Central banks, as a general rule, act as a check on over-exuberant financial disruption. They don’t do the disrupting themselves.

Yet if the Federal Reserve joins with several of its counterparts around the world in creating a “central bank digital currency” (CBDC), the impact on traditional institutions — particularly in regard to payments — could be as disruptive as anything seen so far.

Is that likely? By one measure, no.

In a speech by Fed Governor Christopher Waller, notably titled “CBDC: A Solution in Search of a Problem?,” he said that “the first order of business is to ask whether there is compelling need for the Fed to create a digital currency. I am highly skeptical.”

However, bankers and credit union executives would be wrong to let such skepticism lead them to ignore what’s brewing on the CBDC front. The situation globally and especially in the U.S. is extremely fluid, and there are concepts in the mix that could undermine the role of traditional institutions.

“It is evident that the evolution of CBDCs will have profound ripple effects for the whole financial ecosystem,” states a white paper from Deloitte, “Central Bank Digital Currencies: The Next Disruptor.”

The Fed has been in wait and see mode while a joint paper is pending from the Boston Federal Reserve Bank and the Digital Currency Initiative at Massachusetts Institute of Technology. The paper is intended to set some direction, not to decide the issue.

Those looking for fast moves on CBDCs in the U.S. after the report drops have a mix of exuberance and anxiety. There are concerns that the U.S. can’t hold off the “ripple effects” of other countries’ CBDC activities while it gets things just so. While some of the most mature CBDC efforts are in small markets — like the Sand Dollar of the Central Bank of the Bahamas and the DCash of the Eastern Caribbean Central Bank — that is far overshadowed by the pilot project of the People’s Bank of China. Tens of millions of transactions have gone through China’s CBDC, the digital renminbi, during its pilot phase and it is moving into the production phase now, according to Richard Walker, Principal at Deloitte Consulting LLP.

CBDCs = Major Economic Change:

Some might say there’s a sort of economic “FOMO” — fear of missing out — on some level. But that trivializes things, because some bigger issues are at stake.

One of the biggest impacts of CBDCs is the future role of the U.S. dollar on the world stage. An article appearing on the website of the Carnegie Endowment for World Peace states that:

“Beijing is likely to leverage frustrations with the inefficiencies of existing cross-border payments channels to strengthen support for its vision of lower-cost alternatives built upon CBDCs. If realized, such arrangements could allow Chinese firms and their trading partners to reduce usage of the U.S. dollar for cross-border transactions and circumvent payments channels that the U.S. government can shut off to entities it sanctions for national security reasons.”

More broadly, there’s a sense that the financial tide favors development of CBDCs for the U.S. and other major nations.

“I believe there’s recognition in the market that CBDCs are an eventuality,” says Walker in an interview with The Financial Brand. But there are a lot of uncertainties about exactly how they will be structured, what their characteristics will be, and when they will be delivered. There’s a lot of exploration going on, many organizations doing research and looking at various scenarios for how CBDCs will be put into place.”

What’s At Stake for the Banking Industry

Walker describes a kind of financial “creative tension” building up over what a U.S. CBDC would look and function like.

“There’s a high degree of sensitivity among the central bankers in developed countries, and the U.S. in particular to not disrupt a well-functioning banking system by taking on some of the roles that banks provide,” Walker says.

As he explains it, what a CBDC will be, how it will work, and the place it will take in an economy will vary from country to country. Walker also says that multiple forms of a CBDC could exist in a country simultaneously, depending on what they are trying to accomplish.

Cryptocurrency in general has been in a continuing state of ferment, with Walker noting that there are actually over 9,000 cryptocurrencies out there already, some of them created for highly specialized purposes. The CBDC discussion is sitting in a giant vat of potential financial change.

A quote from Deloitte’s paper, “Central Bank Digital Currencies: Regulatory and Policy Considerations in the U.S.” helps clarify the role of CBDCs:

“The main difference between CBDCs and other digital assets (such as stablecoins or Bitcoin) is that a CBDC is a direct claim on the Federal Reserve, and the others are not. Bitcoin (and other cryptocurrencies like Ethereum) is effectively a digital asset and is usually bought and sold as such. Stablecoins, while pegged to a central bank currency and backed by holdings denominated in that currency, are not a direct claim on the Federal Reserve and would still require an intermediary to support.”

— Deloitte report

The private banking system in the U.S. stopped issuing its own currency more than 100 years ago, but commercial banks do “make” money in the process of issuing loans as a multiple of deposits. “U.S. policy discussions often highlight that a CBDC should not disrupt the role that banks play in capital creation and liquidity,” Deloitte states.

Read More: Are Cryptocurrencies Coming to Everybody’s Checking Accounts?

Understanding the Present to Comprehend the Future

Transactions using CBDCs would go beyond the digital transactions we have today.

“Digital money moving electronically, as we’ve had for decades, is really a payment instruction of sorts that is processed according to the payment system used, whether it is the automated clearinghouse or wires,” explains Walker. “The settlement of the actual payment happens sometime later. It may feel real time, but ACH settles two to three days later and that’s when the recipient actually has access to the funds. A wire receipt happens more quickly, but it is still a matter of several hours.”

Beyond that, with instruments like credit cards there are risks involved which are solved through fees charged for running the card networks.

