Jamie Dimon is a self-confessed Bitcoin skeptic, and has been for some time. To Dimon, it all comes down to the very point of what “money” is.

“People have to remember that a [traditional] currency is supported by the taxing authority of a country, by the military authority, by the rule of law, by a central bank that makes sure not to debase it. It’s not the same as somebody who has no asset backing,” said the Chairman and CEO of JPMorganChase during a one-on-one at the Wall Street Journal CEO Council virtual gathering in May 2021. “I am not a Bitcoin supporter, I don’t care about Bitcoin. I know I am going to get tons of emails. I have no interest in it.”

Pretty definitive, and yet …

In 2021 Bitcoin and other cryptocurrencies have moved even further out of the realm of fringe finance and more towards the mainstream.

More headlines about cryptocurrencies have been published in 2021 than ever, with many new players coming into the field and a small but growing portion of traditional financial institutions committing to some degree of involvement in the digital currency business. (Among them is Vast Bank, a small Oklahoma community bank that launched crypto accounts in late August, the subject of an article on The Financial Brand.)

Nonbank payment companies like PayPal have moved into the business for payment purposes as well. Visa and MasterCard have multiple forays going into cryptocurrencies.

Yet when the head of the largest U.S. bank says he doesn’t care about Bitcoin, which started the trend, fad or craze, depending on your viewpoint, that should say something, right?

What Do Americans Want?

As more and more men and women on the street know a bit about Bitcoin and want to get in on the action, one is reminded of the possibly apocryphal story of shoeshine boys giving clients stock tips in the frenzied run-up to the 1929 Stock Market crash.

But note this. Even Chase is beginning to offer wealth management clients the opportunity to invest in digital currency opportunities, in spite of Dimon’s ambivalence. CNBC covered this development in an August report, labeling it an “awkward fact.”

Actually, Dimon explained the seeming disconnect pretty clearly.

“Clients are interested and I don’t tell clients what to do,” said Dimon at the WSJ event. “People want us to have custody of it, to have custody of the keys, they want to be able to put it on statements, they want help to be able to buy and sell it. If we can help them to do all those things very, very safely, with all the proper disclosures, then that’s their job. It’s not my job to tell them what to do with their money.”

For example, Chase joined Morgan Stanley and MassMutual in allowing their advisors to recommend investments in a Bitcoin fund run by NYDIG (New York Digital Investment Group LLC). The latter has various arrangements with other financial firms, from FIS to Moven to Nymbus to Kasasa. (CNBC noted that the Chase efforts represented “a muted rollout.”)

Most bankers and credit union executives have been plenty busy operating during an ongoing pandemic and dealing with a host of new competitors. Cryptocurrency may not come knocking on their doors tomorrow, but this fresh source of competition, or new business, in the potential longer run, needs to be further understood.

You may not personally be interested in Bitcoin — or other cryptocurrencies like Ethereum, Dogecoin or Litecoin. (Investopedia says there are an estimated 4,000+ different types of cryptocurrency out there.) But ignoring this trend completely could be like those institutions that thought the internet was a passing fad. The recent revival of the Facebook-led Novi cryptocurrency effort — once nearly left for dead — should be sufficient warning. Novi uses its own crypto payment system, called Diem.

Think of this article as a primer, a sampling of what’s going on and what financial services executives have to be up on in order to remain competitive.

Read More: Will Facebook’s Relaunched Digital Wallet Alter the Future of Payments?

1. What roles do cryptocurrencies play at present?

Cryptocurrencies use blockchain technology, and, in spite of the attractive renderings of them in golden images for article illustrations, they are completely virtual. As Investopedia explains, the significance of the “crypto” in their name refers to their origin as software code. Bitcoin, for example, comes out of computer “mines” devoted to producing the cryptocurrency. This is accomplished through the mines’ computers solving mathematical equations to earn Bitcoins. It gives the term “making money” new meaning.

The value of cryptocurrencies fluctuates on digital markets and can be quite volatile. Hence the invention of “stablecoins,” which typically correlate one-to-one with real governmental currencies, according to a guide from the American Bankers Association. It is similar in a way to the idea of mutual fund share values fluctuating, while money market mutual funds are based on a $1 per share concept. (Stablecoins don’t presently have “legal tender” status in the U.S.)

2. Who is interested in cryptocurrency?

Not so long ago, desire for cryptocurrencies was limited to early adopters who like living on the leading edge. Multiple research studies suggest that cryptocurrencies’ base is broadening and, for investors, interest is moving beyond short-term speculation.

