The growth of online deposits has clearly slowed. The question is whether the deceleration reflects product maturation, or rather a temporary pause caused by low interest rates. It is a bit of both, and how much one vs. the other will become apparent when interest rates rise.

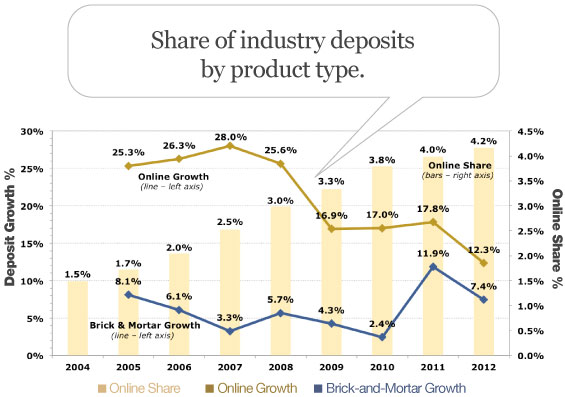

We have estimated and tracked online deposits by type and provider for the past decade, as reflected in the attached chart. Online deposits were growing at a brisk 20-30% pace through 2008, while brick and-mortar deposits were in low/mid-single digits. In response to the financial crisis, the Federal Reserve lowered short-term interest rates to near zero, and pumped in liquidity that increased deposit growth. Online deposit growth tapered off, while traditional deposit growth picked up. Most recently, in 2012, online deposit growth fell to 12%, no longer several times higher than brick & mortar growth.

Two factors are at work. First, as with all new products, the “S-curve” of product adoption translates to high growth off a low base in the early years, and then slows as the base grows and product penetration reaches maturity. Second, the very low rate environment has minimized the difference in deposit rates paid to online vs. traditional deposits. It is one thing to advertise that online rates are ten times higher, but when that only amounts to 10 bp (1/10th of 1%) of interest, it does not motivate people to move their money.

Clearly the grow rate of online deposits must slow as online share grows. Online deposits now account for over four percent of all deposits – heavily skewed toward CDs and savings. But bankers should be cautious about assuming the worst is over. When interest rates return to more normal levels, and the differential between online and traditional deposits rises up toward a full 100 bp (1%) or more, we expect to see renewed switching behavior. This will be accelerated by electronic innovation such as mobile check deposit, which is un-tethering the consumer from the branch. Another potential headache to keep retail bankers up at night.

Lee Kyriacou is Managing Director with Novantas. Lee’s industry research, forecasts and opinions leverage twenty-plus years in consulting and banking to offer industry analysis and insights. His banking experience includes head of bank-wide financial planning and analysis, as well as strategy and M&A roles, at two top ten banks. Lee also has an banking business focus in consumer and wholesale payments and payments-related lending.