The majority of today’s banking consumers have made the move to digital channels, but that doesn’t necessarily mean they are happy about it. Banks and credit unions continue to fall short of consumer expectations, particularly when it comes to more complex transactions, payments and areas involving personal financial management.

According to a study fielded by Oracle, these shortcomings leave one-third of consumers open to trying a non-bank provider to get what they want. Traditional financial institutions had better figure out how to satisfy consumers in digital channels quickly, because their patience is wearing thin.

In their research, Oracle asked more than 5,000 consumers about their banking preferences and expectations, segmenting responses into five areas: account opening, payments and transfers, personal and lifestyle loans, home loans and mortgages and personal financial management. Findings in their final report shows that today’s banking experience needs to be better integrated into people’s digital lives, providing service that is instant, integrated with social platforms, and — most importantly — driven by data.

69% of consumers want their entire financial lifecycle on digital channels.

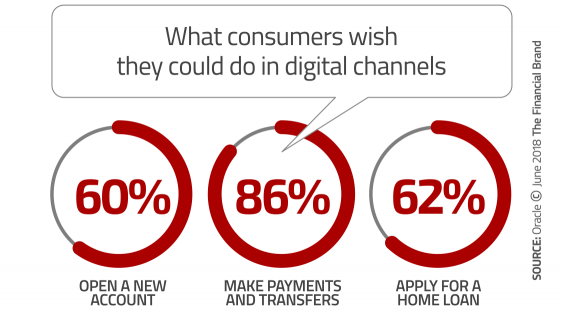

In the study, four out of five respondents said they engage with their financial institution via digital channels at least some of the time, and two-thirds report that they are active online- and mobile bankers. However, 69% of those surveyed said they would like the ability to digitally engage with their bank or credit union for all their financial needs — not just some things, some of the time.

“Unlike their youngest consumers, most retail banking providers don’t have the luxury of being born digital,” Oracle wrote in their report. “For banks and credit unions, making the digital switch has been a long process — and one that hasn’t always served consumer needs in the best ways possible, or have been completed on time.”

Fintechs and Challengers Gaining Ground

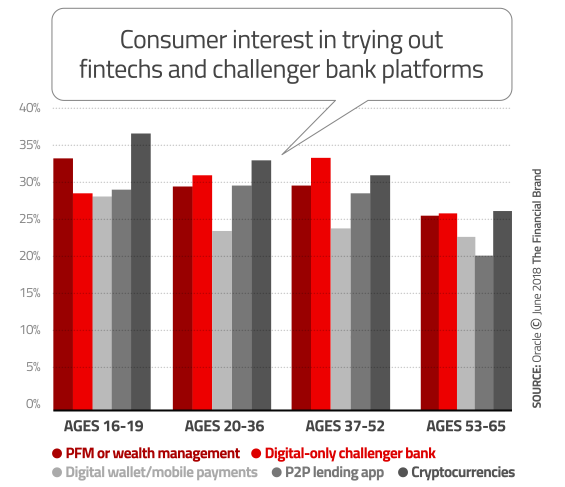

There’s a fair number of consumers who are already engaging with fintechs and digital-only players in the financial space, especially when it comes to digital wallets, mobile payments, personal finance and wealth management apps. In Oracle’s research, more than half of consumers ages 20 to 36 said they already use a digital wallet or mobile payment platform provided by a fintech or challenger bank-provided.

That might not be all that shocking, but what should scare traditional banks and credit unions is the number of consumers who are interested in trying out alternative banking providers and other similar new options.

The danger of course is that consumers will try these products that are likely more innovative and offer a better consumer experience and never go back. And then migrate more and more of their financial life over to fintechs and challenger banks.

“Banks have clearly not been able to keep up with consumer expectations,” says Devie Mohan, a fintech market strategist. “Consumers love digital channels, they just need to be driven there — either by an integrated offering or by a strong marketing channel.

Oracle says that for traditional retail banking providers, the time for change is now. “Challenger banks have never been more compelling for digital consumers, and they are increasingly becoming a popular choice for almost all kinds of banking service, at every stage of the financial lifecycle,” they said in their report.

According to Brett King, Founder and Chairman of Moven and author of Bank 4.0, the fastest growing financial services organizations in the world today are, technology-based providers, not incumbent banks or institutions — challenger brands like Alipay and WeChat in China, M-Pesa in Kenya, Paytm in India, Kakao in Korea, and more.

“The future is pretty clear. In five years’ time, if banks and credit unions aren’t delivering the bulk of their revenues through digital channels, they will be out of business, or in danger of imminent failure.”

— Brett King, Founder and Chairman of Moven

Simplify Banking, Remove Friction and Eliminate Pain Points

The findings in Oracle’s report suggest consumers are restless and growing impatient. When Oracle examined the consumer financial lifecycle, they found that satisfaction scores plunge at critical life moments further down into the stages, with the biggest drops occurring with more complex financial transactions.

“Currently, satisfaction levels are falling for all kinds of banking transactions, and the rise of new digital options has caused many consumers to see banks as a decreasingly relevant part of their digital lives,” wrote Oracle in their report.

What explains these sinking satisfaction scores? Simple: friction in the digital experience.

“There’s a misconception that when consumers say they want banking services to be ‘convenient, they simply mean they want those services to be accessible and fast,” Oracle explains. “While speed and accessibility are important, true convenience often means services are connected together as part of a smart, seamless financial lifecycle.”

This is why Brett King says the banking industry now all boils down to the type of digital experiences financial institutions deliver.

“Technology allows much faster scale on much thinner margins,” King explains. “But it is fundamentally about a key element in the future of customer-centric banking — the removal of friction.”

If banks and credit unions hope to deliver what consumers want when and where they need it — in digital channels and in real-time — King says it will require cultural shifts starting at the very top.

“Digital transformation requires a leadership team that understands technology is at the core of what they do,” King says. “More than that, they must understand ‘the bank’ is no longer a collection of products distributed across channels, but experiences which surface the utility of the bank to a consumer contextually.”

The Digital CX Imperative: Act Now, Before It’s Too Late

“Whichever channels consumers prefer, there’s one thing they all want — connected, seamless, and data-driven experiences across the entire financial lifecycle.”

Oracle says some banks and credit unions are still thinking about and discussing the digital transformation as something that’s “currently happening” or “will happen” in the future.

Reality Check: If you’re still debating your digital transformation journey, you’re too late.

“For many of today’s banks and the services they provide, the shift to digital channels is complete,” explains Gary Pugh, VP/Head of Marketing at Oracle Financial Services Global Business Unit. “But even for banking providers that are already delivering exceptional digital experiences, their broader digital shift is far from over. For banks that have mastered the delivery of basic digital services, the next step is driving digital deeper — and making every experience as simple and intuitive as possible across the customer lifecycle.”

Data will play a critical role in that transformation, helping banks use the information gathered through basic digital services to better understand their consumer, proactively anticipate future needs and build relevance at every stage of the financial lifecycle.

According to Charlotte Petris, co-founder and CEO of Timelio, fintechs wouldn’t have been able to disrupt the banking industry the way they have if traditional institutions did a better job in digital channels.

“The rise of fintechs has been driven by increasing consumer expectations and the faster pace of technological evolution,” Petris says. “Traditional finance companies have left a gap in the market of unmet consumer needs. But with powerful technology companies like Google, Apple and Amazon influencing other parts of consumers’ lives, people now are demanding similar levels of personalized digital interactions from their financial services.”