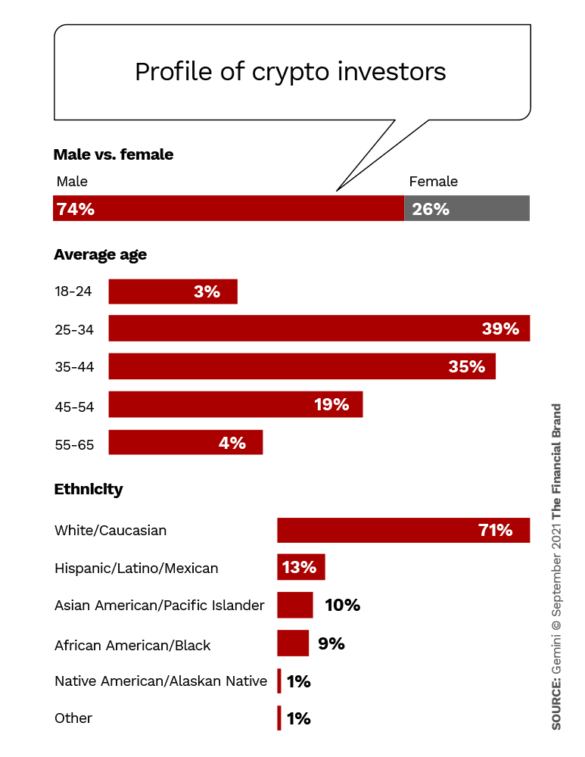

Gemini, a cryptocurrency company that offers a crypto exchange, wallet services, crypto payments and more, estimates in its 2021 State of U.S. Crypto Report that approximately 14% of the U.S. population owns cryptocurrency in some fashion — 21.2 million American adults.

The company’s report states that usage and interest “skews young, male and white” and that the “average” crypto owner is a male, 38, making about $111,000 annually.

The study found that seven out of ten who have bought crypto say they are holding it as a long-term investment, although some appear to buy it for multiple reasons. Nearly four in ten say they do some active trading in crypto and about one in four use crypto for internet purchases.

A “Sort Of” Currency?

The strong interest in investing suggests people regard cryptocurrencies more as investment instruments than as ‘currencies’ in the usual sense.

The Gemini report says further that 63% of American adults are among the “crypto-curious.” These are people who don’t own any crypto but have some interest in learning more. Gemini says just over half of these people are women, and if they follow through, that would change the profile of crypto holders significantly.

Of those who don’t hold crypto, millions could start doing so, as 13% told the company that they plan to buy crypto within the next 12 months. About one in four Americans — 23% — say they don’t care about crypto.

The study found that virtually all (95%) of the crypto curious know about Bitcoin. Familiarity with other currencies falls off quickly, with Ethereum coming in second at 38% and Bitcoin Cash coming in at 24%. (Bitcoin Cash is a “fork” of the original Bitcoin. In the blockchain world, a fork is essentially a “fork in the road” taken for various reason.)

Putting Crypto Investment in Perspective:

A 2021 study by the University of Chicago’s NORC unit, found that 13% of Americans reported that they had purchased or traded crypto in the previous 12 months. In the same period, 24% of respondents had traded stocks in some fashion.

Most investors get their crypto investing information from the exchanges themselves (26%), trading platforms (25%) such as Fidelity or Robinhood, and social media (24%, versus only 9% via traditional media), the NORC study says.

Only 2% get information from a broker or advisor.

3. What’s the attraction of crypto as an investment?

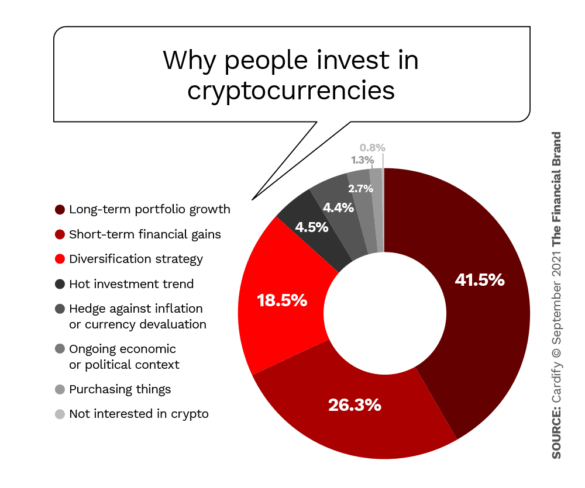

A study by Cardify probed the investment strategy of those buying crypto for that purpose. While many say they are in it for the long term, interestingly one in five appear to regard their investment strictly as a diversification move. Significantly, Cardify found that the average investor holds about 13% of their portfolio in crypto, up from only 3.8% at the same point in 2020.

Yellow Light on Cryptocurrency Investing:

The Cardify study found that only 17% of crypto investors consider their understanding of this asset to be strong. In fact, four out of five crypto investors say they have only a moderate understanding of crypto — or even less.

Note also that the definition of “long term” investing differs among the people in the sample. Cardify noted that while inexperienced investors frequently intended to invest for the long term, they meant by that fewer than 12 months. By contrast, a much greater proportion of experienced investors plan to hold their crypto for more than two years.

