“There is no data about the future. There is only data about the past,” states a report from Deloitte. That would seem limiting for a forward-focused document, but it’s part of what sets this particular effort apart from the glut of predictions attempting to make sense of the coronavirus pandemic for banking.

Rather than staking out any particular viewpoint, the report is a tool for retail banking executives to identify decisions to be made and actions to be taken to remain successful, or even viable, in what could continue to be a rapidly changing landscape.

The report grew out of a joint project between Deloitte and Salesforce to identify likely pandemic-driven scenarios impacting business and society at large. The four scenarios distill uncertainties relating to the possible progression of the disease and the degree of collaboration between countries in responding to the pandemic going forward. The consulting firm applied the four broad themes specifically to consumer banking.

The industry’s future, even compared to the rapid changes of the last three-to-five years, is extremely uncertain now, observes Gopi Billa, Principal and U.S. Banking and Capital Markets Strategy Practice Leader for Deloitte and one of the report’s principal authors. “We don’t know what’s going to play out. What we do know are the underlying elements — the scenarios. How these unfold will be what banking’s future looks like.”

4 Pandemic Scenarios and Their Impact on Banking

The boxes below condense the detailed descriptions Deloitte created for how each of scenario could accelerate or redirect the consumer banking industry over the next one to three years.

The firm recommends that bank and credit union executives “resist the temptation to focus on the scenario closest to your current expectations” or assign probabilities to them. “The question should be, ‘What do we need to be ready for, even if we think it’s improbable?'”

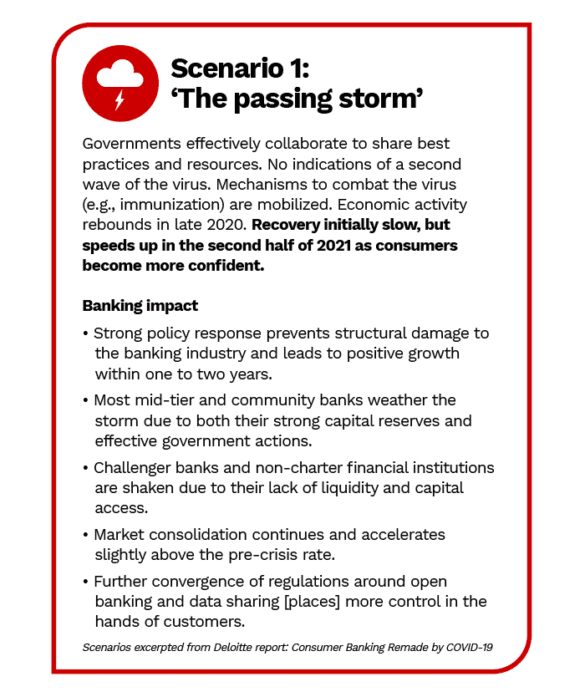

Naturally most people would hope this scenario describes what will actually happen. As indicated above, incumbent financial institutions, other than those that may struggle from credit- or revenue-related issues, could emerge in a strong competitive position especially by comparison to fintech challengers. As the report notes, however, this scenario could lead to only marginal increases in digital banking investments. Ultimately that lack of commitment could make traditional institutions more vulnerable to inroads from big techs like Google or big retailers like Amazon and Walmart, many of which did well through the early stages of the pandemic.

In a conversation with The Financial Brand, Billa notes an astonishing figure: In terms of financial services patents, the top nine tech firms globally outstrip the top 17 banking and payments companies by 20 to 1.

“These tech companies have the ability to scale up, especially because they also are cash rich,” Billa states. “They have been positively affected by this crisis overall.”

He acknowledges that entering banking directly requires becoming regulated, which many nonbank companies may want to avoid. Partnership with banks and credit unions thus may continue to be the preferred route. But such partnerships often involve only a few institutions.

Read More:

- How to Keep Seniors Coming to Digital Banking After America Reopens

- Banks Face Big Risks Shrinking Branch Networks as Pandemic Recedes

- 5 Vital CX Lessons Financial Institutions Can Extract from the Crisis

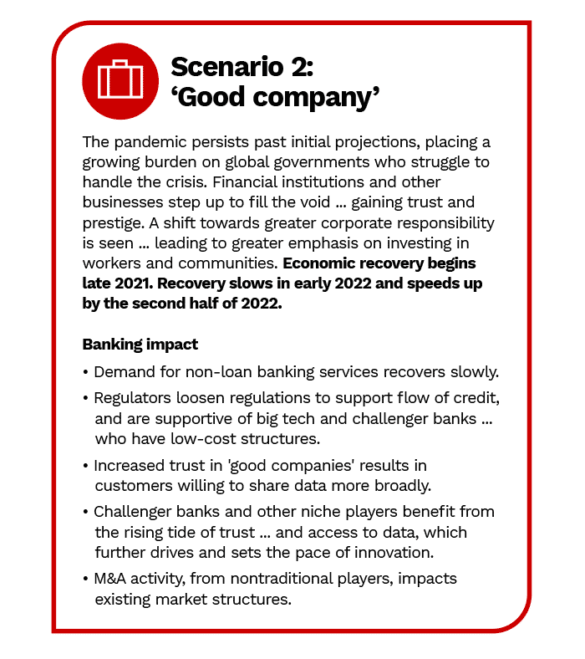

Community banks and credit unions have already had a taste of the positive reputational glow resulting from their efforts to help small businesses to receive Paycheck Protection Program loans. However, the above scenario projects a much later economic recovery than the “The passing storm” scenario. That could lead to significant inroads in lower-end credit from fintech lenders — at least those that get past the current funding challenges.

