Banking is one of the oldest, largest, and most important of our industries, with most adults having some form of relationship with one or several banking organizations. While transforming over time, the industry’s basic purpose has not changed. Banking’s role is to make loans and protect depositors’ money. Even if the future takes banks completely off the street corner, these needs must be served in some manner … by some entity.

But, traditional functions are being contested or commoditized, and emerging competitors are replicating banking functions better and at lower cost. How can traditional banking organizations retain the customer relationships they have built over time?

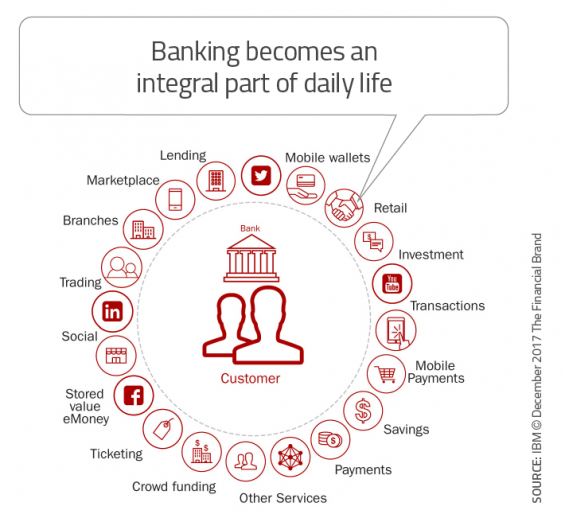

A very viable option is to reposition banks as the principal gatekeeper to their customers, creating an ever-evolving ecosystem of services and experiences provided internally and externally for the benefit of customers.

This is the conclusion of a global banking and consumer study by the IBM Institute for Business Value. By retaining the foundations of a strong customer experience, today’s banks can be the best option for many consumers.

Unfortunately, the banking industry isn’t doing as well as we think when it comes to customer trust, loyalty and creating a personalized banking experience. In fact, there are serious gaps between how banking executives believe they are doing, and how their customers really feel. This can negatively impact the ability to be the gatekeeper of financial services in the future for many organizations.

Customer Experience Perception Gap

The IBM study found that while banks can satisfy the most basic customer demands, banking executives are far too optimistic as to how well they meet their these basic consumer needs today. While 62% of retail banking executives indicate their organizations are able to deliver an excellent customer experience, only 35% of retail customers share this view … a 27% gap!

For wealth management, the gap was even greater, at 41 percentage points. Fifty-seven percent of wealth-management executives believe they provide an excellent experience, while only 16% of wealth-management customers agreed.

While banking did better than bankers anticipated on capabilities like timelines and consistency, the industry falls short in the key areas of creating a personalized customer experience across interactions (45% for bankers, 30% for customers), and encouraging customer loyalty (48% for bankers and 35% for customers).

Customer trust is also overestimated by banking executives surveyed. As many as 96% of bankers believe their customers trust them more than other non-bank competitors, while only 70% of customers agree. Fewer still (67% of customers) trust their primary bank compared to other bank competitors.

Unique Opportunity for Enhanced Customer Experiences

These survey results could present challenges for the banking industry as it becomes increasingly dependent on customer loyalty to compete. Alternatively, bankers can work to position their organizations at the center of rapidly evolving banking ecosystems. While fintechs are able to leverage new technologies to compete against banks in specific functional activities, they do not yet have the benefit of banks’ customer relationships.

“This is a wake-up call for banks faced with increasing competition. As other industry players including financial technology firms, mobile payments companies and startups begin to replicate banking functions, traditional banks will be forced to find new ways to differentiate themselves,” said the study. “For banks that recognize early on that the value is shifting away from banking services to the deep customer relationships they have carefully built over decades, this could be a time of opportunity as bank ecosystems shift dramatically.”

The IBM research believes that banks have an opportunity to position themselves at the epicenter of evolving ecosystems, offering a broad range of best-in-class services for the benefit of their customers. By offering these new and existing services under one roof (or as part of one app), banking organizations can retain customer loyalty through lower costs and a wider selection. Relieved of the burden of offering the services themselves, banks and credit unions could focus more heavily on enhancing the customer experience … reducing the experience gap.

An interesting side benefit is that infrastructure costs could fall as fewer services are offered. Instead, there will be a greater focus on pass-through commissions or markups, allowing margins to increase. The ‘value add’ will be the ability to leverage contextual insights across products to provide highly personalized solutions for consumers.

