Financial marketers may find themselves in an odd spot as institutions attempt to meet demand, prudently, while at the same time lenders work with companies that are already having difficulties with their finances. No lender has ever worked in and through today’s kind of environment.

“This is an incredibly uncertain and unprecedented time,” says Catherine Mann, Managing Director and Global Chief Economist at Citigroup. She is head of the American Bankers Association’s Economic Advisory Committee. The best case scenario seen by the 16 big bank economists on the committee is for the beginning of a recovery in the third quarter.

Beyond that there was only a little consensus among the group’s members. Many don’t see a recovery coming until 2022. Double-digit unemployment is expected to prevail through the end of the year, peaking at 19% and tapering down to 10%. The group expects businesses to let inventories run down through the end of the year and to hold off on spending on new production capacity.

Nearly all economists in the group expect both business credit availability and business credit quality to fall off.

“It remains to be seen whether and when consumer behavior and business activity will return to the normal levels we used to know,” said Mann, “while many believe there will be substantial changes in the post-pandemic world.”

One hears and reads anecdotes about frustrated small business owners and managers pushing the line on their state’s “curbside” rules and about others who in desperation simply choose to break lockdown rules to hold onto a shred of hope that they can remain solvent. Financial institutions, especially community banks, pushed to get Paycheck Protection Program funds into small firms’ hands quickly, in hopes of saving jobs and tiding the companies over to … what, exactly?

Worries about Business and Business Credit, Bolstered by Fears

Even as people get used to the phrase “new normal,” signs of that new normal seem harder and harder to see, and the advent of widespread protests and rioting may have put things off further.

In early June, the new Acting Comptroller of the Currency, Brian Brooks, issued a remarkable warning about the future of businesses and banks themselves if state and local governments didn’t permit more businesses to reopen soon.

In an open letter to associations representing state and local leaders, Brooks said continued lockdowns had to be weighed carefully “because certain aspects of these orders potentially threaten the stability and orderly functioning of the financial system the OCC is charged by law to protect.”

For example, Brooks noted, in some cities leaders have cut off water, electricity or other utilities in order to shut down violators of local lockdown orders. “Banks are a major source of commercial real estate finance in the United States,” he wrote. “Cutting off utilities to commercial buildings can impair their condition, structural integrity, and value, thus impairing the collateral that secures real estate loans.”

Continued stay-at-home orders are having their own impact on commercial properties. “While some cities and states are reopening their economies, others reportedly are extending their lockdown orders for weeks or even months,” Brooks wrote, exposing properties to burglary and vandalism while unoccupied.

But then Brooks went to the heart of lending:

“We now have anecdotal reports of banks that are experiencing small-business loan delinquency rates in the mid-double-digits on loan books that reflected strong cash flow expectations and pristine credit quality at the time of origination, prior to local lockdown orders. Such high delinquency rates have the potential to threaten the community and mid-size banks that are the economic lifeblood of local communities, a factor that your members should take into account in weighing the risks and benefits of lengthy continued lockdown orders.”

In early May a survey by CNBC of 2,200 small firms across the country asked how long they could survive under lockdown conditions: 31% thought they had a few months or less, and 13% had even less time if lockdowns continued. A similar survey of small firms, conducted by the Society for Human Resource Management, released around the same time, reported that just over half of the businesses feared going under.

Philadelphia’s Customers Bank surveyed area business owners and leaders on COVID credit issues in preparation for a town hall. The top two concerns were access to markets, cited by 62%, and access to financial capital, 31.7%. When asked what types of credit they had applied for, 95% reported the Paycheck Protection Program, 35% Small Business Administration Economic Injury Disaster Loans, 15% SBA Express Loans … and only 5% conventional bank financing.

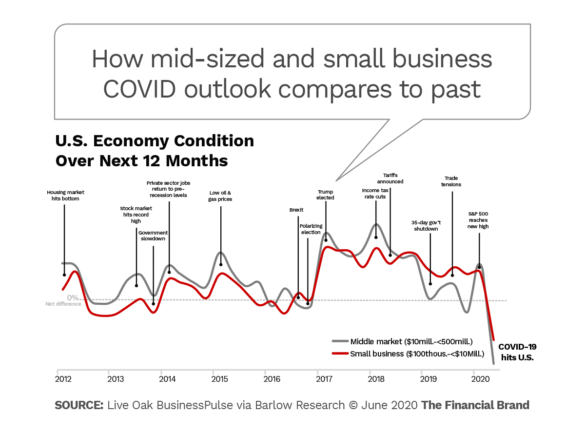

Small businesses face many risks even in the best of times, but the sentiment among middle-market and small businesses has plummeted to record lows as a result of concerns about the impact of COVID-19 on the economy, according to Live Oak Bank’s BusinessPulse survey, conducted by Barlow Research, as shown in the chart below. (The survey was conducted in early April, before the economy’s coronavirus pause had gone on for over three months.)

