Today, customer experience has even greater significance for banks and credit unions for the simple reason that consumers have an abundance of choice. Advances in digital technology have lowered the barrier to entry for hundreds of fintech competitors. And while banking customers still don’t easily switch primary institutions, the means to do so is becoming easier all the time.

The day is drawing near when the incumbents’ advantage of an existing customer base, won’t mean as much, especially if the experience they provide is mediocre.

Right now that’s too often the case. Gallup reports that less than two out of five consumers (17%) are extremely satisfied with all the banking channels they use. Lack of consistency across channels — a long-standing bugaboo for traditional institutions — is a big part of this. In addition, nearly half (48%) of consumers say they were unable to open a banking account completely in a digital channel.

The Financial Brand reached out to five customer experience experts and asked them to address key questions related to how financial institutions can provide exceptional customer experiences.

What are the chief roadblocks keeping financial institutions from delivering exceptional experience?

Apropos of the Gallup statistics just mentioned, several respondents pointed to the limitations imposed by legacy technology, and the need to move from siloed systems and data to an omni-channel approach. That way consumers can shift from mobile to contact center to branch smoothly if they choose to — but aren’t forced to because of a channel shortcoming.

Progress is being made here, depending on the institution, but the pace needs to be much quicker now. This improvement isn’t necessarily a budget-busting requirement. Even though the top four banks collectively are spending $38 billion on technology, the cost of processing is trending toward zero, further democratizing technology, says Don MacDonald, CMO of MX. “The most valuable asset financial institutions have is their data,” he adds, “so any institution can work with a variety of vendors to get to market quicker than by building their own technology.”

Another related CX roadblock is friction — unnecessary steps or difficulty in opening an account, for example. Friction is one of the biggest threats to financial institutions today, maintains Deepanjan (Deep) De, Head of Financial Services at Facebook.

“Just as consumers expect paying for shoes online to be easy, they’ll also expect financial activities like paying bills, setting up a mortgage, and trading stocks to be seamless,” says De.

Lack of a proper culture was mentioned as a roadblock to good customer experience by almost all the experts. Andrea Olson, CEO of Pragmadik put it succinctly: “An organizational culture rooted in bureaucracy, silos, hierarchies and resource competition limits employees’ ability to put consumer needs and objectives over their own internal survival.”

“It’s easy to say you care about customer experience, but to actually build an entire culture around this is complex and difficult.”

— Paul Berg, Gallup

The kind of culture Olson describes is a failure of leadership. Paul Berg, Senior Managing Consultant with Gallup observes, “It’s easy to say you care about customer experience, but to actually build an entire culture around this is complex and difficult.”

The Gallup executive has two specific suggestions for improving this situation:

1. Broaden CX scope internally. Banks and credit unions need to expand the responsibility for customer experience beyond customer-facing teams. Other teams including Digital, Marketing, Product, Risk, and even Finance are “mission critical” to CX, says Berg. However, these groups often have unclear and/or misaligned expectations, he adds, which leads to challenges with budgeting, resource allocation and success metrics.

2. More coaching, less managing. Only one in four employees say they receive supervisor feedback helpful to doing their job better, according to Gallup data. “Most financial institutions confuse managing process with coaching,” Berg states. This typically means the focus is on a scorecard — e.g. ‘How many accounts did you open?’ — versus developing individual employees’ strengths and potential.

Read More:

- Digitizing Banking is All About Engagement and CX, Not ‘Tech’

- How Internal Brand Alignment Amplifies CX in Banking

- Open Banking Fintech Partnerships Required For Better CX

How can financial institutions achieve the right CX balance of human and digital?

None of the six respondents advocated for all-digital, all the time. They believe human interaction will always be a part of good customer experience. As a practical matter, consumer preferences are far from uniform at different financial institutions. For some banks and credit unions, as Gallup has found, more than a third of their customer base fall into the category of “digital laggards” — i.e. preferring in-person channels.

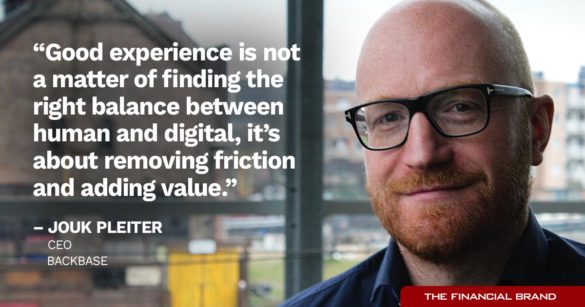

“Good experience is not a matter of finding the right balance between human and digital,” states Jouk Pleiter, CEO and Founder of Backbase, “it’s about removing friction and designing experiences that add value to the customer. It is about solving real problems that people have.” Pleiter believes that digital tools offer a huge potential to solve many kinds of financial problems, and is what consumers expect now. “But people still want to interact with people, and that shouldn’t be a point of friction in the process. It should be a valuable added step.”

As Gallup’s Paul Berg puts it, “Digital should allow people to be ‘more human’.” He points out that behavioral economics teaches that people make decisions about 30% rationally and 70% emotionally. “In order to create engaged customers,” he believes, “it’s highly likely that you’ll need humans in some capacity to capture that 70% emotional space.”