Billa expects that narrowly-focused fintech lenders — he refers to them as “monolines” — will “start kicking in because there will be a need for cheaper loans” — in mortgages, for example. Incumbent institutions with high-cost infrastructures will find that difficult to match.

As the report notes, “advice and speed to credit are among the most critical competencies developed by ‘good companies’.” That factor could accelerate the transformation of bank and credit union branches from full-service channels to a “relationship management channel focused on advice for consumers,” the report states.

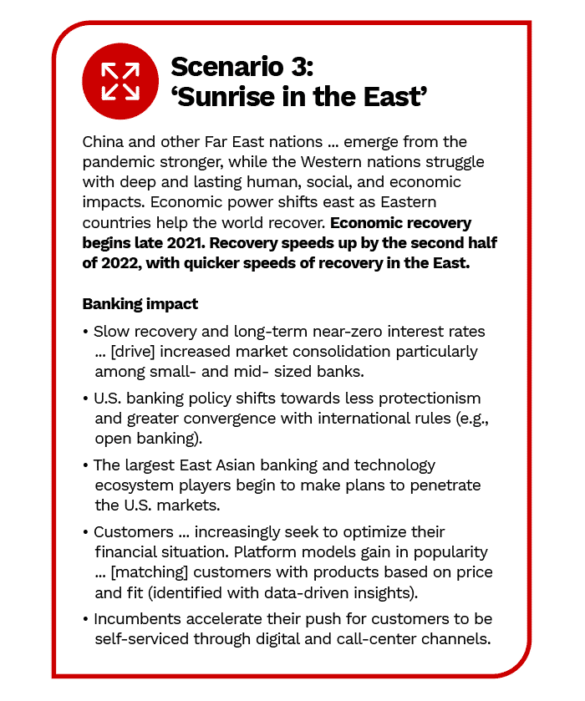

This scenario could prove particularly challenging for incumbent retail banking institutions in the U.S., as it accelerates some of the most disruptive trends that have so far been slow to develop in the U.S. For example, it could see customer loyalty to banks and credit unions diminish as more consumers turn to aggregators and digital marketplaces supported by big tech firms and foreign entrants, according to Deloitte. This would make ownership of the customer experience far more important.

Financial institutions “should expect consumers to have greater control over their data and how the data is used, which is what open banking is about,” states Billa. He thinks that trend will continue and if anything will become even more prominent as people become more and more accustomed to handling banking transactions online.

Whether U.S. regulators decide to push for open banking regulations as their counterparts in Europe and elsewhere have done is a “big unknown,” says Billa. “And that is what eventually will make open banking work or not.” But he feels consumers are ready.

Read More:

- Ally CMO to Banks: ‘It’s Time to Get Rolling Again!’

- Will the Pandemic Give Digital-Only Financial Institutions a Big Win?

- COVID-19 Turns Banks’ Digital Tools into Trust-Building Opportunities

- Bank Branches: There’s No Going Back to Pre-COVID Days

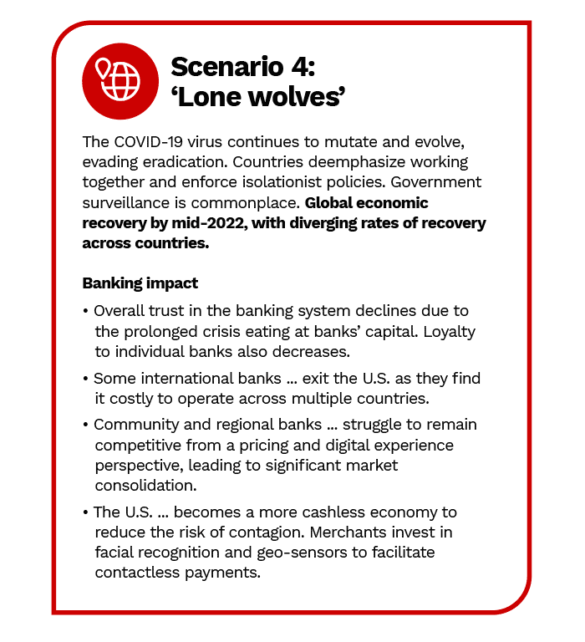

Clearly the worst-case of the four scenarios, this turn of events would severely test incumbents and newcomers on many levels. With COVID-19 — or some mutation of it — lingering for years, Deloitte expects a “strong desire for ‘no-touch’ and ‘light touch’ hyper-personalized experiences will drive adoption of all things contactless.” Being able to meet that demand will become a meaningful differentiator. The firm further believes that in this scenario direct banks with no physical presence (chartered institutions like Marcus and Ally as distinct from most challenger banks) will “decimate” branch-based models.