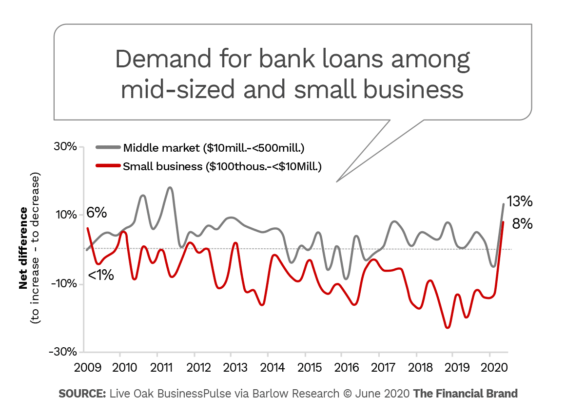

This bank’s study found a mixed picture on credit demand and lender reception of that demand. 72% of the survey group had not applied for new business credit when the research was performed. Of the 28% that did seek credit, the majority were seeking unsecured short-term loans (32%) and secured short-term loans (also 32%). Three-quarters of applications were being approved, 18% partially approved, and 7% turned down.

A study by the National Federation of Independent Business found that interest in expansion has fallen among all sectors of small firms. This reflects a massive loss of optimism in every category of potential future improvement. Expectations of a resurgence of sales has slid significantly

Business Credit Worries Bolstered by Early Facts

Beyond the Comptroller’s warnings, worrisome signs are beginning to arise in the business lending sector.

The Live Oak BusinessPulse research indicates that midsized and small firms want traditional credit, as opposed to the findings of the Customers Bank survey among a small market sample, which suggests a greater reliance on federal aid.

How well they can pay for fresh credit is an open question. The last industrywide numbers from FDIC were yearend 2019 figures, so the totality of banking results for the first quarter 2020 remains to be seen. However, in late May the Risk Management Association in partnership with AFS unveiled findings for the first quarter of 2020 from its database of over 710,000 commercial and industrial loans (C&I) and commercial real estate loans (CRE). In a webinar AFS’s Tom Cronin, Manager, recounted some key findings:

• Total C&I loans surged during the end of the first quarter as business borrowers, including many large ones, drew down lines of credit in order to stockpile cash and brace for disruptions in cash flow. Cronin noted that every bank participating in the database saw C&I loans rise, and that the median increase in outstanding loans from the fourth quarter of 2019 was 9.4%.

Cronin said that such a quarterly increase had never been seen in the 17 years that AFS has maintained the database.

Short-term delinquencies (30-89 days past due) on C&I loans hit the highest level seen since the end of the Great Recession — 0.86% for the quarter. The larger the loan, the greater the decrease in performance, according to Cronin. He added that this is the reverse of the usual pattern, in which more small C&I loans generally run into trouble than large ones.

Average delinquencies for the quarter came to 0.96%, a jump from yearend levels of 0.60%. Many industry groups were at or above yearend delinquency levels.

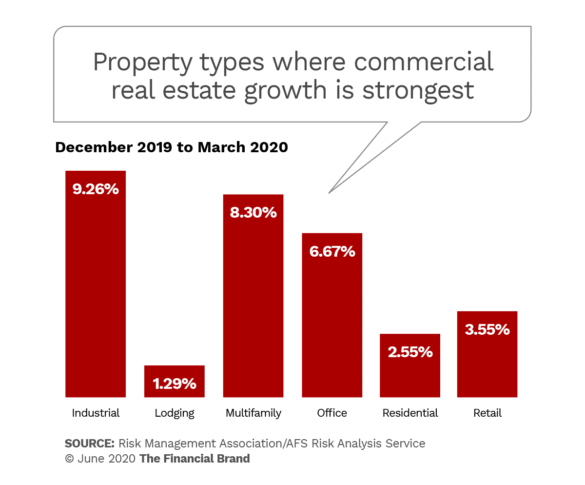

• Commercial real estate lending grew at a “healthy pace.”