Most investors primarily buy their crypto investments on crypto exchanges. The top five worldwide, as ranked by CoinMarketCap, are Binance, Coinbase Exchange, Kraken, Huobi Global and KuCoin. Gemini, whose study was quoted earlier, ranks #15.

The flip side of all this is why people say they aren’t investing in crypto. NORC’s study gave these reasons:

- I don’t understand it enough. 62%

- I don’t think it’s secure. 35%

- I don’t have extra money to invest in anything. 33%

- I don’t know how to invest in cryptocurrency. 31%

- I think the prices move up and down too much. 30%

- I can’t spend it anywhere. 11%

- A financial professional advised me not to. 5%

“If the only reason you’re investing in something is to avoid missing out, the only thing you won’t miss out on is losing everything.”

— from a Coindesk.com tutorial

4. What’s all the talk about crypto wallets and cards?

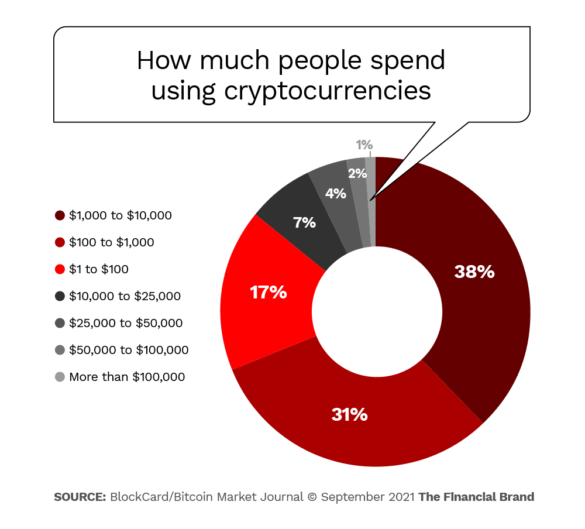

In a 2020 report, BlockCard, a crypto-based spending card, and Bitcoin Market Journal, performed a broad study of spending patterns. Overall, it found that among crypto investors, seven out of ten had spent some cryptocurrency over the previous 12 months. (BlockCard has been rebranding as Unbanked.)

The study found that 77% of those who spent crypto used it to buy more crypto — they want to diversify in multiple cryptocurrencies, the study suggests. Out of other spending categories:

- Entertainment 13%

- Food 11%

- Clothing 8%

- Education 8%

- Housing costs 5%

- Transportation 5%

- Personal care 4%

Here’s how spending levels stack up:

A logical question for newcomers to this area is, how do you go about spending Bitcoin or other cryptocurrency?

More and more alternatives have been invented, and increasingly rewards options are part of the packages.

- PayPal allows users to buy, hold and sell crypto. The app permits use of crypto for certain payments through crypto-enabled checkout. Transactions are reportable for tax purposes, because the transaction involves sale of a financial asset, and transactions are subject to PayPal fees for handling conversion back to standard currency to enable the purchase.

- Venmo has chiefly promoted the ability to buy, hold and sell crypto in the app, even using Venmo balances.

- Crypto.com Rewards Visa is essentially a crypto-backed prepaid debit card, according to an analysis by Bankrate. The site makes the point that beyond the basic level, various rewards levels require “staking” — commitment to lock crypto assets to a given company for a certain length of time.

- Coinbase Commerce enables merchants to accept certain cryptocurrencies for payment. The company says it has more than 8,000 merchants signed up worldwide. The company is introducing Coinbase Card with MetaBank N.A.

- Unbanked, originally called BlockCard, offers a debit card that it says is free of transaction and conversion fees.

- Gift cards are a workaround some consumers use. They buy gift cards with crypto and then use the dollar-denominated cards for their purchases. Numerous crypto companies offer this service.

5. What is the role of central bank digital currencies (CBDCs)?

These are a very different creature than the types of crypto items most banks and credit unions would encounter today, though it is part of the larger matter of crypto assets. A CBDC would be a liability of a central bank, like the Federal Reserve, that can be used as a digital payment instrument — greenbacks made of blips.

Many years ago, at an early blockchain conference, an IBM analyst said, “I keep hearing that the blockchain is the answer. But I want to know what the question was.”

In a similar vein, Federal Reserve Board Governor Christopher Waller noted in an August 2021 speech that the Fed is working on a discussion paper on this issue, but added that “in all the recent exuberance about CBDCs, advocates point to many potential benefits of a Federal Reserve digital currency, but they often fail to ask a simple question: What problem would a CBDC solve?”

What a Federal Reserve CBDC would be is still being formulated. Federal Reserve Board Chairman Jerome Powell has made it clear already that Fed-issued physical currency will not be replaced by federal crypto.

Indeed, in a speech earlier in the summer of 2021, Powell suggested that if the Fed created its own crypto, it would likely negate the need for both crypto like Bitcoin and stablecoins.

As big and broad as the crypto discussion has become, it is still early days, with much in flux with regulators and in Congress.