital banking paradigm.

From the automated technology of the 80s, to the 90s and 2000s’ online platforms, banking has become increasingly depersonalized, powered by the Internet and handheld devices. In 2014, customer service was the top reason for switching banks, according to J.D. Power U.S. Retail Banking Satisfaction Study.

And we’re not talking about answering machines, we’re talking about customized conversations with a real banker. It’s time banks make up for the 20 years of DIY digital banking and the loss of customer loyalty.

The new era of DIFM digital banking has arrived. The conversation between banks and their customers is back on, and you don’t even have to visit your local branch. By browsing experts’ choices such as American Banker’s Top 10 Tech Companies to Watch, we know the industry is about to start recovering peoples’ trust and put the Customer-to-Banker relationship into the digital banking process.

Bill Sarris is a recognized expert in the field of streaming and collaborative technology and the inventor of Linqto technology. Bill has delivered major enterprise software applications for Microsoft, Intuit, Digital Insight, NCR, Google, Stanford and other clients. With over a decade of experience in financial services applications, digital and mobile banking, Bill’s work has received the Forrester Groundswell Award and he holds numerous software certifications.

Bill Sarris is a recognized expert in the field of streaming and collaborative technology and the inventor of Linqto technology. Bill has delivered major enterprise software applications for Microsoft, Intuit, Digital Insight, NCR, Google, Stanford and other clients. With over a decade of experience in financial services applications, digital and mobile banking, Bill’s work has received the Forrester Groundswell Award and he holds numerous software certifications.