Credit unions have always enjoyed higher customer engagement than their competitors. Because they don’t have to be concerned with pleasing Wall Street, these financial institutions can spend more time listening to the people they serve — “members” in credit union terminology — and prioritize being helpful to them above all else.

This type of customer focus pays off. In a recent banking study, Gallup found that 73% of members who felt their credit union cared for their financial well-being were “engaged,” meaning they had a rational, emotional, and psychological attachment to the brand. Among those who did not feel their credit union cared for their financial well-being, only 20% were engaged.

With higher engagement, credit unions see some tangible gains. Engaged members buy more products, stay longer with the credit union, and are more likely to consider it their primary financial institution.

But has this advantage run its course?

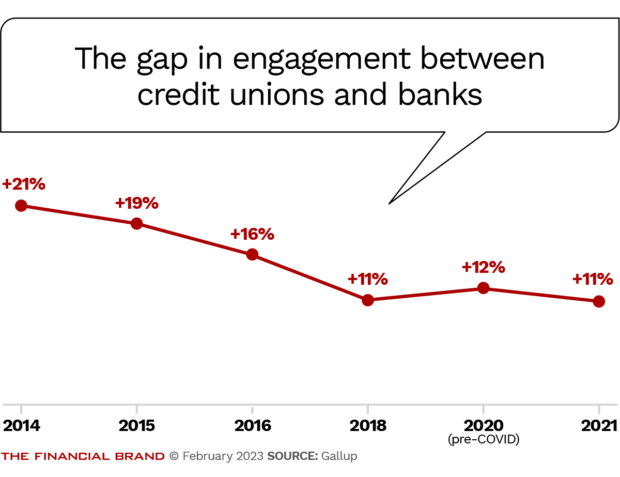

For years, Gallup has researched the advantage in customer engagement that credit unions have had over banks. In 2014, credit unions had a +21% engagement premium and a +29% premium in their net promoter score, or NPS. By 2021, credit unions’ engagement premium had almost halved, to +11%, and the NPS premium had shrunk to just +17%.

Troubling Trends: Fewer Credit Unions, Aging Members

The drop-off comes as credit unions undergo significant changes.

For one, the number of credit unions is shrinking as the smaller ones merge with others to gain the efficiency that comes with scale. In fact, the number of credit unions with fewer than $10 million in assets plummeted by two-thirds in the past 10 years, from nearly 3,000 to just over 1,000. This has led to increased competition and lower differentiation overall.

There is also a significant demographic shift occurring in the member base for most credit unions. According to the World Council of Credit Unions, the average age of credit union members in North America is 53 — which is older than the average for the general population. That’s not a statistic that bodes well for credit unions.

A Demographic Cliff:

The average age of credit union members in North America:53

The overall median age of people in the United States is 38.5, and trending downward. According to the latest Census Bureau statistics, millennials and younger generations are now half of the U.S. population. Gallup research shows that millennials are the least engaged with their credit unions among all generational groups — their 27% compares with 34% for Gen X, 38% for boomers, and 46% for the Silent Generation (75 years and over).

With these headwinds, how can credit unions keep building on their strengths and further capitalize on the engagement premium they have enjoyed for so long? Our work with credit unions across the country suggests three strategies.

Strategy #1: Focus on Financial Well-Being

Financial well-being is where credit unions shine, but they have challengers. Banks seem to be doubling down on financial well-being as a core strategy, to the point that many are beginning to resemble credit unions in how they talk about their service, customer orientation, and brand. Fintechs and neobanks are joining the bandwagon as well, promising people more control over their finances through new technology, digital tools and self-help options.

Even so, a true focus on financial well-being is how credit unions can keep meeting their purpose of serving members. The key is for credit unions to clearly define their financial well-being strategy.

Gallup characterizes well-being as “managing one’s economic life to reduce stress and increase security” — in short, ensuring one’s emotional relationship with money is healthy. Painting an accurate picture of “hope” and “worry” serve as guideposts for financial well-being, and members’ progress can be measured in a way that traditional financial health metrics, frequently offered by banks and fintechs, do not.

Metrics built around members’ relationship with money should be prioritized and tracked to show each member’s progress over time. Beyond measurement, credit unions have a real opportunity to highlight stories of creating member financial well-being — which builds an organizational culture that focuses on well-being rather than financial transactions.

A commonly expressed challenge for credit unions that affects both member and employee engagement is a need for greater cooperation among different departments. Addressing this challenge is a must, because improving a member’s financial well-being depends on holistic service, which requires a high level of cooperation across the entire organization. Multiple channels (human and digital) and front- and back-office team members must be aligned in their pursuit of member engagement and well-being.