Digital assets like CBDCs are a different creature. “You have the potential to move the actual money right away from one wallet to another,” Walker explains. “And that money is then there guaranteed. There is no settlement. There’s no counterparty credit risk. There’s no waiting time.”

The Fastest of Faster Payments:

In a sense, for transactions, paying with CBDCs would be the equivalent of paying via a pneumatic tube that instantly delivers a stack of cash to whoever the sender owes money. It would be real money, not a payment instruction arriving digitally.

Being able to do this will reduce friction, says Walker, and accelerate transactions. For a merchant, this means being able to use funds immediately, say paying a supplier for more inventory. Funds typically used to maintain liquidity could be put to work instead.

Walker suggests that for consumers, paying and receiving funds via CBDCs will mostly feel like a faster version of electronic payments apps available now, except the funds, again, will really be what arrives in their phone. CBDC backers have suggested that a digital U.S. currency would have streamlined and hastened distribution of the various waves of Covid stimulus payments.

One caveat, for banking institutions, is that, depending on design and structure, liquidity could move out of the traditional banking system and become centered in the Federal Reserve, according to Walker. This is interesting in light of the thoughts of the Biden administration’s nominee for Comptroller of the Currency, Saule Omarova. She favors putting banking as we know it into the Federal Reserve System. On the other hand, Omarova is a cryptocurrency skeptic.

Some of this has already happened in Asia. “There wasn’t as much of an appreciation for the implications of CBDCs before the central banks in Asia began experimenting with different models of CBDC,” Walker says.

What a U.S. CBDC Could Look Like

The impression that U.S. development of CBDC policy lags most other nations is not only accurate, but intentional, according to Walker.

“The U.S. central bank has been watching what others have been doing for the purpose of learning from them,” he says. “They’re learning from the innovation of others, watching how different projects at other central banks are developed, and then taking those learnings and incorporating them.” He adds that this is fairly typical of U.S. payments policy. The U.S. FedNow real-time payment project, scheduled for full implementation in 2023, is far behind other nations in the G20, he points out.

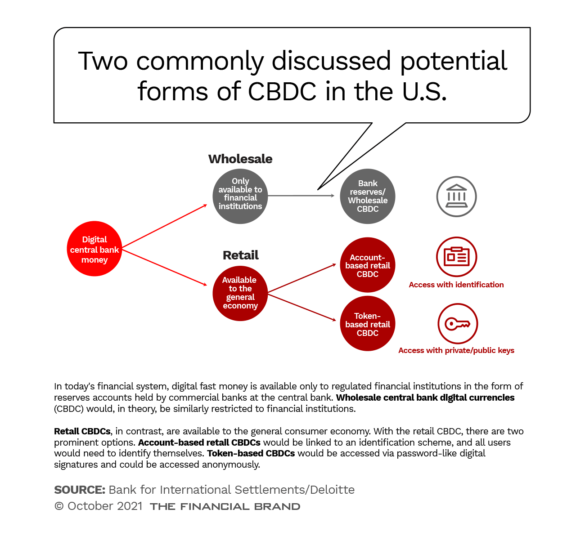

Looking at the Asian experience overall, Walker notes that all countries involved with CBDC there began with “token-based” systems. Put simply, this is an anonymous usage that requires a code to put the transaction through. More recently, according to Walker, Asian CBDC countries have moved into account-based approaches. This entails knowing who is spending the CBDCs.

Walker says this shift reflects the Asian countries being early to the game, before widespread development of digital asset custody infrastructure. This has become more robust in the meantime, so he says later arrivals like the U.S. will be able to tap more technology for CBDC wallets and such.

Just how the U.S. approach would evolve remains to be seen, of course. The diagram below, adapted from one in one of the Deloitte reports, shows in very simple terms how both a wholesale side system would work and how two alternative approaches to the consumer side would work.

Fed Chairman Jerome Powell has made it clear that if the U.S. went ahead with CBDC it would co-exist with existing U.S. currency, at least for a time. Indeed, Walker says it is possible that multiple approaches to a U.S. digital currency could in time co-exist also.

Walker does not believe adoption of a U.S. central bank digital currency would mean the end of Bitcoin and other digital currencies including stablecoins. Walker thinks many different scenarios could play out, some of which would see the three forms of cryptocurrency complementing each other.

Read More: Credit-Hungry Americans Like BNPL, Cards (and Whatever’s Next)

How Far Away is an American CBDC?

When asked about the transition to a CBDC in the U.S., Walker chuckles and notes that in the week before the interview he received two paper checks from individuals. He deposited them via mobile capture. His point is, transitions can take a while, and there’s no reason a shift to a CBDC would be different.

A question that hangs on the design phase is the role for commercial banks in creation of CBDCs.

“The central bank could do all of the ‘minting’ and distribution if the design consisted of one tier, where they create the money supply exclusively,” explains Walker. “Alternatively, there could be a role for commercial banks to be CBDC issuers under a regulatory license and authority from the Federal Reserve.”

One approach might be for commercial banks to have account-based CBDCs, with each bank issuing token-based digital currency to its customers.

Until more clarity comes on the U.S. front, says Walker, “there is no single answer regarding who would mint CBDCs.”