Cronin said it appears that a good deal of the growth seen in the chart above for industrial buildings consists of warehouse space for companies involved in ecommerce. Multifamily housing lending is back in favor, after a lull. However, Cronin pointed to the rise in office building CRE credit as a concern in an economy where many companies have not yet brought staff back to offices and where others question whether they even need to do that.

• CRE delinquencies loom larger. They are rising to levels not seen since 2015, according to Cronin. Short-term delinquencies (30-89 days past due) were at 0.6% for the quarter.

• Many banks in the study group have at least doubled their quarterly provision for loan losses. The provision is the amount that a bank adds to its overall allowance for loan and lease losses, one of the cushions that banks maintain to protect themselves when conditions appear to be worsening.

Cronin said the level of loans criticized by examiners is rising and that there was the beginning of a flight to quality by lenders to be seen in the study’s numbers.

Overall, S&P Global Market Intelligence said in a separate report, “if losses reach Great Recession levels, we think that banks’ forecasts will come up short, requiring them to record very large reserve buildings through 2021, resulting in far lower returns on equity.”

The firm added that, “while the industry as a whole seems well equipped for even heightened losses, some banks will still fall short and certainly will find themselves in need of capital or could pursue distressed sales [of assets] later this year.”

Working with Borrowers Facing Difficulties

Financial institutions began offering various forms of relief to commercial borrowers early in the COVID-19 shutdown, notably payment deferrals, waivers of fees, and extensions of payment terms. Nearly all of the commercial banks taking part in a joint study by Greenwich Associates and S&P Global Market Intelligence found that full or partial payment deferrals were almost universal, at least in mid-April. Most were by request, though 15% of the institutions were offering deferrals. 28% were offering firms liquidity credit lines.

“Banks have started taking other actions to preserve loan portfolio quality and revenues — especially in the large corporate and middle-market segments,” the two firms observe. “A majority of large corporate banks and just over half of middle market banks have elevated underwriting standards on new loans.”

The period ahead will be difficult for most small businesses, certainly, as well as even some major brands that have entered bankruptcy proceedings or are considering doing so. Live Oak Bank’s research indicates that very few small firms — 14% — expect to be able to build up cash reserves over the next year. Nearly half — 48% — expect reserves to slip. Things are worse among the middle-market companies surveyed, 55% of which expect slippage.

Both categories of companies have seen increases in owners tapping personal savings to finance business operations. Nearly one out of three small business owners went into their own wallets to keep things going.

And the survey found that less than half of small firms expect to see any growth in the next five years — half a decade of stagnation brought on by less than four months of shutdown, apparently.

Much-Awaited Fed Main Street Program Remains a Wild Card

Funding for the Main Street program goes back to the CARES Act, passed in late March.

Unlike the Paycheck Protection Program, which launched in April, the multi-faceted Main Street Lending Program still hadn’t launched as of early June. It was imminent, but had been that way for a while.

The Boston Federal Reserve Bank was tasked with setting up this lending facility. “This is an important program, and we’ve worked very hard to get it right. We listened carefully to initial feedback and expanded the program in a number of ways to serve a wider range of borrowers,” said Eric Rosengren, President, in a speech.

If you put aside government-sponsored enterprises like Fannie Mae and Freddie Mac that purchase mortgages, SBA and similar guarantees, and some other programs, this more active participation in business lending by the Fed is a watershed change.

How many companies will be able to use it remains to be seen. For many firms, the minimum loans are too large, even after a reduction to $500,000 for new loans, according to community bank commenters and others. (Banks actually make the loans, and receive a 1% origination fee. The Fed buys most of the loan, the percentage varying according to certain factors. Institutions can lend and then send the credit to the program for potential purchase, or offer the loan conditioned on acceptance of the loan by the Fed. Depending on the type of loan, the lender retains a 5% or 15% share, to have “skin in the game.”)

While financial institutions are preparing to participate in the Main Street program, appetite for the offerings has been questioned. S&P Global Market Intelligence, in a recent roundup of bankers, suggests that many businesses are concentrating on reopening right now. In any event, these loans are intended to help sound companies whose business was damaged by COVID-19 and the lockdowns. The effort is not intended as a rescue program for troubled firms and unlike PPP loans that could qualify for forgiveness, Main Street loans must be repaid.

Says Rosengren about the Main Street program: “It will not be able to assist everyone, but we expect that it will provide an important bridge for many businesses that employ much of the American workforce.”