Strategy #2: Bridge the Digital Divide

The pandemic accelerated the banking industry’s adoption of digital, but many credit unions are holding off on the expense and hassle of introducing new technology to see how others fare first. The fact is, credit unions need to adopt new technology faster.

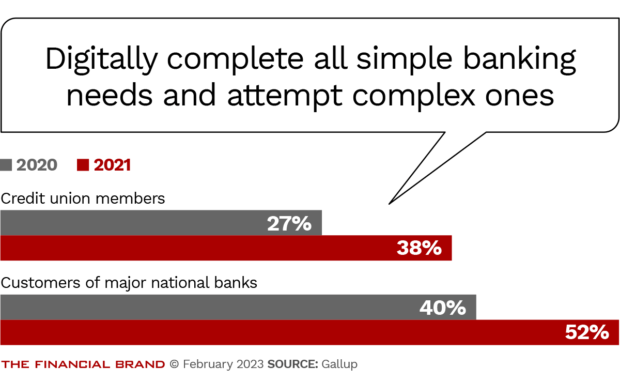

Overall, credit union members are increasingly comparable to bank customers in their reliance on digital solutions. Gallup research shows that in 2021, the proportion of credit union members who were “digital forwards” — people who use digital tools for all their simple banking needs and attempt digital for the most complex ones — was 38% (up from 27% in 2020). Meanwhile, the proportion of digital forwards in 2021 for national banks was 52%, and for large regional banks, 40%. Many of these digital forwards are millennials.

Credit union employees are ideal for educating members about digital bank tools. Indeed, Gallup research shows that human channels are three times more effective in driving digital adoption than any other communication form.

Step-by-step assistance is an effective way to move digital laggards into the digital forward category, but more importantly, that interaction facilitates the financial well-being of members, and leverages credit unions’ unique service and relationship-building strengths.

However, our research also shows that only about one in three members strongly agree their credit union provides digital adoption support and education. One way credit unions could improve on this front is to focus on educating and training employees first. Members are more interested in digital than ever, and credit union employees must stay a step ahead of them to continue being a resource for financial well-being.

Read More:

- Rethink How to Get Branch and Digital Channels to Sync

- How Engaged Employees Improve Customer Experience

- What Do Millennials Want from Financial Institutions?

Strategy #3: Train Employees to be ‘Trusted Advisors’

To genuinely support financial well-being, financial institutions must be able to provide for most of their customers’ needs — today and in the future. Employees also must be trained and empowered to be a true advisor, adept at asking the right questions and getting to the heart of what members need, not just the products available to them.

Financial institutions are doing poorly on that count. Gallup asked people to rate the quality of their typical conversation with employees at their financial institution, from best to worst, as “vital,” “strong,” “inferior” or “poor.” Only 11% of customers of all types of financial institutions say their conversations are “strong.” The most common rating was “poor” (42%). The quality of conversations at credit unions is only a little better: 15% rated it as “vital” and 38% rated it as “inferior.”

Failing in these conversations is akin to fewer at-bats — and many missed opportunities for satisfying member needs. Indeed, many credit union employees might not even know what a good discussion is, which creates variance in conversation quality and extremely spotty member experiences.

Credit unions must train and coach employees on “trusted advisor” behavior, which addresses three core member needs:

- Basic assistance, such as clearly explaining product benefits.

- Holistic focus, such as asking the right questions and demonstrating an interest in the member’s financial well-being.

- Conversations on financial vision, such as helping members see their financial needs differently.

To achieve this, leaders must regularly invest in needs-based conversation coaching. They should also have managers observe employee conversations and offer feedback. Of course, sourcing the right talent with the natural capacity to be a trusted advisor is important as well.

Read More:

- Why the Approach to Financial Wellness Must Change

- Want Growth? Offer Virtual Financial Coaching for Customers

- The Top 5 Customer Experience Trends for 2023 and Beyond

Strategic Advantages Credit Unions Should Capitalize On

The gap in customer engagement between credit unions and their bank counterparts seems to be narrowing. However, credit unions still have a strategic advantage: Members trust them and believe credit unions care about the people they serve, rather than being motivated by profits.

But to compete in the new banking landscape, credit unions will need to drive that differentiation more intentionally. They must understand that financial well-being is emotional, not transactional, and implement strategies addressing this reality. They also should upskill employees in technology, so that they can help members become more digitally adept. Finally, credit unions should lean into their advisor capabilities. Leaders and managers should coach employees in the kinds of conversations members will get value from and find emotionally satisfying.

That approach will help credit unions sustain their customer engagement premium. It will also revitalize the advantage credit unions have that banks don’t: a human-centric mission to serve members, not Wall Street.

About the authors:

Vibhas Ratanjee is senior practice expert and executive advisor on leadership and organizational development at Gallup, the global consulting firm. Dipak Sundaram is Gallup’s executive director for advisory services.