One reason why digital solutions and human interactions seldom mesh seamlessly, Olson observes, is because digital investments too often are based on what’s most cost-effective, and digital transactions are much less costly than teller transactions. Instead, the guideline should be what she calls, “experience impact,” not cost effectiveness only.

How can data improve customer experience?

“Data is the great creator of experiences,” Don MacDonald states emphatically, “it enables banks and credit unions to be Amazon rather than Sears.” The MX CMO cites three examples of how data allows a financial institution to define the appropriate experiences for each consumer:

- Data allows you to identify what loans you could provide that are currently being provided by someone else.

- Data allows you avoid wasting dollars and pixels making offers that are not relevant for a particular customer.

- The right data — i.e. properly “cleansed” — enables a financial institution to send out fraud alerts that are useful, instead of confusing and frustrating. For example: “Did you use your card at a Chevron gas station?” versus the all-too-common “Did you use your card at CSI-264/38654”?

Facebook’s Deepanjan De points out that data drives personalization and today’s consumers expect a personalized experience from brands. In 2019 research Facebook found that 43% of checking account consumers aged 18–34 say are more likely to buy from a business that offers personalized recommendations.

While vital for financial institutions to master, “data” too often is tossed around as the answer to all ills. Andrea Olson offers a cautionary note.

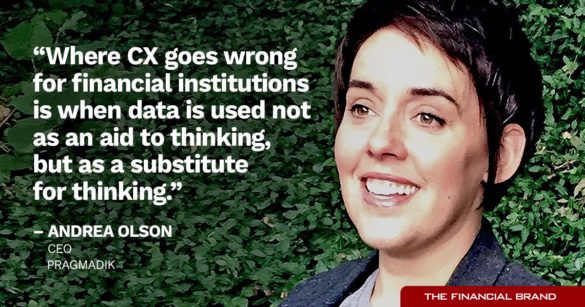

“Where CX goes wrong for financial institutions,” Olson states, “is when data is used not as an aid to thinking, but as a substitute for thinking. There’s a strong tendency in finance to favor arguments based on numbers.”

Institutions that want to effectively use data to improve CX, Olson continues, first need to define consumer objectives, both rational and emotional. Second, they should use data to uncover the most effective ways to consistently achieve those objectives.

Gallup’s Paul Berg observes that data can and should illuminate “systemic, structural or operational issues” that hurt customer experience. For example, if the mortgage division is regularly missing expected closing dates, CX data can help identify where the breakdown is occurring — perhaps with improper expectations set by the loan officer. Or, perhaps the cause is multiple requests for the same documents, which can be a technology issue or a communication issue.

Read More: 16 Must-Have Mobile Banking Features that Raise the CX Bar

What are the best metrics of CX success for financial institutions?

Two themes emerged here: 1. the need for CX metrics to be meaningful, i.e. have real impact on the bottom line, and 2. the importance of having metrics address specific issues.

Berg says Gallup believes “engagement” is the “right north star” for financial institutions. Engagement, which the firm defines as the emotional connection between customers and an institution, is a higher bar, than Net Promoter Score or overall satisfaction, Berg states.

“Immediate, no-BS experience metrics include mobile app ratings and engagement. If you have less than four stars or less than 25% engagement, start worrying.”

— Don MacDonald, MX

“Satisfaction metrics are only truly valuable to shaping the consumer experience when they are tied directly to consumer objectives,” Olson states. “Most financial institution metrics are designed to measure internal performance.” She urges institutions to shift from lagging/passive indicators, such as the “how did we do?”, to engagement/active indicators that capture consumer perspectives and experiences in real-time.

MX’s Don MacDonald puts it a little more bluntly: “Immediate, no-BS experience metrics include mobile app ratings and engagement metrics. If you have less than four stars or less than 25% engagement, start worrying.” He says that building metrics into the various parts of mobile apps allows the institution to see where users abandon and where they succeed.

Read More:

- Best Customer Experience in Banking Blends Digital with Human Touch

- Digital Start-Up’s Branch Sends CX Message to Retail Bankers

What one factor relating to customer experience should banks and credit unions focus on in the year ahead?

Eliminate friction. Every extra step or delay is a reason for a consumer to go to your competitors. Discovering and browsing your products should be easy and stress free. Think about your process for opening an account or getting a quote — can steps be simplified or eliminated? — Deepanjan De

Raise your sights. Behind all the CX data are people. People with expectations that the technology from their financial institution will be as helpful as the technology in their car or shopping experience. Good CX is not just a comparison to other financial institutions anymore but a comparison with Amazon, Tesla and Spotify. — Don MacDonald

Get emotional. With the continued expansion in digital technologies, deliverables such as a mobile banking app’s ease of use become the baseline expectation. Institutions need to design engagement strategies around growing consumers’ emotional satisfaction. Emotional Satisfaction is one of the biggest, untapped opportunities for financial institutions to create a differentiating consumer experience. — Andrea Olson

Focus on culture with tech. Most financial institutions focus on designing and launching digital offerings, as they should, but don’t understand or plan for all the cultural implications. The result is that only about 2% of institutions are fully monetizing the opportunity that exceptional CX creates. — Paul Berg

People over products. Banks and credit unions need to research, test and validate how they can best become part of people’s daily financial lives. Just as your phone helps you order tickets or decide what to eat, it should help you easily manage your finances. Like a friend, it should help you and make suggestions, but only when it’s relevant. — Jouk Pleiter