Five Capabilities Needed for the Future

The survey of banking executives identified five key capabilities required to accelerate the transformation required to be the financial services gatekeeper.

Partnering and Collaboration – To be positioned at the center of the customers’ financial ecosystem, banking organizations will need to be able to partner and collaborate with new fintech players. Forty-five percent of global banking executives believe that partnerships and alliances improve their banks’ competitiveness.

Agility – Traditional banks will need to have agility similar to the new fintech start-ups. Only 21% of global banking executives believe their organizations have above-average agility compared to fintech peers, reflecting a gap in capabilities.

Innovation – Simplified business processes and openness were thought to enhance and speed up innovation processes. The survey indicated that 48% of bankers thought social media will help them innovate in products and services.

Analytics – Actionable insights would allow for personalized interactions and transform customer relationships. Forty-eight percent of bankers say investment in predictive analytics is a key priority.

Digitalization – It was believed that digitalization was imperative for a next generation bank. As a result, 52% of global banking executives say that investment in mobile technologies is a key priority.

Digital Readiness of Banking Organizations

The IBM study found mobile to be a core component of enhanced customer experience in the future. Eighty percent believe their banking mobile apps are user friendly and 86% believe they are easy to use. Bankers and customers both agreed on the growing importance of mobile banking, yet only 10% of banking executives believe the majority of transactions will be conducted through mobile devices in the future. Conversely, 41% of customers expect their transactions to be conducted on a device in the next three years.

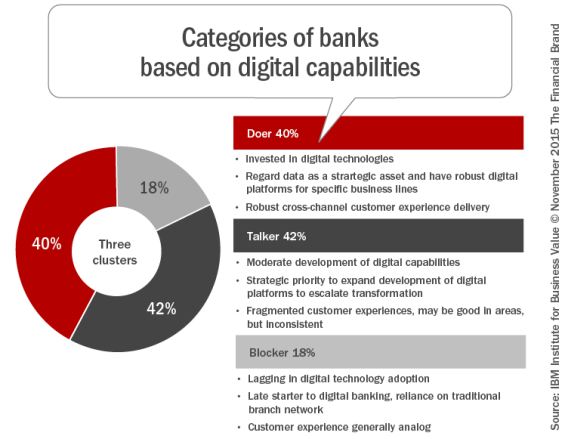

There is obviously a difference in the readiness of some banking organizations for the digital future and the related capability to be at the center of a consumers’ financial life. To analyze the readiness for transformation, IBM conducted a cluster analysis based on data from the more than 1,000 banking executives surveyed.

Three clusters were identified based on the degree of readiness. ‘Doer banks’ were the most prepared based on both revenue growth and operating efficiency. These organizations (40% of the total) face fewer barriers to providing compelling and consistent customer experiences. Doers are 39% more likely to have customers who believe their assets and information are safe, 17% better in managing risk compared to non-traditional competitors and 12% better at managing risk effectively across all businesses and functions.

‘Talker banks’ (42% of the total) were moving down the path of digital transformation and had made digital platforms a strategic priority. While the customer experiences were not as positive as the ‘doer banks’, progress was being made. The final category, ‘blocker banks’, represented 18% of the total and were lagging in both digital adoption and customer experience. These organizations had a greater reliance on branch systems and are falling farther behind as other organizations move forward.

Options for the Future

As fintech start-ups and innovative banking organizations replicate traditional banking functions with less friction and at lower cost, financial services organizations have three options.

- They can do nothing and wait for the marketplace to overtake their organization

- They can try to compete in low-margin services, being relegated to a processor role

- They can leverage the benefit of current customer relationships and build a powerful ecosystem as the relationship gatekeeper

“Traditional concepts of what a bank does will change fundamentally and permanently,” said Likhit Wagle, IBM Global Industry Leader for Banking & Financial Markets. “Bankers will no longer be bankers in the traditional sense. The most successful banks will be focused on collaboration, agility, innovation, analytics and above all on going beyond digital and transforming into becoming a Cognitive Bank.”

Leveraging the deep relationships traditional banking organizations have with customers that will allow banks and credit unions to position themselves as the principal gatekeeper to their customers, creating an ecosystem of even better services and experiences. Most importantly, this strategy can be implemented regardless of size or organizational structure.